Data Science and ML (Part 32): Keeping your AI models updated, Online Learning

Contents

- What is online learning?

- Benefits of online learning

- Online learning infrastructure for MetaTrader 5

- Automating the training and deployment process

- Online learning for deep learning AI models

- Incremental Machine learning

- Conclusion

What is Online Learning?

Online machine learning is a machine learning method in which the model incrementally learns from a stream of data points in real time. It’s a dynamic process that adapts its predictive algorithm over time, allowing the model to change as new data arrives. This method is incredibly significant in rapidly evolving data-rich environments such as in trading data as it can provide timely and accurate predictions.

While working with the trading data, it is always hard to determine the right time to update your models and how often for instance, if you have AI models trained on Bitcoin for the last year, the recent information might turn out to be outliers for a machine learning model considering this cryptocurrency just hit the new highest price last week.

Unlike forex instruments which usually go up and down within specific ranges historically, instruments like NASDAQ 100, S&P 500 and others of their kind and stocks usually tends to increase and hit new peak values.

Online learning is not only for the fear of the old training information becoming obsolete but also for the sake of keeping the model updated with recent information which might have some impact on what's currently happening in the market.

Benefits of Online Learning

- Adaptability

Just like the cyclists learning as they go, online machine learning can adapt to new patterns in the data potentially improving its performance over time. - Scalability

Some online learning methods for some models processes data one at a time. This makes this technique safer for tight computational resources that most of us have, this can finally help in scaling models that depend on big data. - Real-time predictions

Unlike batch learning which might be outdated by the time it's implemented, online learning provides real-time insights which can be critical in many trading applications. - Efficiency

Incremental machine learning allows for continuous learning and updating of models, which can lead to a faster and more cost-efficient training process.

Now that we understand several benefits of this technique, Let's see the infrastructure it takes to make effective online learning in MetaTrader 5.

Online Learning Infrastructure for MetaTrader 5

Since our final goal is to make AI models useful for trading purposes in MetaTrader 5, it takes a different Online learning infrastructure than that usually seen in Python-based applications.

Step 01: Python Client

Inside a Python client (script) is where we want to build AI models based on the trading data received from MetaTrader 5.

Using MetaTrader 5 (python library), we start by initializing the platform.

import pandas as pd import numpy as np import MetaTrader5 as mt5 from datetime import datetime if not mt5.initialize(): # Initialize the MetaTrader 5 platform print("initialize() failed") mt5.shutdown()

After MetaTrader 5 platform initialization, we can obtain trading information from it using the copy_rates_from_pos method.

def getData(start = 1, bars = 1000): rates = mt5.copy_rates_from_pos("EURUSD", mt5.TIMEFRAME_H1, start, bars) if len(rates) < bars: # if the received information is less than specified print("Failed to copy rates from MetaTrader 5, error = ",mt5.last_error()) # create a pnadas DataFrame out of the obtained data df_rates = pd.DataFrame(rates) return df_rates

We can print to see the obtained information.

print("Trading info:\n",getData(1, 100)) # get 100 bars starting at the recent closed bar

Ouputs

time open high low close tick_volume spread real_volume 0 1731351600 1.06520 1.06564 1.06451 1.06491 1688 0 0 1 1731355200 1.06491 1.06519 1.06460 1.06505 1607 0 0 2 1731358800 1.06505 1.06573 1.06495 1.06512 1157 0 0 3 1731362400 1.06512 1.06564 1.06512 1.06557 1112 0 0 4 1731366000 1.06557 1.06579 1.06553 1.06557 776 0 0 .. ... ... ... ... ... ... ... ... 95 1731693600 1.05354 1.05516 1.05333 1.05513 5125 0 0 96 1731697200 1.05513 1.05600 1.05472 1.05486 3966 0 0 97 1731700800 1.05487 1.05547 1.05386 1.05515 2919 0 0 98 1731704400 1.05515 1.05522 1.05359 1.05372 2651 0 0 99 1731708000 1.05372 1.05379 1.05164 1.05279 2977 0 0 [100 rows x 8 columns]

We use the copy_rates_from_pos method as it allows us to access the recenlyt closed bar placed at the index of 1, this is very useful compared to accessing using dates that are fixed.

We can always be confident that by copying from the bar located at the index of 1, we always get the information starting at the recently closed bar all the way to some specified number of bars we want in.

After receiving this information, we can do the typical machine learning stuff for this data.

We create a separate file for our model, by putting each model in its separate file, we make it easy to call these models in the "main.py" file where all the key processes and functions are deployed.

