Developing a multi-currency Expert Advisor (Part 9): Collecting optimization results for single trading strategy instances

Introduction

We have already implemented a lot of interesting things in the previous articles. We have a trading strategy or several trading strategies that we can implement in the EA. Besides, we have developed a structure for connecting many instances of trading strategies in a single EA, added tools for managing the maximum allowable drawdown, looked at possible ways of automated selection of sets of strategy parameters for their best work in a group, learned how to assemble an EA from groups of strategy instances and even from groups of different groups of strategy instances. But the value of the results already obtained will greatly increase if we manage to combine them together.

Let's try to outline a general structure within the article framework: single trading strategies are fed into the input, while the output is a ready-made EA, which uses selected and grouped copies of the original trading strategies that provide the best trading results.

After drawing up a rough road map, let's take a closer look at some section of it, analyze what we need to implement the selected stage, and get down to the actual implementation.

Main stages

Let's list the main stages that we will have to go through while developing the EA:

- Implementing a trading strategy. We develop the class derived from CVirtualStrategy, which implements the trading logic of opening, maintaining and closing virtual positions and orders. We did this in the first four parts of the series.

- Trading strategy optimization. We select good sets of inputs for a trading strategy that show noteworthy results. If none are found, then we return to point 1.

As a rule, it is more convenient for us to perform optimization on one symbol and timeframe. For genetic optimization, we will most likely need to run it several times with different optimization criteria, including some of our own. It will only be possible to use brute force optimization in strategies with a very small number of parameters. Even in our model strategy, exhaustive search is too expensive. Therefore, further on, while speaking about optimization, I will imply genetic optimization in the MetaTrader 5 strategy tester. The optimization process was not described in detail in the articles, since it is pretty standard. - Clustering of sets. This step is not mandatory, but will save some time in the next step. Here we significantly reduce the number of sets of parameters of trading strategy instances, among which we will select suitable groups. This is described in the sixth part.

- Selecting groups of parameter sets. Based on the results of the previous stage, perform optimization selecting

the most compatible sets of parameters of trading strategy instances that produce the best results. This is also mainly described in the sixth and seventh parts. - Selecting groups from groups of parameter sets. Now combine the results of the previous stage into groups using the same principle as when combining the sets of single instance parameter sets.

- Iterating through symbols and timeframes. Repeat steps 2 - 5 for all desired symbols and timeframes. Perhaps, in addition to a symbol and timeframe, it is possible to conduct separate optimization on certain classes of other inputs for some trading strategies.

- Other strategies. If you have other trading strategies in mind, then repeat steps 1 - 6 for each of them.

- Assembling the EA. We collect all the best groups of groups found for different trading strategies, symbols, timeframes and other parameters into one final EA.

Each stage, upon completion, generates some data that needs to be saved and used in the next stages. So far we have been using temporary improvised means, convenient enough to use once or twice, but not particularly convenient for repeated use.

For example, we saved the optimization results after the second stage in an Excel file, then manually added the missing columns, and then, having saved it as a CSV file, used it in the third stage.

We either used the results of the third stage directly from the strategy tester interface, or saved them again in Excel files, carried out some processing there, and again used the results obtained from the tester interface.

We did not actually carry out the fifth stage, only noting the possibility of carrying it out. Therefore, it never came to fruition.

For all these received data, we would like to implement a single storage and usage structure.

Implementation options

Essentially, the main type of data we need to store and use is the optimization results of multiple EAs. As you know, the strategy tester records all optimization results in a separate cache file with the *.opt extension, which can then be reopened in the tester or even opened in the tester of another MetaTrader 5 terminal. The file name is determined from the hash calculated based on the name of the optimized EA and the optimization parameters. This allows us not to lose information about the passes already made when continuing optimization after its early interruption or after changing the optimization criterion.

Therefore, one of the options under consideration is the use of optimization cache files to store intermediate results. There is a good library from fxsaber allowing us to access all saved information from MQL5 programs.

