Monitoring trading with push notifications — example of a MetaTrader 5 service

Contents

- Introduction

- Project Structure

- Deal class

- Historical position class

- Class for searching and sorting by properties of deals and positions

- Class collection of historical positions

- Account class

- Class collection of accounts

- Service app for creating trading reports and sending notifications

- Conclusion

Introduction

When trading on financial markets, an important component is the availability of information about the results of trades conducted over a certain period of time in the past.

Probably, every trader at least once faced the need to monitor the trading results for the past day, week, month, etc., in order to adjust their strategy based on the trading results. MetaTrader 5 client terminal provides good statistics in the form of reports allowing us evaluate the trading results in a convenient visual form. The report can help optimize our portfolio, as well as understand how to reduce risks and increase trading stability.

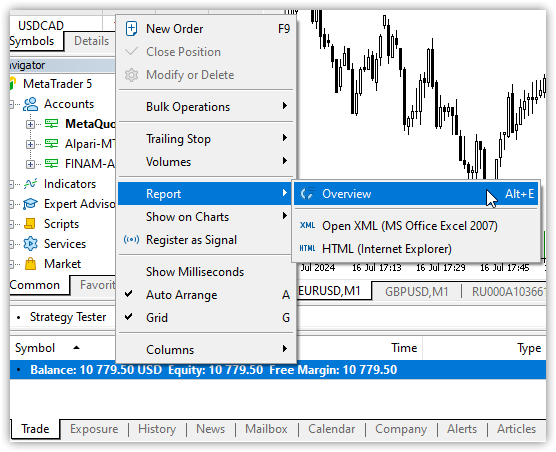

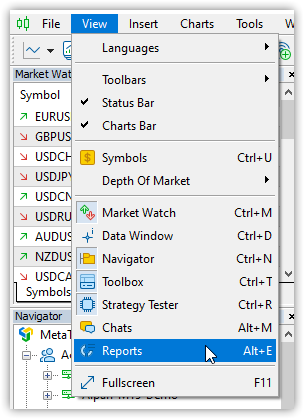

To analyze a strategy, click Report in the trading history context menu or Reports in the View menu (or simply press Alt+E):

|  |

Find more details in the article "New MetaTrader report: 5 most important trading metrics".

If for some reason the standard reports provided by the client terminal are not sufficient, the MQL5 language provides ample opportunities for creating your own programs, including the ones for generating reports and sending them to the trader’s smartphone. This is the possibility we will discuss today.

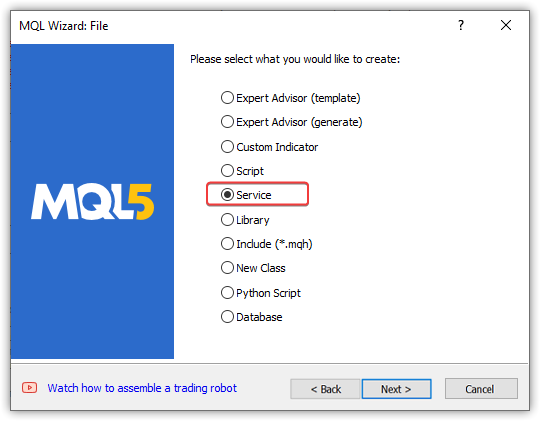

Our program should start at the moment of terminal launch, track the change of a trading account, daytime onset and the time for creating and sending reports. The Service program type will suit us for such purposes.

According to the MQL5 Reference, a Service is a program that, unlike indicators, EAs and scripts, does not require connection to a chart to operate. Like scripts, services do not handle any event except for trigger. To launch a service, its code should contain the OnStart handler function. Services do not accept any other events except Start, but they are able to send custom events to charts using EventChartCustom. Services are stored in <terminal_directory>\MQL5\Services.

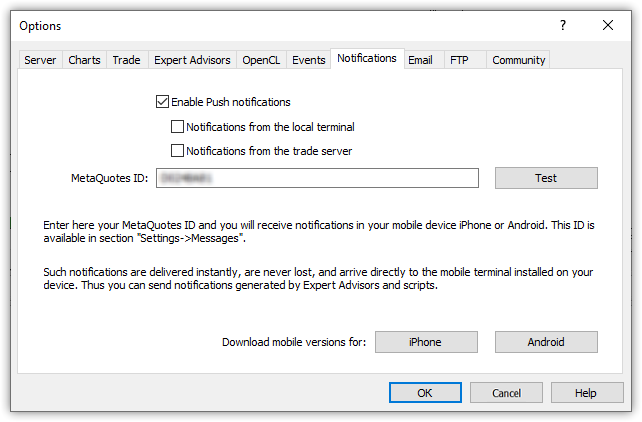

Every service running in the terminal works in its own flow. This means that a looped service cannot affect the operation of other programs. Our service should work in an infinite loop, check for the specified time, read the entire trading history, create lists of closed positions, sort these lists by different criteria and display reports on them to the journal and in Push notifications to the user's smartphone. In addition, when the service is first launched or its settings are changed, the service should check the possibility of sending Push notifications from the terminal. To achieve this, we should arrange an interaction with the user via message windows waiting for the user's response and reaction. In addition, when sending Push notifications, there are limitations on the frequency of notifications per unit of time. Therefore, it is necessary to set delays in sending notifications. All this should not in any way affect the operation of other applications running in the client terminal. Based on all of the above, Services are the most convenient tool for creating such a project.

Now it is necessary to form an idea of the components necessary to assemble everything together.

Project Structure

Let's look at the program and its components from end to beginning:

- Service app. The app has access to data from all accounts that have been active for the entire period of continuous operation of the service. From the accounts data, the app receives lists of closed positions and combines them into one general list. Depending on the settings, the service can use data on closed positions only from the current active account, or from the current and each of the previously used accounts in the client terminal.

Trading statistics is created for the required trading periods based on the data on closed positions obtained from the list of accounts. Then it is sent to the user's smartphone as push notifications. Additionally, trading statistics is displayed in tabular form in the Experts terminal logs. - Collection of accounts. The collection includes a list of accounts the terminal was connected to during the continuous operation of the service. The accounts collection gives access to any account in the list and to all closed positions of all accounts. The lists are available in the service app, and the service makes selections and creates statistics based on them.

- Account object class. Stores data for one account with a list (collection) of all closed positions, whose deals were carried out on this account during the continuous operation of the service. Provides access to account properties, to creating and updating the list of closed positions of this account and returns lists of closed positions by various selection criteria.

- Class collection of historical positions. Contains a list of position objects, provides access to the properties of closed positions, to creating and updating the list of positions. Returns the list of closed positions.

- Position object class. Stores and provides access to the properties of a closed position. Contains functionality for comparing two objects by various properties, which makes it possible to create lists of positions by various selection criteria. Contains a list of deals for this position and provides access to them.

- Deal object class. Stores and provides access to the properties of a single deal. The object contains functionality for comparing two objects by various properties, which makes it possible to create lists of deals by various selection criteria.

We discussed the concept of recovering a closed position from the list of historical deals in the article "How to view deals directly on the chart without weltering in trading history". The list of deals allows determining the affiliaton of each deal with a certain position by position ID (PositionID) set in the deal properties. A position object is created, in which the found deals are placed into the list. Here we will do the same way. But in order to arrange the construction of deal and position objects, we will use a completely different, long-tested concept, where each object has identical methods of access to properties for setting and obtaining them. This concept allows us to create objects in a single common key, store them in lists, filter and sort by any object property and get new lists in the context of the specified property.

Read the following articles to properly understand the concept of building classes in this project:

- structure of object properties "(Part I): Concept, data management and first results",

- structure of object lists "(Part II): Collection of historical orders and deals" and

- methods for filtering objects in lists by properties "(Part III): Collection of market orders and positions, search and sorting"

In essence, the three articles describe the possibility of creating a database for any objects in MQL5, storing them in the database and obtaining the required properties and values. This is precisely the functionality that is needed in this project, and it is for this reason that it was decided to build objects and their collections according to the concept described in the articles. Only here it will be done a little simpler - without creating abstract object classes with protected constructors and without defining unsupported object properties in the classes. Everything will be simpler - each object will have its own list of properties, stored in three arrays with the ability to write and retrieve them. All these objects will be stored in the lists, where it will be possible to obtain new lists of only the required objects according to the specified properties.