File catboost_models.py

from catboost import CatBoostClassifier from sklearn.metrics import accuracy_score from onnx.helper import get_attribute_value from skl2onnx import convert_sklearn, update_registered_converter from sklearn.pipeline import Pipeline from skl2onnx.common.shape_calculator import ( calculate_linear_classifier_output_shapes, ) # noqa from skl2onnx.common.data_types import ( FloatTensorType, Int64TensorType, guess_tensor_type, ) from skl2onnx._parse import _apply_zipmap, _get_sklearn_operator_name from catboost.utils import convert_to_onnx_object # Example initial data (X_initial, y_initial are your initial feature matrix and target) class CatBoostClassifierModel(): def __init__(self, X_train, X_test, y_train, y_test): self.X_train = X_train self.X_test = X_test self.y_train = y_train self.y_test = y_test self.model = None def train(self, iterations=100, depth=6, learning_rate=0.1, loss_function="CrossEntropy", use_best_model=True): # Initialize the CatBoost model params = { "iterations": iterations, "depth": depth, "learning_rate": learning_rate, "loss_function": loss_function, "use_best_model": use_best_model } self.model = Pipeline([ # wrap a catboost classifier in sklearn pipeline | good practice (not necessary tho :)) ("catboost", CatBoostClassifier(**params)) ]) # Testing the model self.model.fit(X=self.X_train, y=self.y_train, catboost__eval_set=(self.X_test, self.y_test)) y_pred = self.model.predict(self.X_test) print("Model's accuracy on out-of-sample data = ",accuracy_score(self.y_test, y_pred)) # a function for saving the trained CatBoost model to ONNX format def to_onnx(self, model_name): update_registered_converter( CatBoostClassifier, "CatBoostCatBoostClassifier", calculate_linear_classifier_output_shapes, self.skl2onnx_convert_catboost, parser=self.skl2onnx_parser_castboost_classifier, options={"nocl": [True, False], "zipmap": [True, False, "columns"]}, ) model_onnx = convert_sklearn( self.model, "pipeline_catboost", [("input", FloatTensorType([None, self.X_train.shape[1]]))], target_opset={"": 12, "ai.onnx.ml": 2}, ) # And save. with open(model_name, "wb") as f: f.write(model_onnx.SerializeToString())

For more information about this CatBoost model deployed, kindly refer to this article. I have used the CatBoost model as an example, feel free to use any of your preferred models.

Now that we have this class to help us with initializing, training, and saving the catboost model. Let us deploy this model in the "main.py" file.

File: main.py

Again, we start by receiving the data from the MetaTrader 5 desktop app.

data = getData(start=1, bars=1000)

If you look closely at the CatBoost model, you'll see that it is a classifier model. We are yet to have the target variable for this classifier, let's make one.

# Preparing the target variable data["future_open"] = data["open"].shift(-1) # shift one bar into the future data["future_close"] = data["close"].shift(-1) target = [] for row in range(data.shape[0]): if data["future_close"].iloc[row] > data["future_open"].iloc[row]: # bullish signal target.append(1) else: # bearish signal target.append(0) data["target"] = target # add the target variable to the dataframe data = data.dropna() # drop empty rows

We can drop all future variables and other features with plenty of zero values from the X 2D array, and assign the "target" variable to the y 1D array.

X = data.drop(columns = ["spread","real_volume","future_close","future_open","target"]) y = data["target"]

We then split the information into training and validation samples, initialize the CatBoost model with the data from the market, and train it.

X_train, X_test, y_train, y_test = train_test_split(X, y, train_size=0.7, random_state=42) catboost_model = catboost_models.CatBoostClassifierModel(X_train, X_test, y_train, y_test) catboost_model.train()

Finally, we save this model in ONNX format in a Common MetaTrader 5 directory.

Step 02: Common Folder

Using the MetaTrader 5 Python, we can get the information on the common path.

terminal_info_dict = mt5.terminal_info()._asdict()

common_path = terminal_info_dict["commondata_path"] This is where we want to save all trained AI models from this Python client we have.

When accessing the common folder using MQL5, it usually refers to a "Files" sub-folder found under the common folder. To make it easier to access these files from an MQL5 standpoint, we have to save the models in that subfolder.

# Save models in a specific location under the common parent folder models_path = os.path.join(common_path, "Files") if not os.path.exists(models_path): #if the folder exists os.makedirs(models_path) # Create the folder if it doesn't exist catboost_model.to_onnx(model_name=os.path.join(models_path, "catboost.H1.onnx"))

Finally, we have to wrap all these lines of code in a single function to make it easier to carry out all these different processes whenever we want.

def trainAndSaveCatBoost(): data = getData(start=1, bars=1000) # Check if we were able to receive some data if (len(data)<=0): print("Failed to obtain data from Metatrader5, error = ",mt5.last_error()) mt5.shutdown() # Preparing the target variable data["future_open"] = data["open"].shift(-1) # shift one bar into the future data["future_close"] = data["close"].shift(-1) target = [] for row in range(data.shape[0]): if data["future_close"].iloc[row] > data["future_open"].iloc[row]: # bullish signal target.append(1) else: # bearish signal target.append(0) data["target"] = target # add the target variable to the dataframe data = data.dropna() # drop empty rows X = data.drop(columns = ["spread","real_volume","future_close","future_open","target"]) y = data["target"] X_train, X_test, y_train, y_test = train_test_split(X, y, train_size=0.7, random_state=42) catboost_model = catboost_models.CatBoostClassifierModel(X_train, X_test, y_train, y_test) catboost_model.train() # Save models in a specific location under the common parent folder models_path = os.path.join(common_path, "Files") if not os.path.exists(models_path): #if the folder exists os.makedirs(models_path) # Create the folder if it doesn't exist catboost_model.to_onnx(model_name=os.path.join(models_path, "catboost.H1.onnx"))