But as the number of optimizations performed increases, the number of files with their results will also increase. In order not to get confused, we will need to come up with some additional structure for arranging the storage and working with these cache files. If optimization is not carried out on one server, then it will be necessary to implement synchronization or storing all cache files in one place. In addition, for the next stage we will still need some processing to export the obtained optimization results to the EA at the next stage.

Then let's look at arranging the storage of all results in the database. At first glance, this would require quite a lot of time to implement. But this work can be broken down into smaller stages, and we will be able to use its results immediately, without waiting for full implementation. This approach also allows for greater freedom in choosing the most convenient means of intermediate processing of stored results. For example, we can assign some processing to simple SQL queries, something will be calculated in MQL5, and something in Python or R programs. We will be able to try different processing options and choose the most suitable one.

MQL5 offers built-in functions for working with the SQLite database. There were also implementations of third-party libraries that allow working, say, with MySQL. It is not yet clear whether SQLite capabilities will be enough for us, but most likely this database will be sufficient for our needs. If it is not sufficient, then we will think about migrating to another DBMS.

Let's start designing the database

First, we need to identify the entities whose information we want to store. Of course, one test run is one of them. The fields of this entity will include test input data fields and test result fields. Generally, they can be distinguished as separate entities. The essence of the input data can be broken down into even smaller entities: the EA, optimization settings and EA single-pass parameters. But let's continue to be guided by the principle of least action. To begin with, one table with fields for the pass results that we used in previous articles and one or two text fields for placing the necessary information about the pass inputs will be sufficient for us.

Such a table can be created with the following SQL query:

CREATE TABLE passes (

id INTEGER PRIMARY KEY AUTOINCREMENT,

pass INT, -- pass index

inputs TEXT, -- pass input values

params TEXT, -- additional pass data

initial_deposit REAL, -- pass results...

withdrawal REAL,

profit REAL,

gross_profit REAL,

gross_loss REAL,

max_profittrade REAL,

max_losstrade REAL,

conprofitmax REAL,

conprofitmax_trades REAL,

max_conwins REAL,

max_conprofit_trades REAL,

conlossmax REAL,

conlossmax_trades REAL,

max_conlosses REAL,

max_conloss_trades REAL,

balancemin REAL,

balance_dd REAL,

balancedd_percent REAL,

balance_ddrel_percent REAL,

balance_dd_relative REAL,

equitymin REAL,

equity_dd REAL,

equitydd_percent REAL,

equity_ddrel_percent REAL,

equity_dd_relative REAL,

expected_payoff REAL,

profit_factor REAL,

recovery_factor REAL,

sharpe_ratio REAL,

min_marginlevel REAL,

deals REAL,

trades REAL,

profit_trades REAL,

loss_trades REAL,

short_trades REAL,

long_trades REAL,

profit_shorttrades REAL,

profit_longtrades REAL,

profittrades_avgcon REAL,

losstrades_avgcon REAL,

complex_criterion REAL,

custom_ontester REAL,

pass_date DATETIME DEFAULT (datetime('now') )

NOT NULL

);

Let's create the auxiliary CDatabase class, which will contain methods for working with the database. We can make it static, since we do not need many instances in one program, just one is sufficient. Since we are currently planning to accumulate all the information in one database, we can rigidly specify the database file name in the source code.

This class will contain the s_db field for storing the open database handle. The Open() database opening method will set its value. If the database has not yet been created at the time of opening, it will be created by calling the Create() method. Once opened, we can execute single SQL queries to the database using the Execute() method or bulk SQL queries in a single transaction using the ExecuteTransaction() method. At the end, we will close the database using the Close() method.

We can also declare a short macro that allows us to replace the long CDatabase class name with the shorter DB.