In short, each object created in the project will have a set of its own properties, as, indeed, any object or entity in MQL5. Only in MQL5 there are standard functions for obtaining properties, and for project objects these will be methods for obtaining integer, real and string properties, set directly in the class of each object. Further on, all these objects will be stored in the lists — dynamic arrays of pointers to the CObject objects of the Standard Library. The Standard Library classes allow us to create complex projects with minimal costs. In this case, this means a database of closed positions of all accounts where trading was conducted, with the ability to obtain lists of objects sorted and selected by any required property.

Any position exists only from the moment it is opened — performing In deal until the moment of closing — performing Out/OutBuy deal. In other words, it is an object that exists only as a market object. Any deal, on the contrary, is only a historical object, since a deal is simply the fact of execution of an order (trading order). Therefore, in the client terminal there are no positions in the historical list - they exist only in the list of current market positions.

Accordingly, in order to recreate an already closed market position, it is necessary to "assemble" a previously existing position from historical deals. Fortunately, each deal features ID of a position the deal participated in. We need to go through the list of historical deals, get the next deal from the list, check the position ID and create the position object. Add the created deal object to the new historical position. We will implement this further. In the meantime, let's create the classes for the deal and position object we will continue to work with.

Deal class

In the terminal directory \MQL5\Services\, create the new AccountReporter\ folder featuring the Deal.mqh new file of the CDeal class.

The class should be derived from the base class of the Standard Library CObject, while its file should be included into the newly created class:

//+------------------------------------------------------------------+ //| Deal.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include <Object.mqh> //+------------------------------------------------------------------+ //| Deal class | //+------------------------------------------------------------------+ class CDeal : public CObject { }

Now let's add the enumerations of integer, real and string deal properties, while in the private, protected and public sections, declare the class member variables and the methods for handling deal properties:

//+------------------------------------------------------------------+ //| Deal.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include <Object.mqh> //--- Enumeration of integer deal properties enum ENUM_DEAL_PROPERTY_INT { DEAL_PROP_TICKET = 0, // Deal ticket DEAL_PROP_ORDER, // Deal order number DEAL_PROP_TIME, // Deal execution time DEAL_PROP_TIME_MSC, // Deal execution time in milliseconds DEAL_PROP_TYPE, // Deal type DEAL_PROP_ENTRY, // Deal direction DEAL_PROP_MAGIC, // Deal magic number DEAL_PROP_REASON, // Deal execution reason or source DEAL_PROP_POSITION_ID, // Position ID DEAL_PROP_SPREAD, // Spread when performing a deal }; //--- Enumeration of real deal properties enum ENUM_DEAL_PROPERTY_DBL { DEAL_PROP_VOLUME = DEAL_PROP_SPREAD+1,// Deal volume DEAL_PROP_PRICE, // Deal price DEAL_PROP_COMMISSION, // Commission DEAL_PROP_SWAP, // Accumulated swap when closing DEAL_PROP_PROFIT, // Deal financial result DEAL_PROP_FEE, // Deal fee DEAL_PROP_SL, // Stop Loss level DEAL_PROP_TP, // Take Profit level }; //--- Enumeration of string deal properties enum ENUM_DEAL_PROPERTY_STR { DEAL_PROP_SYMBOL = DEAL_PROP_TP+1, // Symbol the deal is executed for DEAL_PROP_COMMENT, // Deal comment DEAL_PROP_EXTERNAL_ID, // Deal ID in an external trading system }; //+------------------------------------------------------------------+ //| Deal class | //+------------------------------------------------------------------+ class CDeal : public CObject { private: MqlTick m_tick; // Deal tick structure long m_lprop[DEAL_PROP_SPREAD+1]; // Array for storing integer properties double m_dprop[DEAL_PROP_TP-DEAL_PROP_SPREAD]; // Array for storing real properties string m_sprop[DEAL_PROP_EXTERNAL_ID-DEAL_PROP_TP]; // Array for storing string properties //--- Return the index of the array the deal's (1) double and (2) string properties are located at int IndexProp(ENUM_DEAL_PROPERTY_DBL property) const { return(int)property-DEAL_PROP_SPREAD-1; } int IndexProp(ENUM_DEAL_PROPERTY_STR property) const { return(int)property-DEAL_PROP_TP-1; } //--- Get a (1) deal tick and (2) a spread of the deal minute bar bool GetDealTick(const int amount=20); int GetSpreadM1(void); //--- Return time with milliseconds string TimeMscToString(const long time_msc,int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const; protected: //--- Additional properties int m_digits; // Symbol Digits double m_point; // Symbol Point double m_bid; // Bid when performing a deal double m_ask; // Ask when performing a deal public: //--- Set the properties //--- Set deal's (1) integer, (2) real and (3) string properties void SetProperty(ENUM_DEAL_PROPERTY_INT property,long value){ this.m_lprop[property]=value; } void SetProperty(ENUM_DEAL_PROPERTY_DBL property,double value){ this.m_dprop[this.IndexProp(property)]=value; } void SetProperty(ENUM_DEAL_PROPERTY_STR property,string value){ this.m_sprop[this.IndexProp(property)]=value; } //--- Integer properties void SetTicket(const long ticket) { this.SetProperty(DEAL_PROP_TICKET, ticket); } // Ticket void SetOrder(const long order) { this.SetProperty(DEAL_PROP_ORDER, order); } // Order void SetTime(const datetime time) { this.SetProperty(DEAL_PROP_TIME, time); } // Time void SetTimeMsc(const long value) { this.SetProperty(DEAL_PROP_TIME_MSC, value); } // Time in milliseconds void SetTypeDeal(const ENUM_DEAL_TYPE type) { this.SetProperty(DEAL_PROP_TYPE, type); } // Type void SetEntry(const ENUM_DEAL_ENTRY entry) { this.SetProperty(DEAL_PROP_ENTRY, entry); } // Direction void SetMagic(const long magic) { this.SetProperty(DEAL_PROP_MAGIC, magic); } // Magic number void SetReason(const ENUM_DEAL_REASON reason) { this.SetProperty(DEAL_PROP_REASON, reason); } // Deal execution reason or source void SetPositionID(const long id) { this.SetProperty(DEAL_PROP_POSITION_ID, id); } // Position ID //--- Real properties void SetVolume(const double volume) { this.SetProperty(DEAL_PROP_VOLUME, volume); } // Volume void SetPrice(const double price) { this.SetProperty(DEAL_PROP_PRICE, price); } // Price void SetCommission(const double value) { this.SetProperty(DEAL_PROP_COMMISSION, value); } // Commission void SetSwap(const double value) { this.SetProperty(DEAL_PROP_SWAP, value); } // Accumulated swap when closing void SetProfit(const double value) { this.SetProperty(DEAL_PROP_PROFIT, value); } // Financial result void SetFee(const double value) { this.SetProperty(DEAL_PROP_FEE, value); } // Deal fee void SetSL(const double value) { this.SetProperty(DEAL_PROP_SL, value); } // Stop Loss level void SetTP(const double value) { this.SetProperty(DEAL_PROP_TP, value); } // Take Profit level //--- String properties void SetSymbol(const string symbol) { this.SetProperty(DEAL_PROP_SYMBOL,symbol); } // Symbol name void SetComment(const string comment) { this.SetProperty(DEAL_PROP_COMMENT,comment); } // Comment void SetExternalID(const string ext_id) { this.SetProperty(DEAL_PROP_EXTERNAL_ID,ext_id); } // Deal ID in an external trading system //--- Get the properties //--- Return deal’s (1) integer, (2) real and (3) string property from the properties array long GetProperty(ENUM_DEAL_PROPERTY_INT property) const { return this.m_lprop[property]; } double GetProperty(ENUM_DEAL_PROPERTY_DBL property) const { return this.m_dprop[this.IndexProp(property)]; } string GetProperty(ENUM_DEAL_PROPERTY_STR property) const { return this.m_sprop[this.IndexProp(property)]; } //--- Integer properties long Ticket(void) const { return this.GetProperty(DEAL_PROP_TICKET); } // Ticket long Order(void) const { return this.GetProperty(DEAL_PROP_ORDER); } // Order datetime Time(void) const { return (datetime)this.GetProperty(DEAL_PROP_TIME); } // Time long TimeMsc(void) const { return this.GetProperty(DEAL_PROP_TIME_MSC); } // Time in milliseconds ENUM_DEAL_TYPE TypeDeal(void) const { return (ENUM_DEAL_TYPE)this.GetProperty(DEAL_PROP_TYPE); } // Type ENUM_DEAL_ENTRY Entry(void) const { return (ENUM_DEAL_ENTRY)this.GetProperty(DEAL_PROP_ENTRY); } // Direction long Magic(void) const { return this.GetProperty(DEAL_PROP_MAGIC); } // Magic number ENUM_DEAL_REASON Reason(void) const { return (ENUM_DEAL_REASON)this.GetProperty(DEAL_PROP_REASON); } // Deal execution reason or source long PositionID(void) const { return this.GetProperty(DEAL_PROP_POSITION_ID); } // Position ID //--- Real properties double Volume(void) const { return this.GetProperty(DEAL_PROP_VOLUME); } // Volume double Price(void) const { return this.GetProperty(DEAL_PROP_PRICE); } // Price double Commission(void) const { return this.GetProperty(DEAL_PROP_COMMISSION); } // Commission double Swap(void) const { return this.GetProperty(DEAL_PROP_SWAP); } // Accumulated swap when closing double Profit(void) const { return this.GetProperty(DEAL_PROP_PROFIT); } // Financial result double Fee(void) const { return this.GetProperty(DEAL_PROP_FEE); } // Deal fee double SL(void) const { return this.GetProperty(DEAL_PROP_SL); } // Stop Loss level double TP(void) const { return this.GetProperty(DEAL_PROP_TP); } // Take Profit level //--- String properties string Symbol(void) const { return this.GetProperty(DEAL_PROP_SYMBOL); } // Symbol name string Comment(void) const { return this.GetProperty(DEAL_PROP_COMMENT); } // Comment string ExternalID(void) const { return this.GetProperty(DEAL_PROP_EXTERNAL_ID); } // Deal ID in an external trading system //--- Additional properties double Bid(void) const { return this.m_bid; } // Bid when performing a deal double Ask(void) const { return this.m_ask; } // Ask when performing a deal int Spread(void) const { return (int)this.GetProperty(DEAL_PROP_SPREAD); } // Spread when performing a deal //--- Return the description of a (1) deal type, (2) position change method and (3) deal reason string TypeDescription(void) const; string EntryDescription(void) const; string ReasonDescription(void) const; //--- Return deal description string Description(void); //--- Print deal properties in the journal void Print(void); //--- Compare two objects by the property specified in 'mode' virtual int Compare(const CObject *node, const int mode=0) const; //--- Constructors/destructor CDeal(void){} CDeal(const ulong ticket); ~CDeal(); };