Let's call this function then and see what it does.

trainAndSaveCatBoost()

exit() # stop the script Outcome

0: learn: 0.6916088 test: 0.6934968 best: 0.6934968 (0) total: 163ms remaining: 16.1s 1: learn: 0.6901684 test: 0.6936087 best: 0.6934968 (0) total: 168ms remaining: 8.22s 2: learn: 0.6888965 test: 0.6931576 best: 0.6931576 (2) total: 175ms remaining: 5.65s 3: learn: 0.6856524 test: 0.6927187 best: 0.6927187 (3) total: 184ms remaining: 4.41s 4: learn: 0.6843646 test: 0.6927737 best: 0.6927187 (3) total: 196ms remaining: 3.72s ... ... ... 96: learn: 0.5992419 test: 0.6995323 best: 0.6927187 (3) total: 915ms remaining: 28.3ms 97: learn: 0.5985751 test: 0.7002011 best: 0.6927187 (3) total: 924ms remaining: 18.9ms 98: learn: 0.5978617 test: 0.7003299 best: 0.6927187 (3) total: 928ms remaining: 9.37ms 99: learn: 0.5968786 test: 0.7010596 best: 0.6927187 (3) total: 932ms remaining: 0us bestTest = 0.6927187021 bestIteration = 3 Shrink model to first 4 iterations. Model's accuracy on out-of-sample data = 0.5

The .onnx file can be seen under Common\Files.

Step 03: MetaTrader 5

Now in MetaTrader 5, we have to load this model saved in ONNX format.

We start by importing the library to help us with this task.

Inside "Online Learning Catboost.mq5"

#include <CatBoost.mqh> CCatBoost *catboost; input string model_name = "catboost.H1.onnx"; input string symbol = "EURUSD"; input ENUM_TIMEFRAMES timeframe = PERIOD_H1; string common_path;

The first thing we want to do inside the Oninit function is to check whether the file exists in the common folder, if it doesn't exist, this could indicate that the model wasn't trained.

After that, we initialize the ONNX model by passing the ONNX_COMMON_FOLDER flag to explicitly load the model from the "Common folder".

int OnInit() { //--- Check if the model file exists if (!FileIsExist(model_name, FILE_COMMON)) { printf("%s Onnx file doesn't exist",__FUNCTION__); return INIT_FAILED; } //--- Initialize a catboost model catboost = new CCatBoost(); if (!catboost.Init(model_name, ONNX_COMMON_FOLDER)) { printf("%s failed to initialize the catboost model, error = %d",__FUNCTION__,GetLastError()); return INIT_FAILED; } //--- }

To use this loaded model to make predictions, we can go back to the Python script and check what features were used for training after some were dropped.

The same features and in the same order must be collected in MQL5.

Python code "main.py" file.

X = data.drop(columns = ["spread","real_volume","future_close","future_open","target"]) y = data["target"] print(X.head())

Outcome

time open high low close tick_volume 0 1726772400 1.11469 1.11584 1.11453 1.11556 3315 1 1726776000 1.11556 1.11615 1.11525 1.11606 2812 2 1726779600 1.11606 1.11680 1.11606 1.11656 2309 3 1726783200 1.11656 1.11668 1.11590 1.11622 2667 4 1726786800 1.11622 1.11644 1.11605 1.11615 1166

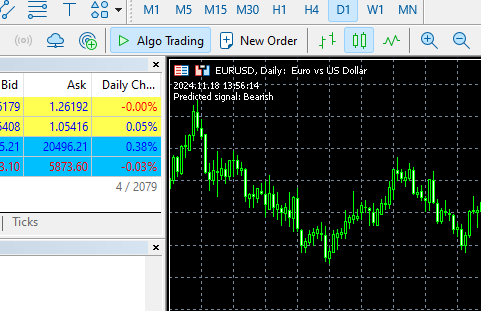

Now, let's obtain this information inside the OnTick function and call the predict_bin function which predicts classes.

This function will predict two classes that were seen in the target variable we prepared in the Python client. 0 (bullish), 1 (bearish).

void OnTick() { //--- MqlRates rates[]; CopyRates(symbol, timeframe, 1, 1, rates); //copy the recent closed bar information vector x = { (double)rates[0].time, rates[0].open, rates[0].high, rates[0].low, rates[0].close, (double)rates[0].tick_volume}; Comment(TimeCurrent(),"\nPredicted signal: ",catboost.predict_bin(x)==0?"Bearish":"Bullish");// if the predicted signal is 0 it means a bearish signal, otherwise it is a bullish signal }

Outcome

Automating the Training and Deployment Process

We were able to train and deploy the model in MetaTrader 5 but, this isn't what we want, our main goal is to automate the entire process.

Inside the Python virtual environment, we have to install the schedule library.

$ pip install schedule

This small module can help in scheduling when we want a specific function to be executed. Since we already wrapped the code for collecting data, training, and saving the model in one function, let's schedule this function to be called after every (one) minute.

schedule.every(1).minute.do(trainAndSaveCatBoost) #schedule catboost training # Keep the script running to execute the scheduled tasks while True: schedule.run_pending() time.sleep(60) # Wait for 1 minute before checking again

This scheduling thing works like a charm :)

In our main Expert Advisor, we also schedule when and how often our EA should load the model from the common directory, in doing so, we effectively update the model for our trading robot.