#define DB CDatabase //+------------------------------------------------------------------+ //| Class for handling the database | //+------------------------------------------------------------------+ class CDatabase { static int s_db; // DB connection handle static string s_fileName; // DB file name public: static bool IsOpen(); // Is the DB open? static void Create(); // Create an empty DB static void Open(); // Opening DB static void Close(); // Closing DB // Execute one query to the DB static bool Execute(string &query); // Execute multiple DB queries in one transaction static bool ExecuteTransaction(string &queries[]); }; int CDatabase::s_db = INVALID_HANDLE; string CDatabase::s_fileName = "database.sqlite";

In the database creation method, we will simply create an array with SQL queries for creating tables and execute them in one transaction:

//+------------------------------------------------------------------+ //| Create an empty DB | //+------------------------------------------------------------------+ void CDatabase::Create() { // Array of DB creation requests string queries[] = { "DROP TABLE IF EXISTS passes;", "CREATE TABLE passes (" "id INTEGER PRIMARY KEY AUTOINCREMENT," "pass INT," "inputs TEXT," "params TEXT," "initial_deposit REAL," "withdrawal REAL," "profit REAL," "gross_profit REAL," "gross_loss REAL," ... "pass_date DATETIME DEFAULT (datetime('now') ) NOT NULL" ");" , }; // Execute all requests ExecuteTransaction(queries); }

In the open database method, we will first try to open an existing database file. If it does not exist, then we create and open it, after which we create the database structure by calling the Create() method:

//+------------------------------------------------------------------+ //| Is the DB open? | //+------------------------------------------------------------------+ bool CDatabase::IsOpen() { return (s_db != INVALID_HANDLE); } ... //+------------------------------------------------------------------+ //| Open DB | //+------------------------------------------------------------------+ void CDatabase::Open() { // Try to open an existing DB file s_db = DatabaseOpen(s_fileName, DATABASE_OPEN_READWRITE | DATABASE_OPEN_COMMON); // If the DB file is not found, try to create it when opening if(!IsOpen()) { s_db = DatabaseOpen(s_fileName, DATABASE_OPEN_READWRITE | DATABASE_OPEN_CREATE | DATABASE_OPEN_COMMON); // Report an error in case of failure if(!IsOpen()) { PrintFormat(__FUNCTION__" | ERROR: %s open failed with code %d", s_fileName, GetLastError()); return; } // Create the database structure Create(); } PrintFormat(__FUNCTION__" | Database %s opened successfully", s_fileName); }

In the method of executing multiple ExecuteTransaction() queries, we create a transaction and start executing all SQL queries in a loop one by one. If an error occurs while executing the next request, we interrupt the loop, report the error, and cancel all previous requests within this transaction. If no errors occur, confirm the transaction:

//+------------------------------------------------------------------+ //| Execute multiple DB queries in one transaction | //+------------------------------------------------------------------+ bool CDatabase::ExecuteTransaction(string &queries[]) { // Open a transaction DatabaseTransactionBegin(s_db); bool res = true; // Send all execution requests FOREACH(queries, { res &= Execute(queries[i]); if(!res) break; }); // If an error occurred in any request, then if(!res) { // Report it PrintFormat(__FUNCTION__" | ERROR: Transaction failed, error code=%d", GetLastError()); // Cancel transaction DatabaseTransactionRollback(s_db); } else { // Otherwise, confirm transaction DatabaseTransactionCommit(s_db); PrintFormat(__FUNCTION__" | Transaction done successfully"); } return res; }

Save the changes in the Database.mqh file of the current folder.

Modifying the EA to collect optimization data

When using only agents on the local computer in the optimization process, we can arrange saving the pass results to the database either in OnTester(), or OnDeinit() handler. When using agents in a local network or in the MQL5 Cloud Network, it will be very difficult, if possible, to achieve saving the results. Fortunately, MQL5 offers a great standard way to get any information from test agents, wherever they are, by creating, sending and receiving data frames.

This mechanism is described in sufficient detail in the reference and in the AlgoBook. In order to use it, we need to add three additional event handlers to the optimized: OnTesterInit(), OnTesterPass() and OnTesterDeinit().

Optimization is always launched from some MetaTrader 5 terminal, which we will henceforth conditionally call the main one. When an EA with such handlers is launched from the main terminal for optimization, a new chart is opened in the main terminal, and another instance of the EA is launched on this chart before distributing the EA instances to testing agents to perform normal optimization passes with different sets of parameters.