Let's have a look at the implementation of the class methods.

In the class constructor, consider that the deal has already been selected and we can get its properties:

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CDeal::CDeal(const ulong ticket) { //--- Store the properties //--- Integer properties this.SetTicket((long)ticket); // Deal ticket this.SetOrder(::HistoryDealGetInteger(ticket, DEAL_ORDER)); // Order this.SetTime((datetime)::HistoryDealGetInteger(ticket, DEAL_TIME)); // Deal execution time this.SetTimeMsc(::HistoryDealGetInteger(ticket, DEAL_TIME_MSC)); // Deal execution time in milliseconds this.SetTypeDeal((ENUM_DEAL_TYPE)::HistoryDealGetInteger(ticket, DEAL_TYPE)); // Type this.SetEntry((ENUM_DEAL_ENTRY)::HistoryDealGetInteger(ticket, DEAL_ENTRY)); // Direction this.SetMagic(::HistoryDealGetInteger(ticket, DEAL_MAGIC)); // Magic number this.SetReason((ENUM_DEAL_REASON)::HistoryDealGetInteger(ticket, DEAL_REASON)); // Deal execution reason or source this.SetPositionID(::HistoryDealGetInteger(ticket, DEAL_POSITION_ID)); // Position ID //--- Real properties this.SetVolume(::HistoryDealGetDouble(ticket, DEAL_VOLUME)); // Volume this.SetPrice(::HistoryDealGetDouble(ticket, DEAL_PRICE)); // Price this.SetCommission(::HistoryDealGetDouble(ticket, DEAL_COMMISSION)); // Commission this.SetSwap(::HistoryDealGetDouble(ticket, DEAL_SWAP)); // Accumulated swap when closing this.SetProfit(::HistoryDealGetDouble(ticket, DEAL_PROFIT)); // Financial result this.SetFee(::HistoryDealGetDouble(ticket, DEAL_FEE)); // Deal fee this.SetSL(::HistoryDealGetDouble(ticket, DEAL_SL)); // Stop Loss level this.SetTP(::HistoryDealGetDouble(ticket, DEAL_TP)); // Take Profit level //--- String properties this.SetSymbol(::HistoryDealGetString(ticket, DEAL_SYMBOL)); // Symbol name this.SetComment(::HistoryDealGetString(ticket, DEAL_COMMENT)); // Comment this.SetExternalID(::HistoryDealGetString(ticket, DEAL_EXTERNAL_ID)); // Deal ID in an external trading system //--- Additional parameters this.m_digits = (int)::SymbolInfoInteger(this.Symbol(), SYMBOL_DIGITS); this.m_point = ::SymbolInfoDouble(this.Symbol(), SYMBOL_POINT); //--- Parameters for calculating spread this.m_bid = 0; this.m_ask = 0; this.SetProperty(DEAL_PROP_SPREAD, 0); //--- If the historical tick and the Point value of the symbol were obtained if(this.GetDealTick() && this.m_point!=0) { //--- set the Bid and Ask price values, calculate and save the spread value this.m_bid=this.m_tick.bid; this.m_ask=this.m_tick.ask; int spread=(int)::fabs((this.m_ask-this.m_bid)/this.m_point); this.SetProperty(DEAL_PROP_SPREAD, spread); } //--- If failed to obtain a historical tick, take the spread value of the minute bar the deal took place on else this.SetProperty(DEAL_PROP_SPREAD, this.GetSpreadM1()); }

Save the deal properties, as well as Digits and Point of the symbol the deal was carried out for in the class properties arrays to perform calculations and display the deal information. Next, get the historical tick at the time of the deal. This way we provide access to the Bid and Ask prices at the time of the deal, and hence the ability to calculate the spread.