We can use the OnTimer function which also works like a charm :)

int OnInit() { //--- Check if the model file exists .... //--- Initialize a catboost model .... //--- if (!EventSetTimer(60)) //Execute the OnTimer function after every 60 seconds { printf("%s failed to set the event timer, error = %d",__FUNCTION__,GetLastError()); return INIT_FAILED; } //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Expert deinitialization function | //+------------------------------------------------------------------+ void OnDeinit(const int reason) { //--- if (CheckPointer(catboost) != POINTER_INVALID) delete catboost; } //+------------------------------------------------------------------+ //| Expert tick function | //+------------------------------------------------------------------+ void OnTick() { //--- .... } //+------------------------------------------------------------------+ //| | //+------------------------------------------------------------------+ void OnTimer(void) { if (CheckPointer(catboost) != POINTER_INVALID) delete catboost; //--- Load the new model after deleting the prior one from memory catboost = new CCatBoost(); if (!catboost.Init(model_name, ONNX_COMMON_FOLDER)) { printf("%s failed to initialize the catboost model, error = %d",__FUNCTION__,GetLastError()); return; } printf("%s New model loaded",TimeToString(TimeCurrent(), TIME_DATE|TIME_MINUTES)); }

Outcome

HO 0 13:14:00.648 Online Learning Catboost (EURUSD,D1) 2024.11.18 12:14 New model loaded FK 0 13:15:55.388 Online Learning Catboost (GBPUSD,H1) 2024.11.18 12:15 New model loaded JG 0 13:16:55.380 Online Learning Catboost (GBPUSD,H1) 2024.11.18 12:16 New model loaded MP 0 13:17:55.376 Online Learning Catboost (GBPUSD,H1) 2024.11.18 12:17 New model loaded JM 0 13:18:55.377 Online Learning Catboost (GBPUSD,H1) 2024.11.18 12:18 New model loaded PF 0 13:19:55.368 Online Learning Catboost (GBPUSD,H1) 2024.11.18 12:19 New model loaded CR 0 13:20:55.387 Online Learning Catboost (GBPUSD,H1) 2024.11.18 12:20 New model loaded NO 0 13:21:55.377 Online Learning Catboost (GBPUSD,H1) 2024.11.18 12:21 New model loaded LH 0 13:22:55.379 Online Learning Catboost (GBPUSD,H1) 2024.11.18 12:22 New model loaded

Now that we have seen how you can schedule the training process and keep the new models in sync with the ExpertAdvisor in MetaTrader 5. While the process is easy to implement for most machine learning techniques, it could be a challenging process when working with deep learning models such as Recurrent Neural Networks(RNNs), which can't be contained inside the Sklearn pipeline which makes our life easier when working with various machine learning models.

Let us see how you can apply this technique when working with a Gated Recurrent Unit(GRU) which is a special form of a recurrent neural network.

Online Learning for Deep Learning AI models

In Python Client

We apply the typical machine learning stuff inside the GRUClassifier class. For more information on GRU kindly refer to this article.

After training the model we save it to ONNX, this time we also save the StandardScaler's information in binary files, this will help us later in similarly normalizing the new data in MQL5 as it currently stands in Python.

File gru_models.py

import numpy as np import tensorflow as tf from tensorflow.keras.models import Sequential from tensorflow.keras.layers import GRU, Dense, Input, Dropout from keras.callbacks import EarlyStopping from keras.optimizers import Adam import tf2onnx class GRUClassifier(): def __init__(self, time_step, X_train, X_test, y_train, y_test): self.X_train = X_train self.X_test = X_test self.y_train = y_train self.y_test = y_test self.model = None self.time_step = time_step self.classes_in_y = np.unique(self.y_train) def train(self, learning_rate=0.001, layers=2, neurons = 50, activation="relu", batch_size=32, epochs=100, loss="binary_crossentropy", verbose=0): self.model = Sequential() self.model.add(Input(shape=(self.time_step, self.X_train.shape[2]))) self.model.add(GRU(units=neurons, activation=activation)) # input layer for layer in range(layers): # dynamically adjusting the number of hidden layers self.model.add(Dense(units=neurons, activation=activation)) self.model.add(Dropout(0.5)) self.model.add(Dense(units=len(self.classes_in_y), activation='softmax', name='output_layer')) # the output layer # Compile the model adam_optimizer = Adam(learning_rate=learning_rate) self.model.compile(optimizer=adam_optimizer, loss=loss, metrics=['accuracy']) early_stopping = EarlyStopping(monitor='val_loss', patience=10, restore_best_weights=True) history = self.model.fit(self.X_train, self.y_train, epochs=epochs, batch_size=batch_size, validation_data=(self.X_test, self.y_test), callbacks=[early_stopping], verbose=verbose) val_loss, val_accuracy = self.model.evaluate(self.X_test, self.y_test, verbose=verbose) print("Gru accuracy on validation sample = ",val_accuracy) def to_onnx(self, model_name, standard_scaler): # Convert the Keras model to ONNX spec = (tf.TensorSpec((None, self.time_step, self.X_train.shape[2]), tf.float16, name="input"),) self.model.output_names = ['outputs'] onnx_model, _ = tf2onnx.convert.from_keras(self.model, input_signature=spec, opset=13) # Save the ONNX model to a file with open(model_name, "wb") as f: f.write(onnx_model.SerializeToString()) # Save the mean and scale parameters to binary files standard_scaler.mean_.tofile(f"{model_name.replace('.onnx','')}.standard_scaler_mean.bin") standard_scaler.scale_.tofile(f"{model_name.replace('.onnx','')}.standard_scaler_scale.bin")