This instance is launched in a special mode: the standard OnInit(), OnTick() and OnDeinit() handlers are not executed in it. Only these three new handlers are executed instead. This mode even has its own name - the mode of collecting frames of optimization results. If necessary, we can check that the EA is running in this mode in the EA functions by calling the MQLInfoInteger() function the following way:

// Check if the EA is running in data frame collection mode bool isFrameMode = MQLInfoInteger(MQL_FRAME_MODE);

As the names suggest, in frame collection mode, the OnTesterInit() handler runs once before optimization, OnTesterPass() runs every time any of the test agents completes its pass, while OnTesterDeinit() runs once after all scheduled optimization passes are completed or when optimization is interrupted.

The EA instance launched on the main terminal chart in the frame collection mode will be responsible for collecting data frames from all test agents. "Data frame" is just a convenient name to use when describing the data exchange between test agents and the EA in the main terminal. It denotes a data set with a name and a numeric ID that the test agent created and sent to the main terminal after completing a single optimization pass.

It should be noted that it makes sense to create data frames only in the EA instances operating in normal mode on the test agents, and to collect and handle data frames only in the EA instance in the main terminal operating in frame collection mode. So let's start with creating frames.

We can place the creation of frames in the EA in the OnTester() handler or in any function or method called from OnTester(). The handler is launched after the completion of the pass, and we can get in it the values of all statistical characteristics of the completed pass and, if necessary, calculate the value of the user criterion for evaluating the pass results.

We currently have the code in it that calculates a custom criterion showing the predicted profit that could be obtained given the maximum achievable drawdown of 10%:

//+------------------------------------------------------------------+ //| Test results | //+------------------------------------------------------------------+ double OnTester(void) { // Maximum absolute drawdown double balanceDrawdown = TesterStatistics(STAT_EQUITY_DD); // Profit double profit = TesterStatistics(STAT_PROFIT); // The ratio of possible increase in position sizes for the drawdown of 10% of fixedBalance_ double coeff = fixedBalance_ * 0.1 / balanceDrawdown; // Recalculate the profit double fittedProfit = profit * coeff; return fittedProfit; }

Let's move this code from the SimpleVolumesExpertSingle.mq5 EA file to the new CVirtualAdvisor method class, while the EA is left with returning the method call result:

//+------------------------------------------------------------------+ //| Test results | //+------------------------------------------------------------------+ double OnTester(void) { return expert.Tester(); }

When moving, we should consider that we can no longer use the fixedBalance_ variable inside the method, since it may not be present in another EA as well. But its value can be obtained from the CMoney static class by calling the CMoney::FixedBalance() method. Along the way, we will make one more change to the calculation of our user criterion. After determining the projected profit, we will recalculate it per unit of time, for example, profit per year. This will allow us to roughly compare the results of passes over periods of different lengths.

To do this, we need to remember the test start date in the EA. Let's add the new property m_fromDate, which is to store the current time in the EA object constructor.

//+------------------------------------------------------------------+ //| Class of the EA handling virtual positions (orders) | //+------------------------------------------------------------------+ class CVirtualAdvisor : public CAdvisor { protected: ... datetime m_fromDate; public: ... virtual double Tester() override; // OnTester event handler ... }; //+------------------------------------------------------------------+ //| OnTester event handler | //+------------------------------------------------------------------+ double CVirtualAdvisor::Tester() { // Maximum absolute drawdown double balanceDrawdown = TesterStatistics(STAT_EQUITY_DD); // Profit double profit = TesterStatistics(STAT_PROFIT); // The ratio of possible increase in position sizes for the drawdown of 10% of fixedBalance_ double coeff = CMoney::FixedBalance() * 0.1 / balanceDrawdown; // Calculate the profit in annual terms long totalSeconds = TimeCurrent() - m_fromDate; double fittedProfit = profit * coeff * 365 * 24 * 3600 / totalSeconds ; // Perform data frame generation on the test agent CTesterHandler::Tester(fittedProfit, ~((CVirtualStrategy *) m_strategies[0])); return fittedProfit; }

Later, we might make several custom optimization criteria, and then this code will be moved again to a new location. But for now, let's not get distracted by the extensive topic of studying various fitness functions for optimizing EAs and leave the code as is.