The method that compares two objects by a specified property:

//+------------------------------------------------------------------+ //| Compare two objects by the specified property | //+------------------------------------------------------------------+ int CDeal::Compare(const CObject *node,const int mode=0) const { const CDeal * obj = node; switch(mode) { case DEAL_PROP_TICKET : return(this.Ticket() > obj.Ticket() ? 1 : this.Ticket() < obj.Ticket() ? -1 : 0); case DEAL_PROP_ORDER : return(this.Order() > obj.Order() ? 1 : this.Order() < obj.Order() ? -1 : 0); case DEAL_PROP_TIME : return(this.Time() > obj.Time() ? 1 : this.Time() < obj.Time() ? -1 : 0); case DEAL_PROP_TIME_MSC : return(this.TimeMsc() > obj.TimeMsc() ? 1 : this.TimeMsc() < obj.TimeMsc() ? -1 : 0); case DEAL_PROP_TYPE : return(this.TypeDeal() > obj.TypeDeal() ? 1 : this.TypeDeal() < obj.TypeDeal() ? -1 : 0); case DEAL_PROP_ENTRY : return(this.Entry() > obj.Entry() ? 1 : this.Entry() < obj.Entry() ? -1 : 0); case DEAL_PROP_MAGIC : return(this.Magic() > obj.Magic() ? 1 : this.Magic() < obj.Magic() ? -1 : 0); case DEAL_PROP_REASON : return(this.Reason() > obj.Reason() ? 1 : this.Reason() < obj.Reason() ? -1 : 0); case DEAL_PROP_POSITION_ID : return(this.PositionID() > obj.PositionID() ? 1 : this.PositionID() < obj.PositionID() ? -1 : 0); case DEAL_PROP_SPREAD : return(this.Spread() > obj.Spread() ? 1 : this.Spread() < obj.Spread() ? -1 : 0); case DEAL_PROP_VOLUME : return(this.Volume() > obj.Volume() ? 1 : this.Volume() < obj.Volume() ? -1 : 0); case DEAL_PROP_PRICE : return(this.Price() > obj.Price() ? 1 : this.Price() < obj.Price() ? -1 : 0); case DEAL_PROP_COMMISSION : return(this.Commission() > obj.Commission() ? 1 : this.Commission() < obj.Commission() ? -1 : 0); case DEAL_PROP_SWAP : return(this.Swap() > obj.Swap() ? 1 : this.Swap() < obj.Swap() ? -1 : 0); case DEAL_PROP_PROFIT : return(this.Profit() > obj.Profit() ? 1 : this.Profit() < obj.Profit() ? -1 : 0); case DEAL_PROP_FEE : return(this.Fee() > obj.Fee() ? 1 : this.Fee() < obj.Fee() ? -1 : 0); case DEAL_PROP_SL : return(this.SL() > obj.SL() ? 1 : this.SL() < obj.SL() ? -1 : 0); case DEAL_PROP_TP : return(this.TP() > obj.TP() ? 1 : this.TP() < obj.TP() ? -1 : 0); case DEAL_PROP_SYMBOL : return(this.Symbol() > obj.Symbol() ? 1 : this.Symbol() < obj.Symbol() ? -1 : 0); case DEAL_PROP_COMMENT : return(this.Comment() > obj.Comment() ? 1 : this.Comment() < obj.Comment() ? -1 : 0); case DEAL_PROP_EXTERNAL_ID : return(this.ExternalID() > obj.ExternalID() ? 1 : this.ExternalID() < obj.ExternalID() ? -1 : 0); default : return(-1); } }

This is a virtual method that overrides the method of the same name in the CObject parent class. Depending on the comparison mode (one of the properties of the deal object), these properties are compared for the current object and for the one passed to the method by the pointer. The method returns 1 if the value of the current object property exceeds the one of the compared object. If less, we have -1. If the values are equal, we have 0.

The method that returns a deal type description:

//+------------------------------------------------------------------+ //| Return the deal type description | //+------------------------------------------------------------------+ string CDeal::TypeDescription(void) const { switch(this.TypeDeal()) { case DEAL_TYPE_BUY : return "Buy"; case DEAL_TYPE_SELL : return "Sell"; case DEAL_TYPE_BALANCE : return "Balance"; case DEAL_TYPE_CREDIT : return "Credit"; case DEAL_TYPE_CHARGE : return "Additional charge"; case DEAL_TYPE_CORRECTION : return "Correction"; case DEAL_TYPE_BONUS : return "Bonus"; case DEAL_TYPE_COMMISSION : return "Additional commission"; case DEAL_TYPE_COMMISSION_DAILY : return "Daily commission"; case DEAL_TYPE_COMMISSION_MONTHLY : return "Monthly commission"; case DEAL_TYPE_COMMISSION_AGENT_DAILY : return "Daily agent commission"; case DEAL_TYPE_COMMISSION_AGENT_MONTHLY: return "Monthly agent commission"; case DEAL_TYPE_INTEREST : return "Interest rate"; case DEAL_TYPE_BUY_CANCELED : return "Canceled buy deal"; case DEAL_TYPE_SELL_CANCELED : return "Canceled sell deal"; case DEAL_DIVIDEND : return "Dividend operations"; case DEAL_DIVIDEND_FRANKED : return "Franked (non-taxable) dividend operations"; case DEAL_TAX : return "Tax charges"; default : return "Unknown: "+(string)this.TypeDeal(); } }

Depending on the deal type, its text description is returned. For this project, this method is redundant, since we will not use all types of deals, but only those that relate to the position - buy or sell.

The method returning a description of the position change method:

//+------------------------------------------------------------------+ //| Return position change method | //+------------------------------------------------------------------+ string CDeal::EntryDescription(void) const { switch(this.Entry()) { case DEAL_ENTRY_IN : return "Entry In"; case DEAL_ENTRY_OUT : return "Entry Out"; case DEAL_ENTRY_INOUT : return "Reverse"; case DEAL_ENTRY_OUT_BY : return "Close a position by an opposite one"; default : return "Unknown: "+(string)this.Entry(); } }

The method returning a deal reason description:

//+------------------------------------------------------------------+ //| Return a deal reason description | //+------------------------------------------------------------------+ string CDeal::ReasonDescription(void) const { switch(this.Reason()) { case DEAL_REASON_CLIENT : return "Terminal"; case DEAL_REASON_MOBILE : return "Mobile"; case DEAL_REASON_WEB : return "Web"; case DEAL_REASON_EXPERT : return "EA"; case DEAL_REASON_SL : return "SL"; case DEAL_REASON_TP : return "TP"; case DEAL_REASON_SO : return "SO"; case DEAL_REASON_ROLLOVER : return "Rollover"; case DEAL_REASON_VMARGIN : return "Var. Margin"; case DEAL_REASON_SPLIT : return "Split"; case DEAL_REASON_CORPORATE_ACTION: return "Corp. Action"; default : return "Unknown reason "+(string)this.Reason(); } }

The method returning a deal description:

//+------------------------------------------------------------------+ //| Return deal description | //+------------------------------------------------------------------+ string CDeal::Description(void) { return(::StringFormat("Deal: %-9s %.2f %-4s #%I64d at %s", this.EntryDescription(), this.Volume(), this.TypeDescription(), this.Ticket(), this.TimeMscToString(this.TimeMsc()))); }

The method that prints deal properties in the journal:

//+------------------------------------------------------------------+ //| Print deal properties in the journal | //+------------------------------------------------------------------+ void CDeal::Print(void) { ::Print(this.Description()); }

The method returning time with milliseconds:

//+------------------------------------------------------------------+ //| Return time with milliseconds | //+------------------------------------------------------------------+ string CDeal::TimeMscToString(const long time_msc, int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const { return(::TimeToString(time_msc/1000, flags) + "." + ::IntegerToString(time_msc %1000, 3, '0')); }

All methods that return and log text descriptions are intended to describe the deal. In this project, they are not actually needed, but one should always remember about expansion and improvements. For this reason such methods are present here.

Method that receives the deal tick:

//+------------------------------------------------------------------+ //| Get the deal tick | //| https://www.mql5.com/ru/forum/42122/page47#comment_37205238 | //+------------------------------------------------------------------+ bool CDeal::GetDealTick(const int amount=20) { MqlTick ticks[]; // We will receive ticks here int attempts = amount; // Number of attempts to get ticks int offset = 500; // Initial time offset for an attempt int copied = 0; // Number of ticks copied //--- Until the tick is copied and the number of copy attempts is over //--- we try to get a tick, doubling the initial time offset at each iteration (expand the "from_msc" time range) while(!::IsStopped() && (copied<=0) && (attempts--)!=0) copied = ::CopyTicksRange(this.Symbol(), ticks, COPY_TICKS_INFO, this.TimeMsc()-(offset <<=1), this.TimeMsc()); //--- If the tick was successfully copied (it is the last one in the tick array), set it to the m_tick variable if(copied>0) this.m_tick=ticks[copied-1]; //--- Return the flag that the tick was copied return(copied>0); }

The method logic is described in the code comments. After receiving a tick, the Ask and Bid prices are taken from it and the spread size is calculated as (Ask - Bid) / Point.