Inside the "main.py" file, we create a function responsible for everything we want to happen with the GRU model.

def trainAndSaveGRU(): data = getData(start=1, bars=1000) # Preparing the target variable data["future_open"] = data["open"].shift(-1) data["future_close"] = data["close"].shift(-1) target = [] for row in range(data.shape[0]): if data["future_close"].iloc[row] > data["future_open"].iloc[row]: target.append(1) else: target.append(0) data["target"] = target data = data.dropna() # Check if we were able to receive some data if (len(data)<=0): print("Failed to obtain data from Metatrader5, error = ",mt5.last_error()) mt5.shutdown() X = data.drop(columns = ["spread","real_volume","future_close","future_open","target"]) y = data["target"] X_train, X_test, y_train, y_test = train_test_split(X, y, train_size=0.7, shuffle=False) ########### Preparing data for timeseries forecasting ############### time_step = 10 scaler = StandardScaler() X_train = scaler.fit_transform(X_train) X_test = scaler.transform(X_test) x_train_seq, y_train_seq = create_sequences(X_train, y_train, time_step) x_test_seq, y_test_seq = create_sequences(X_test, y_test, time_step) ###### One HOt encoding ####### y_train_encoded = to_categorical(y_train_seq) y_test_encoded = to_categorical(y_test_seq) gru = gru_models.GRUClassifier(time_step=time_step, X_train= x_train_seq, y_train= y_train_encoded, X_test= x_test_seq, y_test= y_test_encoded ) gru.train( batch_size=64, learning_rate=0.001, activation = "relu", epochs=1000, loss="binary_crossentropy", layers = 2, neurons = 50, verbose=1 ) # Save models in a specific location under the common parent folder models_path = os.path.join(common_path, "Files") if not os.path.exists(models_path): #if the folder exists os.makedirs(models_path) # Create the folder if it doesn't exist gru.to_onnx(model_name=os.path.join(models_path, "gru.H1.onnx"), standard_scaler=scaler)

Finally, we can schedule how often this trainAndSaveGRU function should be called into action, similarly to how we scheduled for the CatBoost function.

schedule.every(1).minute.do(trainAndSaveGRU) #scheduled GRU training

Outcome

Epoch 1/1000 11/11 ━━━━━━━━━━━━━━━━━━━━ 7s 87ms/step - accuracy: 0.4930 - loss: 0.6985 - val_accuracy: 0.5000 - val_loss: 0.6958 Epoch 2/1000 11/11 ━━━━━━━━━━━━━━━━━━━━ 0s 16ms/step - accuracy: 0.4847 - loss: 0.6957 - val_accuracy: 0.4931 - val_loss: 0.6936 Epoch 3/1000 11/11 ━━━━━━━━━━━━━━━━━━━━ 0s 17ms/step - accuracy: 0.5500 - loss: 0.6915 - val_accuracy: 0.4897 - val_loss: 0.6934 Epoch 4/1000 11/11 ━━━━━━━━━━━━━━━━━━━━ 0s 16ms/step - accuracy: 0.4910 - loss: 0.6923 - val_accuracy: 0.4690 - val_loss: 0.6938 Epoch 5/1000 11/11 ━━━━━━━━━━━━━━━━━━━━ 0s 16ms/step - accuracy: 0.5538 - loss: 0.6910 - val_accuracy: 0.4897 - val_loss: 0.6935 Epoch 6/1000 11/11 ━━━━━━━━━━━━━━━━━━━━ 0s 20ms/step - accuracy: 0.5037 - loss: 0.6953 - val_accuracy: 0.4931 - val_loss: 0.6937 Epoch 7/1000 ... ... ... 11/11 ━━━━━━━━━━━━━━━━━━━━ 0s 22ms/step - accuracy: 0.4964 - loss: 0.6952 - val_accuracy: 0.4793 - val_loss: 0.6940 Epoch 20/1000 11/11 ━━━━━━━━━━━━━━━━━━━━ 0s 19ms/step - accuracy: 0.5285 - loss: 0.6914 - val_accuracy: 0.4793 - val_loss: 0.6949 Epoch 21/1000 11/11 ━━━━━━━━━━━━━━━━━━━━ 0s 17ms/step - accuracy: 0.5224 - loss: 0.6935 - val_accuracy: 0.4966 - val_loss: 0.6942 Epoch 22/1000 11/11 ━━━━━━━━━━━━━━━━━━━━ 0s 21ms/step - accuracy: 0.5009 - loss: 0.6936 - val_accuracy: 0.5103 - val_loss: 0.6933 10/10 ━━━━━━━━━━━━━━━━━━━━ 0s 19ms/step - accuracy: 0.4925 - loss: 0.6938 Gru accuracy on validation sample = 0.5103448033332825

In MetaTrader 5

We start by loading the libraries to help us with the task of loading the GRU model and the standard scaler.