The SimpleVolumesExpertSingle.mq5 EA file now gets new handlers OnTesterInit(), OnTesterPass() and OnTesterDeinit(). Since, according to our plan, the logic of these functions should be the same for all EAs, we will first lower their implementation to the EA level (CVirtualAdvisor class object).

It should be taken into account that when the EA is launched in the main terminal in the frame collection mode, the OnInit() function, in which the EA instance is created, will not be executed. Therefore, in order not to add creation/deletion of an EA instance to new handlers, make the methods for handling these events static in the CVirtualAdvisor class. Then we need to add the following code to the EA:

//+------------------------------------------------------------------+ //| Initialization before starting optimization | //+------------------------------------------------------------------+ int OnTesterInit(void) { return CVirtualAdvisor::TesterInit(); } //+------------------------------------------------------------------+ //| Actions after completing the next optimization pass | //+------------------------------------------------------------------+ void OnTesterPass() { CVirtualAdvisor::TesterPass(); } //+------------------------------------------------------------------+ //| Actions after optimization is complete | //+------------------------------------------------------------------+ void OnTesterDeinit(void) { CVirtualAdvisor::TesterDeinit(); }

Another change we can make for the future is to get rid of the separate call to the CVirtualAdvisor::Add() method for adding trading strategies to the EA after it is created. Instead, we will immediately transfer information about strategies to the EA's constructor, while it will call the Add() method on its own. Then this method can be removed from the public part.

With this approach, the OnInit() EA initialization function will look as follows:

int OnInit() { CMoney::FixedBalance(fixedBalance_); // Create an EA handling virtual positions expert = new CVirtualAdvisor( new CSimpleVolumesStrategy( symbol_, timeframe_, signalPeriod_, signalDeviation_, signaAddlDeviation_, openDistance_, stopLevel_, takeLevel_, ordersExpiration_, maxCountOfOrders_, 0), // One strategy instance magic_, "SimpleVolumesSingle", true); return(INIT_SUCCEEDED); }

Save the changes in the SimpleVolumesExpertSingle.mq5 file of the current folder.

Modifying the EA class

To avoid overloading the CVirtualAdvisor EA class, let's move the code of the TesterInit, TesterPass and OnTesterDeinit event handlers to the separate CTesterHandler class, in which we will create static methods to handle each of these events. In this case, we need to add to the CVirtualAdvisor class approximately the same code as in the main EA file:

//+------------------------------------------------------------------+ //| Class of the EA handling virtual positions (orders) | //+------------------------------------------------------------------+ class CVirtualAdvisor : public CAdvisor { ... public: ... static int TesterInit(); // OnTesterInit event handler static void TesterPass(); // OnTesterDeinit event handler static void TesterDeinit(); // OnTesterDeinit event handler }; //+------------------------------------------------------------------+ //| Initialization before starting optimization | //+------------------------------------------------------------------+ int CVirtualAdvisor::TesterInit() { return CTesterHandler::TesterInit(); } //+------------------------------------------------------------------+ //| Actions after completing the next optimization pass | //+------------------------------------------------------------------+ void CVirtualAdvisor::TesterPass() { CTesterHandler::TesterPass(); } //+------------------------------------------------------------------+ //| Actions after optimization is complete | //+------------------------------------------------------------------+ void CVirtualAdvisor::TesterDeinit() { CTesterHandler::TesterDeinit(); }

Let's also make some additions to the EA object constructor code. Move all actions from the constructor to the new Init() initialization method with future improvements in mind. This will allow us to add multiple constructors with different sets of parameters that will all use the same initialization method after a little preprocessing of the parameters.

Let's add constructors whose first argument will be either a strategy object or a strategy group object. Then we can add strategies to the EA directly in the constructor. In this case, we no longer need to call the Add() method in the OnInit() EA function.