If failed to obtain a tick using this method, obtain the average value of the spread using the method for obtaining the spread of the deal minute bar:

//+------------------------------------------------------------------+ //| Gets the spread of the deal minute bar | //+------------------------------------------------------------------+ int CDeal::GetSpreadM1(void) { int array[1]={}; int bar=::iBarShift(this.Symbol(), PERIOD_M1, this.Time()); if(bar==WRONG_VALUE) return 0; return(::CopySpread(this.Symbol(), PERIOD_M1, bar, 1, array)==1 ? array[0] : 0); }

The deal class is ready. The class objects will be stored in the list of deals in the historical position class, from which it will be possible to obtain pointers to the required deals and handle their data.

Historical position class

In \MQL5\Services\AccountReporter\, create the new file Position.mqh of the CPosition class.

The class should be inherited from the CObject Standard Library base object class:

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { }

Since the position class will contain a list for this position, it is necessary to include to the created file the deal class file and the class file of the dynamic array of pointers to CObject objects:

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include "Deal.mqh" #include <Arrays\ArrayObj.mqh> //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { }

Now let's add the enumerations of integer, real and string deal properties, while in the private, protected and public sections, declare the class member variables and the methods for handling position properties:

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include "Deal.mqh" #include <Arrays\ArrayObj.mqh> //--- Enumeration of integer position properties enum ENUM_POSITION_PROPERTY_INT { POSITION_PROP_TICKET = 0, // Position ticket POSITION_PROP_TIME, // Position open time POSITION_PROP_TIME_MSC, // Position open time in milliseconds POSITION_PROP_TIME_UPDATE, // Position change time POSITION_PROP_TIME_UPDATE_MSC, // Position change time in milliseconds POSITION_PROP_TYPE, // Position type POSITION_PROP_MAGIC, // Position magic number POSITION_PROP_IDENTIFIER, // Position ID POSITION_PROP_REASON, // Position open reason POSITION_PROP_ACCOUNT_LOGIN, // Account number POSITION_PROP_TIME_CLOSE, // Position close time POSITION_PROP_TIME_CLOSE_MSC, // Position close time in milliseconds }; //--- Enumeration of real position properties enum ENUM_POSITION_PROPERTY_DBL { POSITION_PROP_VOLUME = POSITION_PROP_TIME_CLOSE_MSC+1,// Position volume POSITION_PROP_PRICE_OPEN, // Position price POSITION_PROP_SL, // Stop Loss for open position POSITION_PROP_TP, // Take Profit for open position POSITION_PROP_PRICE_CURRENT, // Symbol current price POSITION_PROP_SWAP, // Accumulated swap POSITION_PROP_PROFIT, // Current profit POSITION_PROP_CONTRACT_SIZE, // Symbol trade contract size POSITION_PROP_PRICE_CLOSE, // Position close price POSITION_PROP_COMMISSIONS, // Accumulated commission POSITION_PROP_FEE, // Accumulated payment for deals }; //--- Enumeration of string position properties enum ENUM_POSITION_PROPERTY_STR { POSITION_PROP_SYMBOL = POSITION_PROP_FEE+1,// A symbol the position is open for POSITION_PROP_COMMENT, // Comment to a position POSITION_PROP_EXTERNAL_ID, // Position ID in the external system POSITION_PROP_CURRENCY_PROFIT, // Position symbol profit currency POSITION_PROP_ACCOUNT_CURRENCY, // Account deposit currency POSITION_PROP_ACCOUNT_SERVER, // Server name }; //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { private: long m_lprop[POSITION_PROP_TIME_CLOSE_MSC+1]; // Array for storing integer properties double m_dprop[POSITION_PROP_FEE-POSITION_PROP_TIME_CLOSE_MSC]; // Array for storing real properties string m_sprop[POSITION_PROP_ACCOUNT_SERVER-POSITION_PROP_FEE]; // Array for storing string properties //--- Return the index of the array the order's (1) double and (2) string properties are located at int IndexProp(ENUM_POSITION_PROPERTY_DBL property) const { return(int)property-POSITION_PROP_TIME_CLOSE_MSC-1;} int IndexProp(ENUM_POSITION_PROPERTY_STR property) const { return(int)property-POSITION_PROP_FEE-1; } protected: CArrayObj m_list_deals; // List of position deals CDeal m_temp_deal; // Temporary deal object for searching by property in the list //--- Return time with milliseconds string TimeMscToString(const long time_msc,int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const; //--- Additional properties int m_profit_pt; // Profit in points int m_digits; // Symbol digits double m_point; // One symbol point value double m_tick_value; // Calculated tick value //--- Return the pointer to (1) open and (2) close deal CDeal *GetDealIn(void) const; CDeal *GetDealOut(void) const; public: //--- Return the list of deals CArrayObj *GetListDeals(void) { return(&this.m_list_deals); } //--- Set the properties //--- Set (1) integer, (2) real and (3) string properties void SetProperty(ENUM_POSITION_PROPERTY_INT property,long value) { this.m_lprop[property]=value; } void SetProperty(ENUM_POSITION_PROPERTY_DBL property,double value) { this.m_dprop[this.IndexProp(property)]=value; } void SetProperty(ENUM_POSITION_PROPERTY_STR property,string value) { this.m_sprop[this.IndexProp(property)]=value; } //--- Integer properties void SetTicket(const long ticket) { this.SetProperty(POSITION_PROP_TICKET, ticket); } // Position ticket void SetTime(const datetime time) { this.SetProperty(POSITION_PROP_TIME, time); } // Position open time void SetTimeMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_MSC, value); } // Position open time in milliseconds since 01.01.1970 void SetTimeUpdate(const datetime time) { this.SetProperty(POSITION_PROP_TIME_UPDATE, time); } // Position update time void SetTimeUpdateMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_UPDATE_MSC, value); } // Position update time in milliseconds since 01.01.1970 void SetTypePosition(const ENUM_POSITION_TYPE type) { this.SetProperty(POSITION_PROP_TYPE, type); } // Position type void SetMagic(const long magic) { this.SetProperty(POSITION_PROP_MAGIC, magic); } // Magic number for a position (see ORDER_MAGIC) void SetID(const long id) { this.SetProperty(POSITION_PROP_IDENTIFIER, id); } // Position ID void SetReason(const ENUM_POSITION_REASON reason) { this.SetProperty(POSITION_PROP_REASON, reason); } // Position open reason void SetTimeClose(const datetime time) { this.SetProperty(POSITION_PROP_TIME_CLOSE, time); } // Close time void SetTimeCloseMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_CLOSE_MSC, value); } // Close time in milliseconds void SetAccountLogin(const long login) { this.SetProperty(POSITION_PROP_ACCOUNT_LOGIN, login); } // Acount number //--- Real properties void SetVolume(const double volume) { this.SetProperty(POSITION_PROP_VOLUME, volume); } // Position volume void SetPriceOpen(const double price) { this.SetProperty(POSITION_PROP_PRICE_OPEN, price); } // Position price void SetSL(const double value) { this.SetProperty(POSITION_PROP_SL, value); } // Stop Loss level for an open position void SetTP(const double value) { this.SetProperty(POSITION_PROP_TP, value); } // Take Profit level for an open position void SetPriceCurrent(const double price) { this.SetProperty(POSITION_PROP_PRICE_CURRENT, price); } // Current price by symbol void SetSwap(const double value) { this.SetProperty(POSITION_PROP_SWAP, value); } // Accumulated swap void SetProfit(const double value) { this.SetProperty(POSITION_PROP_PROFIT, value); } // Current profit void SetPriceClose(const double price) { this.SetProperty(POSITION_PROP_PRICE_CLOSE, price); } // Close price void SetContractSize(const double value) { this.SetProperty(POSITION_PROP_CONTRACT_SIZE, value); } // Symbol trading contract size void SetCommissions(void); // Total commission of all deals void SetFee(void); // Total deal fee //--- String properties void SetSymbol(const string symbol) { this.SetProperty(POSITION_PROP_SYMBOL, symbol); } // Symbol a position is opened for void SetComment(const string comment) { this.SetProperty(POSITION_PROP_COMMENT, comment); } // Position comment void SetExternalID(const string ext_id) { this.SetProperty(POSITION_PROP_EXTERNAL_ID, ext_id); } // Position ID in an external system (on the exchange) void SetAccountServer(const string server) { this.SetProperty(POSITION_PROP_ACCOUNT_SERVER, server); } // Server name void SetAccountCurrency(const string currency) { this.SetProperty(POSITION_PROP_ACCOUNT_CURRENCY, currency); } // Account deposit currency void SetCurrencyProfit(const string currency) { this.SetProperty(POSITION_PROP_CURRENCY_PROFIT, currency); } // Profit currency of the position symbol //--- Get the properties //--- Return (1) integer, (2) real and (3) string property from the properties array long GetProperty(ENUM_POSITION_PROPERTY_INT property) const { return this.m_lprop[property]; } double GetProperty(ENUM_POSITION_PROPERTY_DBL property) const { return this.m_dprop[this.IndexProp(property)]; } string GetProperty(ENUM_POSITION_PROPERTY_STR property) const { return this.m_sprop[this.IndexProp(property)]; } //--- Integer properties long Ticket(void) const { return this.GetProperty(POSITION_PROP_TICKET); } // Position ticket datetime Time(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME); } // Position open time long TimeMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_MSC); } // Position open time in milliseconds since 01.01.1970 datetime TimeUpdate(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME_UPDATE);} // Position change time long TimeUpdateMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_UPDATE_MSC); } // Position update time in milliseconds since 01.01.1970 ENUM_POSITION_TYPE TypePosition(void) const { return (ENUM_POSITION_TYPE)this.GetProperty(POSITION_PROP_TYPE);}// Position type long Magic(void) const { return this.GetProperty(POSITION_PROP_MAGIC); } // Magic number for a position (see ORDER_MAGIC) long ID(void) const { return this.GetProperty(POSITION_PROP_IDENTIFIER); } // Position ID ENUM_POSITION_REASON Reason(void) const { return (ENUM_POSITION_REASON)this.GetProperty(POSITION_PROP_REASON);}// Position opening reason datetime TimeClose(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME_CLOSE); } // Close time long TimeCloseMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_CLOSE_MSC); } // Close time in milliseconds long AccountLogin(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_LOGIN); } // Login //--- Real properties double Volume(void) const { return this.GetProperty(POSITION_PROP_VOLUME); } // Position volume double PriceOpen(void) const { return this.GetProperty(POSITION_PROP_PRICE_OPEN); } // Position price double SL(void) const { return this.GetProperty(POSITION_PROP_SL); } // Stop Loss level for an open position double TP(void) const { return this.GetProperty(POSITION_PROP_TP); } // Take Profit level for an open position double PriceCurrent(void) const { return this.GetProperty(POSITION_PROP_PRICE_CURRENT); } // Current price by symbol double Swap(void) const { return this.GetProperty(POSITION_PROP_SWAP); } // Accumulated swap double Profit(void) const { return this.GetProperty(POSITION_PROP_PROFIT); } // Current profit double ContractSize(void) const { return this.GetProperty(POSITION_PROP_CONTRACT_SIZE); } // Symbol trading contract size double PriceClose(void) const { return this.GetProperty(POSITION_PROP_PRICE_CLOSE); } // Close price double Commissions(void) const { return this.GetProperty(POSITION_PROP_COMMISSIONS); } // Total commission of all deals double Fee(void) const { return this.GetProperty(POSITION_PROP_FEE); } // Total deal fee //--- String properties string Symbol(void) const { return this.GetProperty(POSITION_PROP_SYMBOL); } // A symbol position is opened on string Comment(void) const { return this.GetProperty(POSITION_PROP_COMMENT); } // Position comment string ExternalID(void) const { return this.GetProperty(POSITION_PROP_EXTERNAL_ID); } // Position ID in an external system (on the exchange) string AccountServer(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_SERVER); } // Server name string AccountCurrency(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_CURRENCY); } // Account deposit currency string CurrencyProfit(void) const { return this.GetProperty(POSITION_PROP_CURRENCY_PROFIT); } // Profit currency of the position symbol //--- Additional properties ulong DealIn(void) const; // Open deal ticket ulong DealOut(void) const; // Close deal ticket int ProfitInPoints(void) const; // Profit in points int SpreadIn(void) const; // Spread when opening int SpreadOut(void) const; // Spread when closing double SpreadOutCost(void) const; // Spread cost when closing double PriceOutAsk(void) const; // Ask price when closing double PriceOutBid(void) const; // Bid price when closing //--- Add a deal to the list of deals, return the pointer CDeal *DealAdd(const long ticket); //--- Return a position type description string TypeDescription(void) const; //--- Return position open time and price description string TimePriceCloseDescription(void); //--- Return position close time and price description string TimePriceOpenDescription(void); //--- Return position description string Description(void); //--- Print the properties of the position and its deals in the journal void Print(void); //--- Compare two objects by the property specified in 'mode' virtual int Compare(const CObject *node, const int mode=0) const; //--- Constructor/destructor CPosition(const long position_id, const string symbol); CPosition(void){} ~CPosition(); };