#include <preprocessing.mqh> #include <GRU.mqh> CGRU *gru; StandardizationScaler *scaler; //--- Arrays for temporary storage of the scaler values double scaler_mean[], scaler_std[]; input string model_name = "gru.H1.onnx"; string mean_file; string std_file;

The first thing we want to do in the OnInit function is to get the names of the scaler binary files, we applied this same principle when creating these files.

string base_name__ = model_name; if (StringReplace(base_name__,".onnx","")<0) { printf("%s Failed to obtain the parent name for the scaler files, error = %d",__FUNCTION__,GetLastError()); return INIT_FAILED; } mean_file = base_name__ + ".standard_scaler_mean.bin"; std_file = base_name__ + ".standard_scaler_scale.bin";

Finally, we proceed to load the GRU model in ONNX format from the common folder, we also read the scaler files in binary format by assigning their values in the scaler_mean and scaler_std arrays.

int OnInit() { string base_name__ = model_name; if (StringReplace(base_name__,".onnx","")<0) //we followed this same file patterns while saving the binary files in python client { printf("%s Failed to obtain the parent name for the scaler files, error = %d",__FUNCTION__,GetLastError()); return INIT_FAILED; } mean_file = base_name__ + ".standard_scaler_mean.bin"; std_file = base_name__ + ".standard_scaler_scale.bin"; //--- Check if the model file exists if (!FileIsExist(model_name, FILE_COMMON)) { printf("%s Onnx file doesn't exist",__FUNCTION__); return INIT_FAILED; } //--- Initialize the GRU model from the common folder gru = new CGRU(); if (!gru.Init(model_name, ONNX_COMMON_FOLDER)) { printf("%s failed to initialize the gru model, error = %d",__FUNCTION__,GetLastError()); return INIT_FAILED; } //--- Read the scaler files if (!readArray(mean_file, scaler_mean) || !readArray(std_file, scaler_std)) { printf("%s failed to read scaler information",__FUNCTION__); return INIT_FAILED; } scaler = new StandardizationScaler(scaler_mean, scaler_std); //Load the scaler class by populating it with values //--- Set the timer if (!EventSetTimer(60)) { printf("%s failed to set the event timer, error = %d",__FUNCTION__,GetLastError()); return INIT_FAILED; } //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Expert deinitialization function | //+------------------------------------------------------------------+ void OnDeinit(const int reason) { //--- if (CheckPointer(gru) != POINTER_INVALID) delete gru; if (CheckPointer(scaler) != POINTER_INVALID) delete scaler; }

We schedule the process of reading the scaler and model files from the common folder in the OnTimer function.

void OnTimer(void) { //--- Delete the existing pointers in memory as the new ones are about to be created if (CheckPointer(gru) != POINTER_INVALID) delete gru; if (CheckPointer(scaler) != POINTER_INVALID) delete scaler; //--- if (!readArray(mean_file, scaler_mean) || !readArray(std_file, scaler_std)) { printf("%s failed to read scaler information",__FUNCTION__); return; } scaler = new StandardizationScaler(scaler_mean, scaler_std); gru = new CGRU(); if (!gru.Init(model_name, ONNX_COMMON_FOLDER)) { printf("%s failed to initialize the gru model, error = %d",__FUNCTION__,GetLastError()); return; } printf("%s New model loaded",TimeToString(TimeCurrent(), TIME_DATE|TIME_MINUTES)); }

Outcome

II 0 14:49:35.920 Online Learning GRU (GBPUSD,H1) 2024.11.18 13:49 New model loaded QP 0 14:50:35.886 Online Learning GRU (GBPUSD,H1) Initilaizing ONNX model... MF 0 14:50:35.919 Online Learning GRU (GBPUSD,H1) ONNX model Initialized IJ 0 14:50:35.919 Online Learning GRU (GBPUSD,H1) 2024.11.18 13:50 New model loaded EN 0 14:51:35.894 Online Learning GRU (GBPUSD,H1) Initilaizing ONNX model... JD 0 14:51:35.913 Online Learning GRU (GBPUSD,H1) ONNX model Initialized EL 0 14:51:35.913 Online Learning GRU (GBPUSD,H1) 2024.11.18 13:51 New model loaded NM 0 14:52:35.885 Online Learning GRU (GBPUSD,H1) Initilaizing ONNX model... KK 0 14:52:35.915 Online Learning GRU (GBPUSD,H1) ONNX model Initialized QQ 0 14:52:35.915 Online Learning GRU (GBPUSD,H1) 2024.11.18 13:52 New model loaded DK 0 14:53:35.899 Online Learning GRU (GBPUSD,H1) Initilaizing ONNX model... HI 0 14:53:35.935 Online Learning GRU (GBPUSD,H1) ONNX model Initialized MS 0 14:53:35.935 Online Learning GRU (GBPUSD,H1) 2024.11.18 13:53 New model loaded DI 0 14:54:35.885 Online Learning GRU (GBPUSD,H1) Initilaizing ONNX model... IL 0 14:54:35.908 Online Learning GRU (GBPUSD,H1) ONNX model Initialized QE 0 14:54:35.908 Online Learning GRU (GBPUSD,H1) 2024.11.18 13:54 New model loaded

To receive the predictions from the GRU model, we have to consider the timestep value which helps Recurrent Neural Networks(RNNs) understand temporal dependencies in the data.