//+------------------------------------------------------------------+ //| Class of the EA handling virtual positions (orders) | //+------------------------------------------------------------------+ class CVirtualAdvisor : public CAdvisor { protected: ... datetime m_fromDate; public: CVirtualAdvisor(CVirtualStrategy *p_strategy, ulong p_magic = 1, string p_name = "", bool p_useOnlyNewBar = false); // Constructor CVirtualAdvisor(CVirtualStrategyGroup *p_group, ulong p_magic = 1, string p_name = "", bool p_useOnlyNewBar = false); // Constructor void CVirtualAdvisor::Init(CVirtualStrategyGroup *p_group, ulong p_magic = 1, string p_name = "", bool p_useOnlyNewBar = false ); ... }; ... //+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CVirtualAdvisor::CVirtualAdvisor(CVirtualStrategy *p_strategy, ulong p_magic = 1, string p_name = "", bool p_useOnlyNewBar = false ) { CVirtualStrategy *strategies[] = {p_strategy}; Init(new CVirtualStrategyGroup(strategies), p_magic, p_name, p_useOnlyNewBar); }; //+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CVirtualAdvisor::CVirtualAdvisor(CVirtualStrategyGroup *p_group, ulong p_magic = 1, string p_name = "", bool p_useOnlyNewBar = false ) { Init(p_group, p_magic, p_name, p_useOnlyNewBar); }; //+------------------------------------------------------------------+ //| EA initialization method | //+------------------------------------------------------------------+ void CVirtualAdvisor::Init(CVirtualStrategyGroup *p_group, ulong p_magic = 1, string p_name = "", bool p_useOnlyNewBar = false ) { // Initialize the receiver with a static receiver m_receiver = CVirtualReceiver::Instance(p_magic); // Initialize the interface with the static interface m_interface = CVirtualInterface::Instance(p_magic); m_lastSaveTime = 0; m_useOnlyNewBar = p_useOnlyNewBar; m_name = StringFormat("%s-%d%s.csv", (p_name != "" ? p_name : "Expert"), p_magic, (MQLInfoInteger(MQL_TESTER) ? ".test" : "") ); m_fromDate = TimeCurrent(); Add(p_group); delete p_group; };

Save the changes in the VirtualExpert.mqh of the current folder.

Optimization event handling class

Let's now focus directly on the implementation of actions performed before the start, after the completion of the pass, and after the completion of the optimization. We will create the CTesterHandler class and add to it methods for handling the necessary events, as well as a couple of auxiliary methods placed in the closed part of the class:

//+------------------------------------------------------------------+ //| Optimization event handling class | //+------------------------------------------------------------------+ class CTesterHandler { static string s_fileName; // File name for writing frame data static void ProcessFrames(); // Handle incoming frames static string GetFrameInputs(ulong pass); // Get pass inputs public: static int TesterInit(); // Handle the optimization start in the main terminal static void TesterDeinit(); // Handle the optimization completion in the main terminal static void TesterPass(); // Handle the completion of a pass on an agent in the main terminal static void Tester(const double OnTesterValue, const string params); // Handle completion of tester pass for agent }; string CTesterHandler::s_fileName = "data.bin"; // File name for writing frame data

The event handlers for the main terminal look very simple, since we will move the main code into auxiliary functions:

//+------------------------------------------------------------------+ //| Handling the optimization start in the main terminal | //+------------------------------------------------------------------+ int CTesterHandler::TesterInit(void) { // Open / create a database DB::Open(); // If failed to open it, we do not start optimization if(!DB::IsOpen()) { return INIT_FAILED; } // Close a successfully opened database DB::Close(); return INIT_SUCCEEDED; } //+------------------------------------------------------------------+ //| Handling the optimization completion in the main terminal | //+------------------------------------------------------------------+ void CTesterHandler::TesterDeinit(void) { // Handle the latest data frames received from agents ProcessFrames(); // Close the chart with the EA running in frame collection mode ChartClose(); } //+--------------------------------------------------------------------+ //| Handling the completion of a pass on an agent in the main terminal | //+--------------------------------------------------------------------+ void CTesterHandler::TesterPass(void) { // Handle data frames received from the agent ProcessFrames(); }

The actions performed after the completion of one pass will exist in two versions:

- For the test agent. It is there that, after the passage, the necessary information will be collected and a data frame will be created for sending to the main terminal. These actions will be collected in the Tester() event handler.