Let's have a look at the implementation of the class methods.

Set the position ID and symbol from the parameters passed to the method in the class constructor, as well as write the account and symbol data:

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CPosition::CPosition(const long position_id, const string symbol) { this.m_list_deals.Sort(DEAL_PROP_TIME_MSC); this.SetID(position_id); this.SetSymbol(symbol); this.SetAccountLogin(::AccountInfoInteger(ACCOUNT_LOGIN)); this.SetAccountServer(::AccountInfoString(ACCOUNT_SERVER)); this.SetAccountCurrency(::AccountInfoString(ACCOUNT_CURRENCY)); this.SetCurrencyProfit(::SymbolInfoString(this.Symbol(),SYMBOL_CURRENCY_PROFIT)); this.SetContractSize(::SymbolInfoDouble(this.Symbol(),SYMBOL_TRADE_CONTRACT_SIZE)); this.m_digits = (int)::SymbolInfoInteger(this.Symbol(),SYMBOL_DIGITS); this.m_point = ::SymbolInfoDouble(this.Symbol(),SYMBOL_POINT); this.m_tick_value = ::SymbolInfoDouble(this.Symbol(), SYMBOL_TRADE_TICK_VALUE); }

In the class destructor, clear the list of position deals:

//+------------------------------------------------------------------+ //| Destructor | //+------------------------------------------------------------------+ CPosition::~CPosition() { this.m_list_deals.Clear(); }

The method that compares two objects by a specified property:

//+------------------------------------------------------------------+ //| Compare two objects by the specified property | //+------------------------------------------------------------------+ int CPosition::Compare(const CObject *node,const int mode=0) const { const CPosition *obj=node; switch(mode) { case POSITION_PROP_TICKET : return(this.Ticket() > obj.Ticket() ? 1 : this.Ticket() < obj.Ticket() ? -1 : 0); case POSITION_PROP_TIME : return(this.Time() > obj.Time() ? 1 : this.Time() < obj.Time() ? -1 : 0); case POSITION_PROP_TIME_MSC : return(this.TimeMsc() > obj.TimeMsc() ? 1 : this.TimeMsc() < obj.TimeMsc() ? -1 : 0); case POSITION_PROP_TIME_UPDATE : return(this.TimeUpdate() > obj.TimeUpdate() ? 1 : this.TimeUpdate() < obj.TimeUpdate() ? -1 : 0); case POSITION_PROP_TIME_UPDATE_MSC : return(this.TimeUpdateMsc() > obj.TimeUpdateMsc() ? 1 : this.TimeUpdateMsc() < obj.TimeUpdateMsc() ? -1 : 0); case POSITION_PROP_TYPE : return(this.TypePosition() > obj.TypePosition() ? 1 : this.TypePosition() < obj.TypePosition() ? -1 : 0); case POSITION_PROP_MAGIC : return(this.Magic() > obj.Magic() ? 1 : this.Magic() < obj.Magic() ? -1 : 0); case POSITION_PROP_IDENTIFIER : return(this.ID() > obj.ID() ? 1 : this.ID() < obj.ID() ? -1 : 0); case POSITION_PROP_REASON : return(this.Reason() > obj.Reason() ? 1 : this.Reason() < obj.Reason() ? -1 : 0); case POSITION_PROP_ACCOUNT_LOGIN : return(this.AccountLogin() > obj.AccountLogin() ? 1 : this.AccountLogin() < obj.AccountLogin() ? -1 : 0); case POSITION_PROP_TIME_CLOSE : return(this.TimeClose() > obj.TimeClose() ? 1 : this.TimeClose() < obj.TimeClose() ? -1 : 0); case POSITION_PROP_TIME_CLOSE_MSC : return(this.TimeCloseMsc() > obj.TimeCloseMsc() ? 1 : this.TimeCloseMsc() < obj.TimeCloseMsc() ? -1 : 0); case POSITION_PROP_VOLUME : return(this.Volume() > obj.Volume() ? 1 : this.Volume() < obj.Volume() ? -1 : 0); case POSITION_PROP_PRICE_OPEN : return(this.PriceOpen() > obj.PriceOpen() ? 1 : this.PriceOpen() < obj.PriceOpen() ? -1 : 0); case POSITION_PROP_SL : return(this.SL() > obj.SL() ? 1 : this.SL() < obj.SL() ? -1 : 0); case POSITION_PROP_TP : return(this.TP() > obj.TP() ? 1 : this.TP() < obj.TP() ? -1 : 0); case POSITION_PROP_PRICE_CURRENT : return(this.PriceCurrent() > obj.PriceCurrent() ? 1 : this.PriceCurrent() < obj.PriceCurrent() ? -1 : 0); case POSITION_PROP_SWAP : return(this.Swap() > obj.Swap() ? 1 : this.Swap() < obj.Swap() ? -1 : 0); case POSITION_PROP_PROFIT : return(this.Profit() > obj.Profit() ? 1 : this.Profit() < obj.Profit() ? -1 : 0); case POSITION_PROP_CONTRACT_SIZE : return(this.ContractSize() > obj.ContractSize() ? 1 : this.ContractSize() < obj.ContractSize() ? -1 : 0); case POSITION_PROP_PRICE_CLOSE : return(this.PriceClose() > obj.PriceClose() ? 1 : this.PriceClose() < obj.PriceClose() ? -1 : 0); case POSITION_PROP_COMMISSIONS : return(this.Commissions() > obj.Commissions() ? 1 : this.Commissions() < obj.Commissions() ? -1 : 0); case POSITION_PROP_FEE : return(this.Fee() > obj.Fee() ? 1 : this.Fee() < obj.Fee() ? -1 : 0); case POSITION_PROP_SYMBOL : return(this.Symbol() > obj.Symbol() ? 1 : this.Symbol() < obj.Symbol() ? -1 : 0); case POSITION_PROP_COMMENT : return(this.Comment() > obj.Comment() ? 1 : this.Comment() < obj.Comment() ? -1 : 0); case POSITION_PROP_EXTERNAL_ID : return(this.ExternalID() > obj.ExternalID() ? 1 : this.ExternalID() < obj.ExternalID() ? -1 : 0); case POSITION_PROP_CURRENCY_PROFIT : return(this.CurrencyProfit() > obj.CurrencyProfit() ? 1 : this.CurrencyProfit() < obj.CurrencyProfit() ? -1 : 0); case POSITION_PROP_ACCOUNT_CURRENCY : return(this.AccountCurrency() > obj.AccountCurrency() ? 1 : this.AccountCurrency() < obj.AccountCurrency() ? -1 : 0); case POSITION_PROP_ACCOUNT_SERVER : return(this.AccountServer() > obj.AccountServer() ? 1 : this.AccountServer() < obj.AccountServer() ? -1 : 0); default : return -1; } }

This is a virtual method that overrides the method of the same name in the CObject parent class. Depending on the comparison mode (one of the properties of the position object), these properties are compared for the current object and for the one passed to the method by the pointer. The method returns 1 if the value of the current object property exceeds the one of the compared object. If less, we have -1. If the values are equal, we have 0.

The method that returns time with milliseconds:

//+------------------------------------------------------------------+ //| Return time with milliseconds | //+------------------------------------------------------------------+ string CPosition::TimeMscToString(const long time_msc, int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const { return(::TimeToString(time_msc/1000, flags) + "." + ::IntegerToString(time_msc %1000, 3, '0')); }

The method returning the pointer to the open deal:

//+------------------------------------------------------------------+ //| Return the pointer to the opening deal | //+------------------------------------------------------------------+ CDeal *CPosition::GetDealIn(void) const { int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; if(deal.Entry()==DEAL_ENTRY_IN) return deal; } return NULL; }

In the loop via the list of position deals, look for a deal with the DEAL_ENTRY_IN (market entry) position change method and return the pointer to the found deal

The method returning the pointer to the close deal:

//+------------------------------------------------------------------+ //| Return the pointer to the close deal | //+------------------------------------------------------------------+ CDeal *CPosition::GetDealOut(void) const { for(int i=this.m_list_deals.Total()-1; i>=0; i--) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; if(deal.Entry()==DEAL_ENTRY_OUT || deal.Entry()==DEAL_ENTRY_OUT_BY) return deal; } return NULL; }

In the loop via the list of position deals, look for a deal with the DEAL_ENTRY_OUT (market exit) or DEAL_ENTRY_OUT_BY (close by) position change method and return the pointer to the found deal

The method returning the open deal ticket:

//+------------------------------------------------------------------+ //| Return the open deal ticket | //+------------------------------------------------------------------+ ulong CPosition::DealIn(void) const { CDeal *deal=this.GetDealIn(); return(deal!=NULL ? deal.Ticket() : 0); }

Get the pointer to the market entry deal and return its ticket.

The method returning the close deal ticket:

//+------------------------------------------------------------------+ //| Return the close deal ticket | //+------------------------------------------------------------------+ ulong CPosition::DealOut(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Ticket() : 0); }

Get the pointer to the market exit deal and return its ticket.

The method returning spread when opening:

//+------------------------------------------------------------------+ //| Return spread when opening | //+------------------------------------------------------------------+ int CPosition::SpreadIn(void) const { CDeal *deal=this.GetDealIn(); return(deal!=NULL ? deal.Spread() : 0); }

Get the pointer to the market entry deal and return the spread set in the deal.

The method returning spread when closing:

//+------------------------------------------------------------------+ //| Return spread when closing | //+------------------------------------------------------------------+ int CPosition::SpreadOut(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Spread() : 0); }

Get the pointer to the market exit deal and return the spread set in the deal.

The method returning the Ask price when closing:

//+------------------------------------------------------------------+ //| Return Ask price when closing | //+------------------------------------------------------------------+ double CPosition::PriceOutAsk(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Ask() : 0); }

Get the pointer to the market exit deal and return the Ask price value set in the deal.

The method returning Bid price when closing:

//+------------------------------------------------------------------+ //| Return the Bid price when closing | //+------------------------------------------------------------------+ double CPosition::PriceOutBid(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Bid() : 0); }

Get the pointer to the market exit deal and return the Bid price value set in the deal.