We used a timestep value of ten(10) inside the function "trainAndSaveGRU".

def trainAndSaveGRU(): data = getData(start=1, bars=1000) .... .... time_step = 10

Let's collect the last 10 bars (timesteps) from history starting from the recently closed bar in MQL5. (this is how it is supposed to be)

input int time_step = 10;

void OnTick() { //--- MqlRates rates[]; CopyRates(symbol, timeframe, 1, time_step, rates); //copy the recent closed bar information vector classes = {0,1}; //Beware of how classes are organized in the target variable. use numpy.unique(y) to determine this array matrix X = matrix::Zeros(time_step, 6); // 6 columns for (int i=0; i<time_step; i++) { vector row = { (double)rates[i].time, rates[i].open, rates[i].high, rates[i].low, rates[i].close, (double)rates[i].tick_volume}; X.Row(row, i); } X = scaler.transform(X); //it's important to normalize the data Comment(TimeCurrent(),"\nPredicted signal: ",gru.predict_bin(X, classes)==0?"Bearish":"Bullish");// if the predicted signal is 0 it means a bearish signal, otherwise it is a bullish signal }

Outcome

Incremental Machine Learning

Some models are more proficient and robust than others when it comes to the training methods. When you are searching for "Online machine learning" on the internet, most folks say that it is a process through which small batches of data are retrained back to the model for the bigger training goal.

The problem with this is that many models do not support or work well when given a small sample of data.

Modern machine learning techniques like CatBoost comes with incremental learning in mind. This training method can be used for Online learning and it can help save a lot of memory when working with big data, as data can be split into small chunks which can be re-trained back to the initial model.

def getData(start = 1, bars = 1000): rates = mt5.copy_rates_from_pos("EURUSD", mt5.TIMEFRAME_H1, start, bars) df_rates = pd.DataFrame(rates) return df_rates def trainIncrementally(): # CatBoost model clf = CatBoostClassifier( task_type="CPU", iterations=2000, learning_rate=0.2, max_depth=1, verbose=0, ) # Get big data big_data = getData(1, 10000) # Split into chunks of 1000 samples chunk_size = 1000 chunks = [big_data[i:i + chunk_size].copy() for i in range(0, len(big_data), chunk_size)] # Use .copy() here for i, chunk in enumerate(chunks): # Preparing the target variable chunk["future_open"] = chunk["open"].shift(-1) chunk["future_close"] = chunk["close"].shift(-1) target = [] for row in range(chunk.shape[0]): if chunk["future_close"].iloc[row] > chunk["future_open"].iloc[row]: target.append(1) else: target.append(0) chunk["target"] = target chunk = chunk.dropna() # Check if we were able to receive some data if (len(chunk)<=0): print("Failed to obtain chunk from Metatrader5, error = ",mt5.last_error()) mt5.shutdown() X = chunk.drop(columns = ["spread","real_volume","future_close","future_open","target"]) y = chunk["target"] X_train, X_val, y_train, y_val = train_test_split(X, y, train_size=0.8, random_state=42) if i == 0: # Initial training, training the model for the first time clf.fit(X_train, y_train, eval_set=(X_val, y_val)) y_pred = clf.predict(X_val) print(f"---> Acc score: {accuracy_score(y_pred=y_pred, y_true=y_val)}") else: # Incremental training by using the intial trained model clf.fit(X_train, y_train, init_model="model.cbm", eval_set=(X_val, y_val)) y_pred = clf.predict(X_val) print(f"---> Acc score: {accuracy_score(y_pred=y_pred, y_true=y_val)}") # Save the model clf.save_model("model.cbm") print(f"Chunk {i + 1}/{len(chunks)} processed and model saved.")

Outcome

---> Acc score: 0.555 Chunk 1/10 processed and model saved. ---> Acc score: 0.505 Chunk 2/10 processed and model saved. ---> Acc score: 0.55 Chunk 3/10 processed and model saved. ---> Acc score: 0.565 Chunk 4/10 processed and model saved. ---> Acc score: 0.495 Chunk 5/10 processed and model saved. ---> Acc score: 0.55 Chunk 6/10 processed and model saved. ---> Acc score: 0.555 Chunk 7/10 processed and model saved. ---> Acc score: 0.52 Chunk 8/10 processed and model saved. ---> Acc score: 0.455 Chunk 9/10 processed and model saved. ---> Acc score: 0.535 Chunk 10/10 processed and model saved.

You can follow the same online learning architecture while building the model incrementally and save the final model in ONNX format in the "Common Folder" for MetaTrader 5 usage.

Final Thoughts

Online learning is an excellent approach for keeping models continuously updated with minimal manual intervention. By implementing this infrastructure, you can be sure that your models stay aligned with the latest market trends and are adapting quickly to new information. However, it is important to note that online learning can sometimes make models highly sensitive to the order in which data is processed very often human oversight may be necessary to verify that the model and training information makes logical sense from a human perspective.You need to find the right balance between automating the learning process and periodic evaluation of your models to ensure everything goes as expected.

Attachments Table

Infrastructure (Folders) | Files | Description & Usage |

|---|---|---|

Python Client | - catboost_models.py - gru_models.py - main.py - incremental_learning.py | - A CatBoost model can be found in this file - A GRU model can be found in this file - The main python file for putting it all together - Incremental learning for CatBoost model is deployed in this file |

Common Folder | - catboost.H1.onnx - gru.H1.onnx - gru.H1.standard_scaler_mean.bin - gru.H1.standard_scaler_scale.bin | All the AI models in ONNX format and the scaler files in binary formats can be found in this folder |

| MetaTrader 5 (MQL5) | - Experts\Online Learning Catboost.mq5 - Experts\Online Learning GRU.mq5 - Include\CatBoost.mqh - Include\GRU.mqh - Include\preprocessing.mqh | - Deploys a CatBoost model in MQL5 - Deploys a GRU model in MQL5 - A library file for initializing and deploying a CatBoost model in ONNX format - A library file for initializing and deploying a GRU model in ONNX format - A library file which contains the StandardScaler for normalizing the data for ML model usage |

Warning: All rights to these materials are reserved by MetaQuotes Ltd. Copying or reprinting of these materials in whole or in part is prohibited.

This article was written by a user of the site and reflects their personal views. MetaQuotes Ltd is not responsible for the accuracy of the information presented, nor for any consequences resulting from the use of the solutions, strategies or recommendations described.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

Hi Omega J Msigwa

I asked what version of python are you using for this article I installed it and there is a library conflict.

The conflict is caused by:

The user requested protobuf==3.20.3

onnx 1.17.0 depends on protobuf>=3.20.2

onnxconverter-common 1.14.0 depends on protobuf==3.20.2

Then I edited the version as suggested and got another installation error.

To fix this you could try to:

1. loosen the range of package versions you've specified

2. remove package versions to allow pip to attempt to solve the dependency conflict

The conflict is caused by:

The user requested protobuf==3.20.2

onnx 1.17.0 depends on protobuf>=3.20.2

onnxconverter-common 1.14.0 depends on protobuf==3.20.2

tensorboard 2.18.0 depends on protobuf!=4.24.0 and >=3.19.6

tensorflow-intel 2.18.0 depends on protobuf!=4.21.0, !=4.21.1, !=4.21.2, !=4.21.3, !=4.21.4, !=4.21.5, <6.0.0dev and >=3.20.3

To fix this you could try to:

1. loosen the range of package versions you've specified

2. remove package versions to allow pip to attempt to solve the dependency conflict

Please give more instructions

Hi Omega J Msigwa

I asked what version of python are you using for this article I installed it and there is a library conflict.

The conflict is caused by:

The user requested protobuf==3.20.3

onnx 1.17.0 depends on protobuf>=3.20.2

onnxconverter-common 1.14.0 depends on protobuf==3.20.2

Then I edited the version as suggested and got another installation error.

To fix this you could try to:

1. loosen the range of package versions you've specified

2. remove package versions to allow pip to attempt to

solve the dependency conflict

The conflict is caused by:

The user requested protobuf==3.20.2

onnx 1.17.0 depends on protobuf>=3.20.2

onnxconverter-common 1.14.0 depends on protobuf==3.20.2

tensorboard 2.18.0 depends on protobuf!=4.24.0 and >=3.19.6

tensorflow-intel 2.18.0 depends on protobuf!=4.21.0, !=4.21.1, !=4.21.2, !=4.21.3, !=4.21.4, !=4.21.5, <6.0.0dev and >=3.20.3

To fix this you could try to:

1. loosen the range of package versions you've specified

2. remove package versions to allow pip to attempt to solve the dependency conflict

Please give more instructions

Hi Omega J Msigwa

I asked what version of python are you using for this article I installed it and there is a library conflict.

The conflict is caused by:

The user requested protobuf==3.20.3

onnx 1.17.0 depends on protobuf>=3.20.2

onnxconverter-common 1.14.0 depends on protobuf==3.20.2

Then I edited the version as suggested and got another installation error.

To fix this you could try to:

1. loosen the range of package versions you've specified

2. remove package versions to allow pip to attempt to solve the dependency conflict

The conflict is caused by:

The user requested protobuf==3.20.2

onnx 1.17.0 depends on protobuf>=3.20.2

onnxconverter-common 1.14.0 depends on protobuf==3.20.2

tensorboard 2.18.0 depends on protobuf!=4.24.0 and >=3.19.6

tensorflow-intel 2.18.0 depends on protobuf!=4.21.0, !=4.21.1, !=4.21.2, !=4.21.3, !=4.21.4, !=4.21.5, <6.0.0dev and >=3.20.3

To fix this you could try to:

1. loosen the range of package versions you've specified

2. remove package versions to allow pip to attempt to solve the dependency conflict

Please give more instructions

numpy==1.23.5