- For the main terminal. Here we can receive data frames from test agents, parse the information received in the frame and enter it into the database. These actions will be collected in the TesterPass() handler.

Generating a data frame for the test agent should be performed in the EA, namely inside the OnTester handler. Since we moved its code to the EA object level (to the CVirtualAdvisor class), then this is where we need to add the CTesterHandler::Tester() method. We will pass the newly calculated value of the custom optimization criterion and a string describing the parameters of the strategy, that was used in the optimized EA, as the method parameters. To form such a string, we will use the already created ~ (tilde) for the CVirtualStrategy class objects.

//+------------------------------------------------------------------+ //| OnTester event handler | //+------------------------------------------------------------------+ double CVirtualAdvisor::Tester() { // Maximum absolute drawdown double balanceDrawdown = TesterStatistics(STAT_EQUITY_DD); // Profit double profit = TesterStatistics(STAT_PROFIT); // The ratio of possible increase in position sizes for the drawdown of 10% of fixedBalance_ double coeff = CMoney::FixedBalance() * 0.1 / balanceDrawdown; // Calculate the profit in annual terms long totalSeconds = TimeCurrent() - m_fromDate; double fittedProfit = profit * coeff * 365 * 24 * 3600 / totalSeconds ; // Perform data frame generation on the test agent CTesterHandler::Tester(fittedProfit, ~((CVirtualStrategy *) m_strategies[0])); return fittedProfit; }

In the CTesterHandler::Tester() method itself, go through all possible names of available statistical characteristics, get their values, convert them to strings and add these strings to the stats array. Why did we need to convert real numeric characteristics to strings? Only so that they could be passed in one frame with a string description of the strategy parameters. In one frame, we can pass either an array of values of one of the simple types (strings do not apply to) or a pre-created file with any data. Therefore, in order to avoid the hassle of sending two different frames (one containing numbers and the other containing strings from a file), we will convert all the data into strings, write them to a file, and send its contents in one frame:

//+------------------------------------------------------------------+ //| Handling completion of tester pass for agent | //+------------------------------------------------------------------+ void CTesterHandler::Tester(double custom, // Custom criteria string params // Description of EA parameters in the current pass ) { // Array of names of saved statistical characteristics of the pass ENUM_STATISTICS statNames[] = { STAT_INITIAL_DEPOSIT, STAT_WITHDRAWAL, STAT_PROFIT, ... }; // Array for values of statistical characteristics of the pass as strings string stats[]; ArrayResize(stats, ArraySize(statNames)); // Fill the array of values of statistical characteristics of the pass FOREACH(statNames, stats[i] = DoubleToString(TesterStatistics(statNames[i]), 2)); // Add the custom criterion value to it APPEND(stats, DoubleToString(custom, 2)); // Screen the quotes in the description of parameters just in case StringReplace(params, "'", "\\'"); // Open the file to write data for the frame int f = FileOpen(s_fileName, FILE_WRITE | FILE_TXT | FILE_ANSI); // Write statistical characteristics FOREACH(stats, FileWriteString(f, stats[i] + ",")); // Write a description of the EA parameters FileWriteString(f, StringFormat("'%s'", params)); // Close the file FileClose(f); // Create a frame with data from the recorded file and send it to the main terminal if(!FrameAdd("", 0, 0, s_fileName)) { PrintFormat(__FUNCTION__" | ERROR: Frame add error: %d", GetLastError()); } }

Finally, let's consider an auxiliary method that will accept data frames and save the information from them to the database. In this method, we receive in a loop all incoming frames that have not yet been handled at the current moment. From each frame, we obtain data in the form of a character array and convert them into a string. Next, we form a string with the names and values of the parameters of the pass with the given index. We use the obtained values to form an SQL query to insert a new row into the passes table in our database. Add the created SQL query to the SQL query array.

After handling all currently received data frames in this way, we execute all SQL queries from the array within a single transaction.

//+------------------------------------------------------------------+ //| Handling incoming frames | //+------------------------------------------------------------------+ void CTesterHandler::ProcessFrames(void) { // Open the database DB::Open(); // Variables for reading data from frames string name; // Frame name (not used) ulong pass; // Frame pass index long id; // Frame type ID (not used) double value; // Single frame value (not used) uchar data[]; // Frame data array as a character array string values; // Frame data as a string string inputs; // String with names and values of pass parameters string query; // A single SQL query string string queries[]; // SQL queries for adding records to the database // Go through frames and read data from them while(FrameNext(pass, name, id, value, data)) { // Convert the array of characters read from the frame into a string values = CharArrayToString(data); // Form a string with names and values of the pass parameters inputs = GetFrameInputs(pass); // Form an SQL query from the received data query = StringFormat("INSERT INTO passes " "VALUES (NULL, %d, %s,\n'%s',\n'%s');", pass, values, inputs, TimeToString(TimeLocal(), TIME_DATE | TIME_SECONDS)); // Add it to the SQL query array APPEND(queries, query); } // Execute all requests DB::ExecuteTransaction(queries); // Close the database DB::Close(); }

The GetFrameInputs() auxiliary method for forming a string with names and values of input variables of the pass has been taken from the AlgoBook and slightly supplemented to suit our needs.

Save the obtained code in the TesterHandler.mqh file of the current folder.

Checking operation

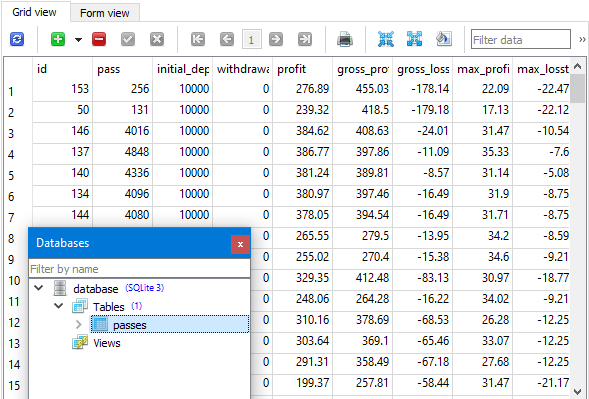

To test the functionality, let's run optimization with a small number of parameters to be iterated over a relatively short time period. After the optimization process is completed, we can look at the results in the strategy tester and in the created database.

Fig. 1. Optimization results in the strategy tester

Fig. 2. Optimization results in the database

As we can see, the database results match the results in the tester: with the same sorting by user criteria, we observe the same sequence of profit values in both cases. The best pass reports that the expected profit may exceed USD 5000 within a year with the initial deposit of USD 10,000 and a maximum achievable drawdown of 10% of the initial deposit (USD 1000). Currently, however, we are not so interested in the quantitative characteristics of the optimization results as in the fact that they can now be stored in a database.

Conclusion

So, we are one step closer to our goal. We managed to save the results of the conducted optimizations of the EA parameters to our database. In this way, we have provided the foundation for further automated implementation of the second stage of the EA development.

There are still quite a few questions left behind the scenes. Many things had to be postponed for the future, since their implementation would require significant costs. But having received the current results, we can more clearly formulate the direction of further project development.

The implemented saving currently works only for one optimization process in the sense that we save information about the passes, but it is still difficult to extract groups of strings related to one optimization process from them. To do this, we will need to make changes to the database structure, which is now made extremely simple. In the future, we will try to automate the launch of several sequential optimization processes with preliminary assignment of different options for the parameters to be optimized.

Thank you for your attention! See you soon!

Translated from Russian by MetaQuotes Ltd.

Original article: https://www.mql5.com/ru/articles/14680

Warning: All rights to these materials are reserved by MetaQuotes Ltd. Copying or reprinting of these materials in whole or in part is prohibited.

This article was written by a user of the site and reflects their personal views. MetaQuotes Ltd is not responsible for the accuracy of the information presented, nor for any consequences resulting from the use of the solutions, strategies or recommendations described.

Creating an MQL5-Telegram Integrated Expert Advisor (Part 5): Sending Commands from Telegram to MQL5 and Receiving Real-Time Responses

Creating an MQL5-Telegram Integrated Expert Advisor (Part 5): Sending Commands from Telegram to MQL5 and Receiving Real-Time Responses

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use