The method returning a profit in points:

//+------------------------------------------------------------------+ //| Return a profit in points | //+------------------------------------------------------------------+ int CPosition::ProfitInPoints(void) const { //--- If symbol Point has not been received previously, inform of that and return 0 if(this.m_point==0) { ::Print("The Point() value could not be retrieved."); return 0; } //--- Get position open and close prices double open =this.PriceOpen(); double close=this.PriceClose(); //--- If failed to get the prices, return 0 if(open==0 || close==0) return 0; //--- Depending on the position type, return the calculated value of the position profit in points return (int)::round(this.TypePosition()==POSITION_TYPE_BUY ? (close-open)/this.m_point : (open-close)/this.m_point); }

The method returning the spread when closing:

//+------------------------------------------------------------------+ //| Return the spread value when closing | //+------------------------------------------------------------------+ double CPosition::SpreadOutCost(void) const { //--- Get close deal CDeal *deal=this.GetDealOut(); if(deal==NULL) return 0; //--- Get position profit and position profit in points double profit=this.Profit(); int profit_pt=this.ProfitInPoints(); //--- If the profit is zero, return the spread value using the TickValue * Spread * Lots equation if(profit==0) return(this.m_tick_value * deal.Spread() * deal.Volume()); //--- Calculate and return the spread value (proportion) return(profit_pt>0 ? deal.Spread() * ::fabs(profit / profit_pt) : 0); }

The method uses two methods for calculating the spread value:

- if the position profit is not equal to zero, then the cost of the spread is calculated in the proportion: spread size in points * position profit in money / position profit in points.

- if the position profit is zero, then the spread value is calculated using the equation: calculated tick value * spread size in points * deal volume.

The method that sets the total commission for all deals:

//+------------------------------------------------------------------+ //| Set the total commission for all deals | //+------------------------------------------------------------------+ void CPosition::SetCommissions(void) { double res=0; int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); res+=(deal!=NULL ? deal.Commission() : 0); } this.SetProperty(POSITION_PROP_COMMISSIONS, res); }

To determine the commission taken for the entire position lifetime, we need to add up the commissions of all deals in the position. In the loop through the list of position deals, add the commission of each deal to the resulting value, which is eventually returned from the method.

The method setting the total deal fee:

//+------------------------------------------------------------------+ //| Sets the total deal fee | //+------------------------------------------------------------------+ void CPosition::SetFee(void) { double res=0; int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); res+=(deal!=NULL ? deal.Fee() : 0); } this.SetProperty(POSITION_PROP_FEE, res); }

Here everything is exactly the same as in the previous method - we return the total sum of the Fee values of each position deal.

Both of these methods must be called when all the position's trades have already been listed, otherwise the result will be incomplete.

The method that adds a deal to the list of position deals:

//+------------------------------------------------------------------+ //| Add a deal to the list of deals | //+------------------------------------------------------------------+ CDeal *CPosition::DealAdd(const long ticket) { //--- A temporary object gets a ticket of the desired deal and the flag of sorting the list of deals by ticket this.m_temp_deal.SetTicket(ticket); this.m_list_deals.Sort(DEAL_PROP_TICKET); //--- Set the result of checking if a deal with such a ticket is present in the list bool exist=(this.m_list_deals.Search(&this.m_temp_deal)!=WRONG_VALUE); //--- Return sorting by time in milliseconds for the list this.m_list_deals.Sort(DEAL_PROP_TIME_MSC); //--- If a deal with such a ticket is already in the list, return NULL if(exist) return NULL; //--- Create a new deal object CDeal *deal=new CDeal(ticket); if(deal==NULL) return NULL; //--- Add the created object to the list in sorting order by time in milliseconds //--- If failed to add the deal to the list, remove the the deal object and return NULL if(!this.m_list_deals.InsertSort(deal)) { delete deal; return NULL; } //--- If this is a position closing deal, set the profit from the deal properties to the position profit value if(deal.Entry()==DEAL_ENTRY_OUT || deal.Entry()==DEAL_ENTRY_OUT_BY) { this.SetProfit(deal.Profit()); this.SetSwap(deal.Swap()); } //--- Return the pointer to the created deal object return deal; }

The method logic is fully described in the code comments. The method receives the ticket of the currently selected deal. If there are no deals with such a ticket in the list yet, a new deal object is created and added to the list of position deals.

The methods that return descriptions of some position properties:

//+------------------------------------------------------------------+ //| Return a position type description | //+------------------------------------------------------------------+ string CPosition::TypeDescription(void) const { return(this.TypePosition()==POSITION_TYPE_BUY ? "Buy" : this.TypePosition()==POSITION_TYPE_SELL ? "Sell" : "Unknown::"+(string)this.TypePosition()); } //+------------------------------------------------------------------+ //| Return position open time and price description | //+------------------------------------------------------------------+ string CPosition::TimePriceOpenDescription(void) { return(::StringFormat("Opened %s [%.*f]", this.TimeMscToString(this.TimeMsc()),this.m_digits, this.PriceOpen())); } //+------------------------------------------------------------------+ //| Return position close time and price description | //+------------------------------------------------------------------+ string CPosition::TimePriceCloseDescription(void) { if(this.TimeCloseMsc()==0) return "Not closed yet"; return(::StringFormat("Closed %s [%.*f]", this.TimeMscToString(this.TimeCloseMsc()),this.m_digits, this.PriceClose())); } //+------------------------------------------------------------------+ //| Return a brief position description | //+------------------------------------------------------------------+ string CPosition::Description(void) { return(::StringFormat("%I64d (%s): %s %.2f %s #%I64d, Magic %I64d", this.AccountLogin(), this.AccountServer(), this.Symbol(), this.Volume(), this.TypeDescription(), this.ID(), this.Magic())); }

These methods are used, for example, to display a position description in the journal.

The Print method allows displaying the position description in the journal:

//+------------------------------------------------------------------+ //| Print the position properties and deals in the journal | //+------------------------------------------------------------------+ void CPosition::Print(void) { ::PrintFormat("%s\n-%s\n-%s", this.Description(), this.TimePriceOpenDescription(), this.TimePriceCloseDescription()); for(int i=0; i<this.m_list_deals.Total(); i++) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; deal.Print(); } }

First, a header with a position description is printed. Then a description of each deal is printed using its Print() method in a loop through all the position deals.

The historical position class is ready. Now let's create a static class for selecting, searching and sorting deals and positions by their properties.

Class for searching and sorting by properties of deals and positions

This class was thoroughly considered in the article "Library for easy and quick development of MetaTrader programs (Part III): Collection of market orders and positions, search and sorting" (Arranging the search section).

In \MQL5\Services\AccountReporter\, create the new file Select.mqh of the CSelect class:

//+------------------------------------------------------------------+ //| Select.mqh | //| Copyright 2024, MetaQuotes Software Corp. | //| https://mql5.com/en/users/artmedia70 | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Software Corp." #property link "https://mql5.com/en/users/artmedia70" #property version "1.00" //+------------------------------------------------------------------+ //| Class for sorting objects meeting the criterion | //+------------------------------------------------------------------+ class CSelect { }

Set the enumeration of comparison modes, include the files of deal and position classes and declare the storage list:

//+------------------------------------------------------------------+ //| Select.mqh | //| Copyright 2024, MetaQuotes Software Corp. | //| https://mql5.com/en/users/artmedia70 | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Software Corp." #property link "https://mql5.com/en/users/artmedia70" #property version "1.00" enum ENUM_COMPARER_TYPE { EQUAL, // Equal MORE, // More LESS, // Less NO_EQUAL, // Not equal EQUAL_OR_MORE, // Equal or more EQUAL_OR_LESS // Equal or less }; //+------------------------------------------------------------------+ //| Include files | //+------------------------------------------------------------------+ #include "Deal.mqh" #include "Position.mqh" //+------------------------------------------------------------------+ //| Storage list | //+------------------------------------------------------------------+ CArrayObj ListStorage; // Storage object for storing sorted collection lists //+------------------------------------------------------------------+ //| Class for sorting objects meeting the criterion | //+------------------------------------------------------------------+ class CSelect { }

Write all the methods for selecting objects and creating lists that satisfy the search criteria: