Biblioteca para el desarrollo rápido y sencillo de programas para MetaTrader (Parte XXV): Procesando los errores retornados por el servidor comercial

Contenido

Concepto

Bueno... Ya hemos implementado en nuestra clase comercial el control de

parámetros permitidos del terminal, la cuenta y el símbolo, así como la

corrección automática de los parámetros indicados de forma incorrecta para la orden comercial. Ahora, solo nos queda implementar el

procesamiento de las respuestas del servidor a una orden comercial preparada y enviada.

Después de enviar una orden comercial al

servidor, no deberíamos pensar que "ya está todo hecho", aún tenemos que comprobar qué respuesta hemos recibido a la solicitud comercial.

El servidor nos devuelve los códigos de error, o bien la ausencia de los mismos. Estos códigos deberemos obtenerlos y procesarlos en caso de

que el servidor retorne error.

Los procesaremos exactamente de la misma forma que hemos procesado los parámetros incorrectos de la

orden comercial:

- No hay error — la orden ha sido correctamente colocada en la cola de ejecución,

- Prohibir el comercio al experto — por ejemplo, prohibición completa por parte del servidor sobre las operaciones

comerciales,

- Salir del método comercial — por ejemplo, si no hay ninguna posibilidad de lograr enviar con éxito una orden al servidor,

o la posición ya ha sido cerrada o la orden pendiente ha sido eliminada,

- Corregir los parámetros de la solicitud comercial y repetir — hay algunos valores erróneos en los parámetros de la

orden comercial; seguramente, los datos han cambiado mientras se preparaba la solicitud al servidor, y ahora es necesario

corregirlos,

- Actualizar los datos y repetir — los datos en el servidor han cambiado, pero no es necesario corregir los valores de la

solicitud comercial,

- Esperar y repetir — debemos esperar un cierto tiempo, por ejemplo, si el precio se encuentra cerca de uno de los niveles

stop de la posición, el parámetro FreezeLevel prohibirá la modificación, dado que la orden stop ya puede activarse. La espera permite

aguardar ya sea la activación de la orden stop y la cancelación de la solicitud comercial, ya sea la salida por parte del precio de la zona

de congelación y el envío exitoso de la orden al servidor,

- Crear una solicitud pendiente — hablaremos de ello en el próximo artículo.

El asunto es que hay más códigos de retorno de los que hicimos anteriormente al corregir los posibles errores en la orden comercial, y no todos

los códigos pueden ser corregidos para repetir la solicitud. No obstante, para evitar errores subsanables, vamos a intentar procesarlos y

enviar de nuevo la orden comercial.

En los métodos de las solicitudes comerciales, después de la comprobación preliminar de las limitaciones y errores en la orden comercial,

organizamos un ciclo para el envío repetido de una orden comercial al servidor. Es decir, si después de la primera solicitud al servidor

hemos obtenido un error, enviaremos la orden comercial tantas veces como intentos comerciales se hayan establecido para la clase: o bien

hasta que la orden sea enviada con éxito al servidor, o bien hasta que se agoten los intentos.

Tras agotar sin éxito todos los intentos de

envío de la solicitud al servidor, retornamos false desde el método comercial,

puediendo en este caso ver en el programa que ha realizado la llamada el código del último error retornado por el servidor comercial, para así

tomar una decisión autónoma en cuanto al procesamiento de dicho error.

Vamos a dar la teoría por finalizada y pasar a la práctica.

Implementación

En la clase de cuenta CAccount, en el archivo Account.mqh, y dentro de este, en el apartado de acceso

simplificado a las propiedades del objeto de cuenta,

añadimos el método que

retorna la bandera de trabajo en la cuenta con el tipo de cobertura:

//+------------------------------------------------------------------+ //| Methods of a simplified access to the account object properties | //+------------------------------------------------------------------+ //--- Return the account's integer properties ENUM_ACCOUNT_TRADE_MODE TradeMode(void) const { return (ENUM_ACCOUNT_TRADE_MODE)this.GetProperty(ACCOUNT_PROP_TRADE_MODE); } ENUM_ACCOUNT_STOPOUT_MODE MarginSOMode(void) const { return (ENUM_ACCOUNT_STOPOUT_MODE)this.GetProperty(ACCOUNT_PROP_MARGIN_SO_MODE); } ENUM_ACCOUNT_MARGIN_MODE MarginMode(void) const { return (ENUM_ACCOUNT_MARGIN_MODE)this.GetProperty(ACCOUNT_PROP_MARGIN_MODE); } long Login(void) const { return this.GetProperty(ACCOUNT_PROP_LOGIN); } long Leverage(void) const { return this.GetProperty(ACCOUNT_PROP_LEVERAGE); } long LimitOrders(void) const { return this.GetProperty(ACCOUNT_PROP_LIMIT_ORDERS); } long TradeAllowed(void) const { return this.GetProperty(ACCOUNT_PROP_TRADE_ALLOWED); } long TradeExpert(void) const { return this.GetProperty(ACCOUNT_PROP_TRADE_EXPERT); } long CurrencyDigits(void) const { return this.GetProperty(ACCOUNT_PROP_CURRENCY_DIGITS); } long ServerType(void) const { return this.GetProperty(ACCOUNT_PROP_SERVER_TYPE); } long FIFOClose(void) const { return this.GetProperty(ACCOUNT_PROP_FIFO_CLOSE); } bool IsHedge(void) const { return this.MarginMode()==ACCOUNT_MARGIN_MODE_RETAIL_HEDGING; } //--- Return the account's real properties

Añadimos al archivo Defines.mqh una macrosustitución para

indicar el número de intentos comerciales por defecto para la clase comercial.

Dado que hoy vamos a preparar de forma adicional

la base para crear solicitudes pendientes, y necesitaremos un temporizador para la clase comercial,

añadimos

directamente los parámetros del temporizador de la clase comercial:

//+------------------------------------------------------------------+ //| Macro substitutions | //+------------------------------------------------------------------+ //--- Describe the function with the error line number #define DFUN_ERR_LINE (__FUNCTION__+(TerminalInfoString(TERMINAL_LANGUAGE)=="Russian" ? ", Page " : ", Line ")+(string)__LINE__+": ") #define DFUN (__FUNCTION__+": ") // "Function description" #define COUNTRY_LANG ("Russian") // Country language #define END_TIME (D'31.12.3000 23:59:59') // End date for account history data requests #define TIMER_FREQUENCY (16) // Minimal frequency of the library timer in milliseconds #define TOTAL_TRY (5) // Default number of trading attempts //--- Standard sounds #define SND_ALERT "alert.wav" #define SND_ALERT2 "alert2.wav" #define SND_CONNECT "connect.wav" #define SND_DISCONNECT "disconnect.wav" #define SND_EMAIL "email.wav" #define SND_EXPERT "expert.wav" #define SND_NEWS "news.wav" #define SND_OK "ok.wav" #define SND_REQUEST "request.wav" #define SND_STOPS "stops.wav" #define SND_TICK "tick.wav" #define SND_TIMEOUT "timeout.wav" #define SND_WAIT "wait.wav" //--- Parameters of the orders and deals collection timer #define COLLECTION_ORD_PAUSE (250) // Orders and deals collection timer pause in milliseconds #define COLLECTION_ORD_COUNTER_STEP (16) // Increment of the orders and deals collection timer counter #define COLLECTION_ORD_COUNTER_ID (1) // Orders and deals collection timer counter ID //--- Parameters of the account collection timer #define COLLECTION_ACC_PAUSE (1000) // Account collection timer pause in milliseconds #define COLLECTION_ACC_COUNTER_STEP (16) // Account timer counter increment #define COLLECTION_ACC_COUNTER_ID (2) // Account timer counter ID //--- Symbol collection timer 1 parameters #define COLLECTION_SYM_PAUSE1 (100) // Pause of the symbol collection timer 1 in milliseconds (for scanning market watch symbols) #define COLLECTION_SYM_COUNTER_STEP1 (16) // Increment of the symbol timer 1 counter #define COLLECTION_SYM_COUNTER_ID1 (3) // Symbol timer 1 counter ID //--- Symbol collection timer 2 parameters #define COLLECTION_SYM_PAUSE2 (300) // Pause of the symbol collection timer 2 in milliseconds (for events of the market watch symbol list) #define COLLECTION_SYM_COUNTER_STEP2 (16) // Increment of the symbol timer 2 counter #define COLLECTION_SYM_COUNTER_ID2 (4) // Symbol timer 2 counter ID //--- Trading class timer parameters #define COLLECTION_REQ_PAUSE (300) // Trading class timer pause in milliseconds #define COLLECTION_REQ_COUNTER_STEP (16) // Trading class timer counter increment #define COLLECTION_REQ_COUNTER_ID (5) // Trading class timer counter ID //--- Collection list IDs #define COLLECTION_HISTORY_ID (0x7779) // Historical collection list ID #define COLLECTION_MARKET_ID (0x777A) // Market collection list ID #define COLLECTION_EVENTS_ID (0x777B) // Event collection list ID #define COLLECTION_ACCOUNT_ID (0x777C) // Account collection list ID #define COLLECTION_SYMBOLS_ID (0x777D) // Symbol collection list ID //--- Data parameters for file operations #define DIRECTORY ("DoEasy\\") // Library directory for storing object folders #define RESOURCE_DIR ("DoEasy\\Resource\\") // Library directory for storing resource folders //--- Symbol parameters #define CLR_DEFAULT (0xFF000000) // Default color #define SYMBOLS_COMMON_TOTAL (1000) // Total number of working symbols //+------------------------------------------------------------------+

Añadimos dos banderas a la lista con las banderas de los métodos de procesamiento de los errores del servidor comercial: la

bandera de error en el precio de la orden pendiente y la bandera de error

en el precio de la orden stop, mientras que añadimos a los métodos de procesamiento de los errores y códigos de retorno del servidor

comercial el método para corregir los parámetros de la orden comercial:

//+------------------------------------------------------------------+ //| Flags indicating the trading request error handling methods | //+------------------------------------------------------------------+ enum ENUM_TRADE_REQUEST_ERR_FLAGS { TRADE_REQUEST_ERR_FLAG_NO_ERROR = 0, // No error TRADE_REQUEST_ERR_FLAG_FATAL_ERROR = 1, // Disable trading for an EA (critical error) - exit TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR = 2, // Library internal error - exit TRADE_REQUEST_ERR_FLAG_ERROR_IN_LIST = 4, // Error in the list - handle (ENUM_ERROR_CODE_PROCESSING_METHOD) TRADE_REQUEST_ERR_FLAG_PRICE_ERROR = 8, // Placement price error TRADE_REQUEST_ERR_FLAG_LIMIT_ERROR = 16, // Limit order price error }; //+------------------------------------------------------------------+ //| The methods of handling errors and server return codes | //+------------------------------------------------------------------+ enum ENUM_ERROR_CODE_PROCESSING_METHOD { ERROR_CODE_PROCESSING_METHOD_OK, // No errors ERROR_CODE_PROCESSING_METHOD_DISABLE, // Disable trading for the EA ERROR_CODE_PROCESSING_METHOD_EXIT, // Exit the trading method ERROR_CODE_PROCESSING_METHOD_CORRECT, // Correct trading request parameters and repeat ERROR_CODE_PROCESSING_METHOD_REFRESH, // Update data and repeat ERROR_CODE_PROCESSING_METHOD_PENDING, // Create a pending request ERROR_CODE_PROCESSING_METHOD_WAIT, // Wait and repeat }; //+------------------------------------------------------------------+

Añadimos en el archivo Datas.mqh los índices de los nuevos mensajes:

//--- CTrading MSG_LIB_TEXT_TERMINAL_NOT_TRADE_ENABLED, // Trade operations are not allowed in the terminal (the AutoTrading button is disabled) MSG_LIB_TEXT_EA_NOT_TRADE_ENABLED, // EA is not allowed to trade (F7 --> Common --> Allow Automated Trading) MSG_LIB_TEXT_ACCOUNT_NOT_TRADE_ENABLED, // Trading is disabled for the current account MSG_LIB_TEXT_ACCOUNT_EA_NOT_TRADE_ENABLED, // Trading on the trading server side is disabled for EAs on the current account MSG_LIB_TEXT_REQUEST_REJECTED_DUE, // Request was rejected before sending to the server due to: MSG_LIB_TEXT_INVALID_REQUEST, // Invalid request: MSG_LIB_TEXT_NOT_ENOUTH_MONEY_FOR, // Insufficient funds for performing a trade MSG_LIB_TEXT_MAX_VOLUME_LIMIT_EXCEEDED, // Exceeded maximum allowed aggregate volume of orders and positions in one direction MSG_LIB_TEXT_REQ_VOL_LESS_MIN_VOLUME, // Request volume is less than the minimum acceptable one MSG_LIB_TEXT_REQ_VOL_MORE_MAX_VOLUME, // Request volume exceeds the maximum acceptable one MSG_LIB_TEXT_CLOSE_BY_ORDERS_DISABLED, // Close by is disabled MSG_LIB_TEXT_INVALID_VOLUME_STEP, // Request volume is not a multiple of the minimum lot change step gradation MSG_LIB_TEXT_CLOSE_BY_SYMBOLS_UNEQUAL, // Symbols of opposite positions are not equal MSG_LIB_TEXT_SL_LESS_STOP_LEVEL, // StopLoss violates requirements for symbol's StopLevel MSG_LIB_TEXT_TP_LESS_STOP_LEVEL, // TakeProfit violates requirements for symbol's StopLevel MSG_LIB_TEXT_PRICE_LESS_STOP_LEVEL, // Order distance in points is less than a value allowed by symbol's StopLevel parameter MSG_LIB_TEXT_LIMIT_LESS_STOP_LEVEL, // Limit order distance in points relative to a stop order is less than a value allowed by symbol's StopLevel parameter MSG_LIB_TEXT_SL_LESS_FREEZE_LEVEL, // The distance from the price to StopLoss is less than a value allowed by symbol's FreezeLevel parameter MSG_LIB_TEXT_TP_LESS_FREEZE_LEVEL, // The distance from the price to TakeProfit is less than a value allowed by symbol's FreezeLevel parameter MSG_LIB_TEXT_PR_LESS_FREEZE_LEVEL, // The distance from the price to an order activation level is less than a value allowed by symbol's FreezeLevel parameter MSG_LIB_TEXT_UNSUPPORTED_SL_TYPE, // Unsupported StopLoss parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_TP_TYPE, // Unsupported TakeProfit parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_PR_TYPE, // Unsupported price parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_PL_TYPE, // Unsupported limit order price parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_PRICE_TYPE_IN_REQ, // Unsupported price parameter type in a request MSG_LIB_TEXT_TRADING_DISABLE, // Trading disabled for the EA until the reason is eliminated MSG_LIB_TEXT_TRADING_OPERATION_ABORTED, // Trading operation is interrupted MSG_LIB_TEXT_CORRECTED_TRADE_REQUEST, // Correcting trading request parameters MSG_LIB_TEXT_CREATE_PENDING_REQUEST, // Creating a pending request MSG_LIB_TEXT_NOT_POSSIBILITY_CORRECT_LOT, // Unable to correct a lot MSG_LIB_TEXT_FAILING_CREATE_PENDING_REQ, // Failed to create a pending request MSG_LIB_TEXT_TRY_N, // Trading attempt # };

y los textos de estos mensajes:

{"Дистанция установки ордера в пунктах меньше разрешённой параметром StopLevel символа","The distance to place an order in points is less than the symbol allowed by the StopLevel parameter"},

{"Дистанция установки лимит-ордера относительно стоп-ордера меньше разрешённой параметром StopLevel символа","The distance to place the limit order relative to the stop order is less than the symbol allowed by the StopLevel parameter"},

{"Дистанция от цены до StopLoss меньше разрешённой параметром FreezeLevel символа","The distance from the price to StopLoss is less than the symbol allowed by the FreezeLevel parameter"},

{"Дистанция от цены до TakeProfit меньше разрешённой параметром FreezeLevel символа","The distance from the price to TakeProfit is less than the symbol allowed by the FreezeLevel parameter"},

{"Дистанция от цены до цены срабатывания ордера меньше разрешённой параметром FreezeLevel символа","The distance from the price to the order triggering price is less than the symbol allowed by the FreezeLevel parameter"},

{"Неподдерживаемый тип параметра StopLoss (необходимо int или double)","Unsupported StopLoss parameter type (int or double required)"},

{"Неподдерживаемый тип параметра TakeProfit (необходимо int или double)","Unsupported TakeProfit parameter type (int or double required)"},

{"Неподдерживаемый тип параметра цены (необходимо int или double)","Unsupported price parameter type (int or double required)"},

{"Неподдерживаемый тип параметра цены limit-ордера (необходимо int или double)","Unsupported type of price parameter for limit order (int or double required)"},

{"Неподдерживаемый тип параметра цены в запросе","Unsupported price parameter type in request"},

{"Торговля отключена для эксперта до устранения причины запрета","Trading for the expert is disabled until this ban is eliminated"},

{"Торговая операция прервана","Trading operation aborted"},

{"Корректировка параметров торгового запроса ...","Correction of trade request parameters ..."},

{"Создание отложенного запроса","Create a pending request"},

{"Нет возможности скорректировать лот","There is no possibility to correct the lot"},

{"Не удалось создать отложенный запрос","Failed to create pending request"},

{"Торговая попытка #","Trading attempt #"},

};

Asimismo, hemos introducido algunos cambios en el archivo del objeto básico TradeObj.mqh.

Hemos añadido al

método de colocación de órdenes pendientes el parámetro del tipo de orden según su

ejecución

(por algún motivo, olvidamos implementarlo en su momento, así que se usaba el método por defecto):

//--- Place an order bool SetOrder(const ENUM_ORDER_TYPE type, const double volume, const double price, const double sl=0, const double tp=0, const double price_stoplimit=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE);

Ahora, si se ha transmitido un valor superior a -1, se usará el valor transmitido al método, de lo contrario, se utilizará el valor establecido por defecto:

//+------------------------------------------------------------------+ //| Set an order | //+------------------------------------------------------------------+ bool CTradeObj::SetOrder(const ENUM_ORDER_TYPE type, const double volume, const double price, const double sl=0, const double tp=0, const double price_stoplimit=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { ::ResetLastError(); //--- If an invalid order type has been passed, write the error code and description, send the message to the journal and return 'false' if(type==ORDER_TYPE_BUY || type==ORDER_TYPE_SELL || type==ORDER_TYPE_CLOSE_BY #ifdef __MQL4__ || type==ORDER_TYPE_BUY_STOP_LIMIT || type==ORDER_TYPE_SELL_STOP_LIMIT #endif ) { this.m_result.retcode=MSG_LIB_SYS_INVALID_ORDER_TYPE; this.m_result.comment=CMessage::Text(this.m_result.retcode); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_INVALID_ORDER_TYPE),OrderTypeDescription(type)); return false; } //--- Clear the structures ::ZeroMemory(this.m_request); ::ZeroMemory(this.m_result); //--- Fill in the request structure this.m_request.action = TRADE_ACTION_PENDING; this.m_request.symbol = this.m_symbol; this.m_request.magic = (magic==ULONG_MAX ? this.m_magic : magic); this.m_request.volume = volume; this.m_request.type = type; this.m_request.stoplimit = price_stoplimit; this.m_request.price = price; this.m_request.sl = sl; this.m_request.tp = tp; this.m_request.expiration = expiration; this.m_request.type_time = (type_time>WRONG_VALUE ? type_time : this.m_type_time); this.m_request.type_filling= (type_filling>WRONG_VALUE ? type_filling : this.m_type_filling); this.m_request.comment = (comment==NULL ? this.m_comment : comment); //--- Return the result of sending a request to the server #ifdef __MQL5__ return(!this.m_async_mode ? ::OrderSend(this.m_request,this.m_result) : ::OrderSendAsync(this.m_request,this.m_result)); #else ::ResetLastError(); int ticket=::OrderSend(m_request.symbol,m_request.type,m_request.volume,m_request.price,(int)m_request.deviation,m_request.sl,m_request.tp,m_request.comment,(int)m_request.magic,m_request.expiration,clrNONE); ::SymbolInfoTick(this.m_symbol,this.m_tick); if(ticket!=WRONG_VALUE) { this.m_result.retcode=::GetLastError(); this.m_result.ask=this.m_tick.ask; this.m_result.bid=this.m_tick.bid; this.m_result.order=ticket; this.m_result.price=(::OrderSelect(ticket,SELECT_BY_TICKET) ? ::OrderOpenPrice() : this.m_request.price); this.m_result.volume=(::OrderSelect(ticket,SELECT_BY_TICKET) ? ::OrderLots() : this.m_request.volume); this.m_result.comment=CMessage::Text(this.m_result.retcode); return true; } else { this.m_result.retcode=::GetLastError(); this.m_result.ask=this.m_tick.ask; this.m_result.bid=this.m_tick.bid; this.m_result.comment=CMessage::Text(this.m_result.retcode); return false; } #endif } //+------------------------------------------------------------------+

Asimismo, hemos corregido los precios en las órdenes comerciales: antes, si un gráfico se construía según los precios Last, el precio en la orden

comercial también se establecía como Ask y Last. Ahora, siempre serán Ask y Bid, independientemente de los precios de construcción del

gráfico.

Las demás correcciones se podrán ver en los archivos adjuntos al final del artículo, ya que son poco significativas y no merece la pena

dedicarles atención aparte.

En el archivo Trading.mqh de la clase comercial CTrading, añadimos a su sección privada la

lista de solicitudes pendientes y la variable para guardar el número de

intentos comerciales:

//+------------------------------------------------------------------+ //| Trading class | //+------------------------------------------------------------------+ class CTrading { private: CAccount *m_account; // Pointer to the current account object CSymbolsCollection *m_symbols; // Pointer to the symbol collection list CMarketCollection *m_market; // Pointer to the list of the collection of market orders and positions CHistoryCollection *m_history; // Pointer to the list of the collection of historical orders and deals CArrayObj m_list_request; // List of pending requests CArrayInt m_list_errors; // Error list bool m_is_trade_disable; // Flag disabling trading bool m_use_sound; // The flag of using sounds of the object trading events uchar m_total_try; // Number of trading attempts ENUM_LOG_LEVEL m_log_level; // Logging level MqlTradeRequest m_request; // Trading request prices ENUM_TRADE_REQUEST_ERR_FLAGS m_error_reason_flags; // Flags of error source in a trading method ENUM_ERROR_HANDLING_BEHAVIOR m_err_handling_behavior; // Behavior when handling error

En la lista de solicitudes comerciales, guardaremos en lo sucesivo los objetos de la clase de la solicitud pendiente, mientras que a la variable m_total_try añadiremos el número de intentos comerciales establecido por defecto para la clase comercial en su constructor:

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CTrading::CTrading() { this.m_list_errors.Clear(); this.m_list_errors.Sort(); this.m_list_request.Clear(); this.m_list_request.Sort(); this.m_total_try=TOTAL_TRY; this.m_log_level=LOG_LEVEL_ALL_MSG; this.m_is_trade_disable=false; this.m_err_handling_behavior=ERROR_HANDLING_BEHAVIOR_CORRECT; ::ZeroMemory(this.m_request); } //+------------------------------------------------------------------+

Aquí mismo, limpiamos la lista de solicitudes pendientes y le asignamos la bandera de

lista clasificada.

Asimismo, añadimos a los parámetros del método de comprobación del precio respecto al nivel StopLevel el

precio de colocación de órdenes límite con el tipo StopLimit:

bool CheckPriceByStopLevel(const ENUM_ORDER_TYPE order_type,const double price,const CSymbol *symbol_obj,const double limit=0);

Y añadimos la comprobación al propio método:

//+------------------------------------------------------------------+ //| Return the flag checking the validity of the distance | //| from the price to the placement level by StopLevel | //+------------------------------------------------------------------+ bool CTrading::CheckPriceByStopLevel(const ENUM_ORDER_TYPE order_type,const double price,const CSymbol *symbol_obj,const double limit=0) { double lv=symbol_obj.TradeStopLevel()*symbol_obj.Point(); double pr=(this.DirectionByActionType((ENUM_ACTION_TYPE)order_type)==ORDER_TYPE_BUY ? symbol_obj.Ask() : symbol_obj.Bid()); return (limit==0 ? //--- Order placement prices relative to the price ( order_type==ORDER_TYPE_SELL_STOP || order_type==ORDER_TYPE_SELL_STOP_LIMIT || order_type==ORDER_TYPE_BUY_LIMIT ? price<(pr-lv) : order_type==ORDER_TYPE_BUY_STOP || order_type==ORDER_TYPE_BUY_STOP_LIMIT || order_type==ORDER_TYPE_SELL_LIMIT ? price>(pr+lv) : true ) : //--- Limit order placement prices relative to the stop order price ( order_type==ORDER_TYPE_BUY_STOP_LIMIT ? limit<(price-lv) : order_type==ORDER_TYPE_SELL_STOP_LIMIT ? limit>(price+lv) : true ) ); } //+------------------------------------------------------------------+

Aquí: si el precio de la orden límite es igual a cero, comprobamos los precio de las órdenes stop y límite, de lo contrario, comprobamos los precios de las órdenes stoplimit (el precio de colocación de una orden límite respecto al precio de colocación de la orden stop conforme a la cual se activa la orden stoplimit).

Vamos a transmitir el código de error al método que retorna el método de procesamiento de errores; asimismo añadimos al método de corrección de errores un puntero adicional al objeto comercial:

//--- Return the error handling method ENUM_ERROR_CODE_PROCESSING_METHOD ResultProccessingMethod(const uint result_code); //--- Correct errors ENUM_ERROR_CODE_PROCESSING_METHOD RequestErrorsCorrecting(MqlTradeRequest &request,const ENUM_ORDER_TYPE order_type,const uint spread_multiplier,CSymbol *symbol_obj,CTradeObj *trade_obj);

Ya que disponemos de multitud de métodos de apertura de posiciones y colocación de órdenes, todos ellos han resultado prácticamente

idénticos. La única diferencia reside en los tipos de las posiciones abiertas y las órdenes colocadas.

Para no escribir el mismo código

para cada método,

vamos a declarar e implementar posteriormente dos métodos privados, uno

para abrir posiciones y otro para colocar órdenes pendientes:

//--- (1) Open a position, (2) place a pending order template<typename SL,typename TP> bool OpenPosition(const ENUM_POSITION_TYPE type, const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX); template<typename PS,typename PL,typename SL,typename TP> bool PlaceOrder( const ENUM_ORDER_TYPE order_type, const double volume, const string symbol, const PS price_stop, const PL price_limit=0, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); public: //--- Constructor

En la sección pública de la clase, declaramos el temporizador

que necesitaremos para trabajar con la clase de solicitudes pendientes, el

método que retorna la lista de solicitudes pendientes y el método que

establece el número de intentos comerciales:

public: //--- Constructor CTrading(); //--- Timer void OnTimer(void); //--- Get the pointers to the lists (make sure to call the method in program's OnInit() since the symbol collection list is created there) void OnInit(CAccount *account,CSymbolsCollection *symbols,CMarketCollection *market,CHistoryCollection *history) { this.m_account=account; this.m_symbols=symbols; this.m_market=market; this.m_history=history; } //--- Return the list of (1) errors and (2) pending requests CArrayInt *GetListErrors(void) { return &this.m_list_errors; } CArrayObj *GetListRequests(void) { return &this.m_list_request;} //--- Set the number of trading attempts void SetTotalTry(const uchar number) { this.m_total_try=number; } //--- Check limitations and errors

Completamos la especifición del método para cerrar las posiciones con un volumen cerrado, por defecto WRONG_VALUE, el cierre completo de la posición, de lo contrario, tendremos el cierre parcial con el volumen indicado:

bool ClosePosition(const ulong ticket,const double volume=WRONG_VALUE,const string comment=NULL,const ulong deviation=ULONG_MAX);

En las especificaciones de los métodos para colocar órdenes pendientes, añadimos

los tipos de ejecución

de órdenes según el resto: antes, siempre se usaba el valor establecido por defecto para la clase. Ahora, se seleccionará el

valor del tipo de ejeucución de orden a partir del valor transmitido al método: si tenemos WRONG_VALUE,

se seleccionará el valor por defecto, de lo contrario, se seleccionará el valor transmitido al método:

//--- Set (1) BuyStop, (2) BuyLimit, (3) BuyStopLimit pending order template<typename PS,typename SL,typename TP> bool PlaceBuyStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename SL,typename TP> bool PlaceBuyLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename PL,typename SL,typename TP> bool PlaceBuyStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); //--- Set (1) SellStop, (2) SellLimit, (3) SellStopLimit pending order template<typename PS,typename SL,typename TP> bool PlaceSellStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename SL,typename TP> bool PlaceSellLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename PL,typename SL,typename TP> bool PlaceSellStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); //--- Modify a pending order template<typename PS,typename PL,typename SL,typename TP> bool ModifyOrder(const ulong ticket, const PS price=WRONG_VALUE, const SL sl=WRONG_VALUE, const TP tp=WRONG_VALUE, const PL limit=WRONG_VALUE, datetime expiration=WRONG_VALUE, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE);

Vamos a escribir la implementación del método. Por ahora, solo implementaremos el procesamiento de la lista de solicitudes pendientes:

//+------------------------------------------------------------------+ //| Temporizador | //+------------------------------------------------------------------+ void CTrading::OnTimer(void) { int total=this.m_list_request.Total(); for(int i=total-1;i>WRONG_VALUE;i--) { } } //+------------------------------------------------------------------+

Implementamos el método que retorna los métodos de procesamiento de los códigos de retorno del servidor comercial:

//+------------------------------------------------------------------+ //| Return the error handling method | //+------------------------------------------------------------------+ ENUM_ERROR_CODE_PROCESSING_METHOD CTrading::ResultProccessingMethod(const uint result_code) { switch(result_code) { #ifdef __MQL4__ //--- Malfunctional trade operation case 9 : //--- Account disabled case 64 : //--- Invalid account number case 65 : return ERROR_CODE_PROCESSING_METHOD_DISABLE; //--- No error but result is unknown case 1 : //--- General error case 2 : //--- Old client terminal version case 5 : //--- Not enough rights case 7 : //--- Market closed case 132 : //--- Trading disabled case 133 : //--- Order is locked and being processed case 139 : //--- Buy only case 140 : //--- The number of open and pending orders has reached the limit set by the broker case 148 : //--- Attempt to open an opposite order if hedging is disabled case 149 : //--- Attempt to close a position on a symbol contradicts the FIFO rule case 150 : return ERROR_CODE_PROCESSING_METHOD_EXIT; //--- Invalid trading request parameters case 3 : //--- Invalid price case 129 : //--- Invalid stop levels case 130 : //--- Invalid volume case 131 : //--- Not enough money to perform the operation case 134 : //--- Expirations are denied by broker case 147 : return ERROR_CODE_PROCESSING_METHOD_CORRECT; //--- Trade server is busy case 4 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- No connection to the trade server case 6 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Too frequent requests case 8 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- No price case 136 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Broker is busy case 137 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Too many requests case 141 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Modification denied because the order is too close to market case 145 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Trade context is busy case 146 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)1000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Trade timeout case 128 : //--- Price has changed case 135 : //--- New prices case 138 : return ERROR_CODE_PROCESSING_METHOD_REFRESH; //--- MQL5 #else //--- Auto trading disabled by the server case 10026 : return ERROR_CODE_PROCESSING_METHOD_DISABLE; //--- Request canceled by a trader case 10007 : //--- Request expired case 10012 : //--- Trading disabled case 10017 : //--- Market closed case 10018 : //--- Order status changed case 10023 : //--- Request unchanged case 10025 : //--- Request blocked for handling case 10028 : //--- Transaction is allowed for live accounts only case 10032 : //--- The maximum number of pending orders is reached case 10033 : //--- Reached the maximum order and position volume for this symbol case 10034 : //--- Invalid or prohibited order type case 10035 : //--- Position with the specified ID already closed case 10036 : //--- A close order is already present for a specified position case 10039 : //--- The maximum number of open positions is reached case 10040 : //--- Request to activate a pending order is rejected, the order is canceled case 10041 : //--- Request is rejected, because the rule "Only long positions are allowed" is set for the symbol case 10042 : //--- Request is rejected, because the rule "Only short positions are allowed" is set for the symbol case 10043 : //--- Request is rejected, because the rule "Only closing of existing positions is allowed" is set for the symbol case 10044 : //--- Request is rejected, because the rule "Only closing of existing positions by FIFO rule is allowed" is set for the symbol case 10045 : return ERROR_CODE_PROCESSING_METHOD_EXIT; //--- Requote case 10004 : //--- Request rejected case 10006 : //--- Prices changed case 10020 : return ERROR_CODE_PROCESSING_METHOD_REFRESH; //--- Invalid request case 10013 : //--- Invalid request volume case 10014 : //--- Invalid request price case 10015 : //--- Invalid request stop levels case 10016 : //--- Insufficient funds for request execution case 10019 : //--- Invalid order expiration in a request case 10022 : //--- The specified type of order execution by balance is not supported case 10030 : //--- Closed volume exceeds the current position volume case 10038 : return ERROR_CODE_PROCESSING_METHOD_CORRECT; //--- No quotes to process the request case 10021 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT; //--- Too frequent requests case 10024 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- An order or a position is frozen case 10029 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT; //--- Request handling error case 10011 : return ERROR_CODE_PROCESSING_METHOD_PENDING; //--- Auto trading disabled by the client terminal case 10027 : return ERROR_CODE_PROCESSING_METHOD_PENDING; //--- No connection to the trade server case 10031 : return ERROR_CODE_PROCESSING_METHOD_PENDING; //--- Order placed case 10008 : //--- Request executed case 10009 : //--- Request executed partially case 10010 : #endif //--- "OK" default: break; } return ERROR_CODE_PROCESSING_METHOD_OK; } //+------------------------------------------------------------------+

Aquí, todo es muy sencillo: transmitimos al método el código obtenido

del servidor después de que la solicitud haya sido enviada a este. A continuación, los códigos cuya obtención da la posibilidad de

corregir el error serán procesados con el método de corrección de errores; asimismo, los códigos que necesitan la actualización de datos y

el envío repetido de solicitud serán procesados de la forma correspondiente, etcétera.

Dado que los servidores de MQL5 y MQL4 retornan

códigos de error diferentes, en el método también se organiza la compilación condicional para MQL4

y MQL5.

Todos los códigos que requieren un procesamiento del mismo

tipo han sido agrupados en el mismo case del operador switch,

y retornan un método único para todos en cuanto al procesamiento del código de retorno del servidor comercial.

Implementación del código de procesamiento de errores del servidor comercial:

//+------------------------------------------------------------------+ //| Correct errors | //+------------------------------------------------------------------+ ENUM_ERROR_CODE_PROCESSING_METHOD CTrading::RequestErrorsCorrecting(MqlTradeRequest &request, const ENUM_ORDER_TYPE order_type, const uint spread_multiplier, CSymbol *symbol_obj, CTradeObj *trade_obj) { //--- The empty error list means no errors are detected, return success int total=this.m_list_errors.Total(); if(total==0) return ERROR_CODE_PROCESSING_METHOD_OK; //--- Trading is disabled for the current account //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_ACCOUNT_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_ACCOUNT_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading on the trading server side is disabled for EAs on the current account //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_ACCOUNT_EA_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_ACCOUNT_EA_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading operations are disabled in the terminal //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_TERMINAL_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TERMINAL_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading operations are disabled for the EA //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_EA_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_EA_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Disable trading on a symbol //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Close only //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_CLOSEONLY)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_CLOSEONLY); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Market orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_MARKET_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_MARKET_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Limit orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_LIMIT_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_LIMIT_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Stop orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_STOP_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_STOP_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- StopLimit orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_STOP_LIMIT_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_STOP_LIMIT_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Sell only //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_SHORTONLY)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_SHORTONLY); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Buy only //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_LONGONLY)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_LONGONLY); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- CloseBy orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_CLOSE_BY_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_CLOSE_BY_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Exceeded maximum allowed aggregate volume of orders and positions in one direction //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_MAX_VOLUME_LIMIT_EXCEEDED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_MAX_VOLUME_LIMIT_EXCEEDED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Close by is disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_CLOSE_BY_ORDERS_DISABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_CLOSE_BY_ORDERS_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Symbols of opposite positions are not equal //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_CLOSE_BY_SYMBOLS_UNEQUAL)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_CLOSE_BY_SYMBOLS_UNEQUAL); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Unsupported price parameter type in a request //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_UNSUPPORTED_PRICE_TYPE_IN_REQ)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_UNSUPPORTED_PRICE_TYPE_IN_REQ); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading disabled for the EA until the reason is eliminated //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_TRADING_DISABLE)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TRADING_DISABLE); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- The maximum number of pending orders is reached //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(10033)) { trade_obj.SetResultRetcode(10033); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Reached the maximum order and position volume for this symbol //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(10034)) { trade_obj.SetResultRetcode(10034); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Correcting trading request parameters //--- Price, according to which stop orders are placed double price_set=(this.IsPresentErrorFlag(TRADE_REQUEST_ERR_FLAG_PRICE_ERROR) ? request.price : request.stoplimit); //--- First, adjust stop orders relative to the order/position level if(this.IsPresentErorCode(MSG_LIB_TEXT_SL_LESS_STOP_LEVEL)) request.sl=this.CorrectStopLoss(order_type,price_set,request.sl,symbol_obj,spread_multiplier); if(this.IsPresentErorCode(MSG_LIB_TEXT_TP_LESS_STOP_LEVEL)) request.tp=this.CorrectTakeProfit(order_type,price_set,request.tp,symbol_obj,spread_multiplier); //--- Pending orders price double shift=0; if(this.IsPresentErrorFlag(TRADE_REQUEST_ERR_FLAG_PRICE_ERROR)) { price_set=request.price; request.price=this.CorrectPricePending(order_type,price_set,0,symbol_obj,spread_multiplier); shift=request.price-price_set; //--- If this is not a stop limit order, move stop orders by the calculated correcting order level shift if(request.stoplimit==0) { if(request.sl>0) request.sl=this.CorrectStopLoss(order_type,request.price,request.sl+shift,symbol_obj,spread_multiplier); if(request.tp>0) request.tp=this.CorrectTakeProfit(order_type,request.price,request.tp+shift,symbol_obj,spread_multiplier); } } //--- The specified type of order execution by balance is not supported if(this.IsPresentErorCode(10030)) request.type_filling=symbol_obj.GetCorrectTypeFilling(); //--- Invalid order expiration in a request - if(this.IsPresentErorCode(10022)) { //--- if the expiration type is not supported as set by the expiration date and the expiration data is defined, reset the expiration date if(!symbol_obj.IsExpirationModeSpecified() && request.expiration>0) request.expiration=0; } //--- View the list of remaining errors and correct trading request parameters for(int i=0;i<total;i++) { int err=this.m_list_errors.At(i); if(err==NULL) continue; switch(err) { //--- Correct an invalid volume and disabling stop levels in a trading request case MSG_LIB_TEXT_REQ_VOL_LESS_MIN_VOLUME : case MSG_LIB_TEXT_REQ_VOL_MORE_MAX_VOLUME : case MSG_LIB_TEXT_INVALID_VOLUME_STEP : request.volume=symbol_obj.NormalizedLot(request.volume); break; case MSG_SYM_SL_ORDER_DISABLED : request.sl=0; break; case MSG_SYM_TP_ORDER_DISABLED : request.tp=0; break; //--- If unable to select the position lot, return "abort trading attempt" since the funds are insufficient even for the minimum lot case MSG_LIB_TEXT_NOT_ENOUTH_MONEY_FOR : request.volume=this.CorrectVolume(request.price,order_type,symbol_obj,DFUN); if(request.volume==0) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_NOT_POSSIBILITY_CORRECT_LOT); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; break; } //--- No quotes to process the request case 10021 : trade_obj.SetResultRetcode(10021); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT - wait 5 seconds //--- No connection to the trade server case 10031 : trade_obj.SetResultRetcode(10031); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT - wait 5 seconds //--- Proximity to the order activation level is handled by five-second waiting - during this time, the price may go beyond the freeze level case MSG_LIB_TEXT_SL_LESS_FREEZE_LEVEL : case MSG_LIB_TEXT_TP_LESS_FREEZE_LEVEL : case MSG_LIB_TEXT_PR_LESS_FREEZE_LEVEL : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT - wait 5 seconds default: break; } } //--- No errors - return ОК trade_obj.SetResultRetcode(0); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_OK; } //+------------------------------------------------------------------+

En el listado del método, en los comentarios al código, se han descrito todas las acciones referentes al procesamiento de los errores retornados por el servidor comercial.

Implementación del método privado para la apertura de posiciones:

//+------------------------------------------------------------------+ //| Open a position | //+------------------------------------------------------------------+ template<typename SL,typename TP> bool CTrading::OpenPosition(const ENUM_POSITION_TYPE type, const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX) { //--- Set the trading request result as 'true' and the error flag as "no errors" bool res=true; this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_NO_ERROR; ENUM_ORDER_TYPE order_type=(ENUM_ORDER_TYPE)type; ENUM_ACTION_TYPE action=(ENUM_ACTION_TYPE)order_type; //--- Get a symbol object by a symbol name. If failed to get CSymbol *symbol_obj=this.m_symbols.GetSymbolObjByName(symbol); //--- If failed to get - write the "internal error" flag, display the message in the journal and return 'false' if(symbol_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_SYM_OBJ)); return false; } //--- get a trading object from a symbol object CTradeObj *trade_obj=symbol_obj.GetTradeObj(); //--- If failed to get - write the "internal error" flag, display the message in the journal and return 'false' if(trade_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_TRADE_OBJ)); return false; } //--- Set the prices //--- If failed to set - write the "internal error" flag, set the error code in the return structure, //--- display the message in the journal and return 'false' if(!this.SetPrices(order_type,0,sl,tp,0,DFUN,symbol_obj)) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; trade_obj.SetResultRetcode(10021); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(10021)); // No quotes to process the request return false; } //--- Write the volume to the request structure this.m_request.volume=volume; //--- Get the method of handling errors from the CheckErrors() method while checking for errors in the request parameters ENUM_ERROR_CODE_PROCESSING_METHOD method=this.CheckErrors(this.m_request.volume,symbol_obj.Ask(),action,order_type,symbol_obj,trade_obj,DFUN,0,this.m_request.sl,this.m_request.tp); //--- In case of trading limitations, funds insufficiency, //--- if there are limitations by StopLevel or FreezeLevel ... if(method!=ERROR_CODE_PROCESSING_METHOD_OK) { //--- If trading is completely disabled, set the error code to the return structure, //--- display a journal message, play the error sound and exit if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TRADING_DISABLE); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_DISABLE)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "abort trading operation" - set the last error code to the return structure, //--- display a journal message, play the error sound and exit if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_OPERATION_ABORTED)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "waiting" - set the last error code to the return structure and display the message in the journal if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); //--- Instead of creating a pending request, we temporarily wait the required time period (the CheckErrors() method result is returned) ::Sleep(method); //--- after waiting, update all data symbol_obj.Refresh(); } //--- If the check result is "create a pending request", do nothing temporarily if(this.m_err_handling_behavior==ERROR_HANDLING_BEHAVIOR_PENDING_REQUEST) { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); } } //--- In the loop by the number of attempts for(int i=0;i<this.m_total_try;i++) { //--- Send the request res=trade_obj.OpenPosition(type,this.m_request.volume,this.m_request.sl,this.m_request.tp,magic,comment,deviation); //--- If the request is executed successfully or the asynchronous order sending mode is set, play the success sound //--- set for a symbol trading object for this type of trading operation and return 'true' if(res || trade_obj.IsAsyncMode()) { if(this.IsUseSounds()) trade_obj.PlaySoundSuccess(action,order_type); return true; } //--- If the request is not successful, play the error sound set for a symbol trading object for this type of trading operation else { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRY_N),string(i+1),". ",CMessage::Text(MSG_LIB_SYS_ERROR),": ",CMessage::Text(trade_obj.GetResultRetcode())); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); //--- Get the error handling method method=this.ResultProccessingMethod(trade_obj.GetResultRetcode()); //--- If "Disable trading for the EA" is received as a result of sending a request, enable the disabling flag and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { this.SetTradingDisableFlag(true); break; } //--- If "Exit the trading method" is received as a result of sending a request, end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { break; } //--- If "Correct the parameters and repeat" is received as a result of sending a request - //--- correct the parameters and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_CORRECT) { this.RequestErrorsCorrecting(this.m_request,order_type,trade_obj.SpreadMultiplier(),symbol_obj,trade_obj); continue; } //--- If "Update data and repeat" is received as a result of sending a request - //--- update data and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_REFRESH) { symbol_obj.Refresh(); continue; } //--- If "Wait and repeat" is received as a result of sending a request - //--- in this implementation, we wait the number of milliseconds equal to the 'method' value and move on to the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_WAIT) { ::Sleep(method); continue; } //--- If "Create a pending request" is received as a result of sending a request - //--- create a pending request with the trading request parameters and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_PENDING) { break; } } } //--- Return the result of sending a trading request in a symbol trading object return res; } //+------------------------------------------------------------------+Este método ha sido comentado con detalle directamente en el listado, y será utilizado para abrir las posiciones Buy y Sell:

//+------------------------------------------------------------------+ //| Open Buy position | //+------------------------------------------------------------------+ template<typename SL,typename TP> bool CTrading::OpenBuy(const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX) { //--- Return the result of sending a trading request from the OpenPosition() method return this.OpenPosition(POSITION_TYPE_BUY,volume,symbol,magic,sl,tp,comment,deviation); } //+------------------------------------------------------------------+ //| Open a Sell position | //+------------------------------------------------------------------+ template<typename SL,typename TP> bool CTrading::OpenSell(const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX) { //--- Return the result of sending a trading request from the OpenPosition() method return this.OpenPosition(POSITION_TYPE_SELL,volume,symbol,magic,sl,tp,comment,deviation); } //+------------------------------------------------------------------+

En estos métodos, simplemente se llama el método privado general para la apertura de posiciones con

indicación del tipo de posición abierta.

Implementación del método privado para colocar órdenes pendientes:

//+------------------------------------------------------------------+ //| Place a pending order | //+------------------------------------------------------------------+ template<typename PS,typename PL,typename SL,typename TP> bool CTrading::PlaceOrder(const ENUM_ORDER_TYPE order_type, const double volume, const string symbol, const PS price_stop, const PL price_limit=0, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { bool res=true; this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_NO_ERROR; ENUM_ACTION_TYPE action=(ENUM_ACTION_TYPE)order_type; //--- Get a symbol object by a symbol name CSymbol *symbol_obj=this.m_symbols.GetSymbolObjByName(symbol); if(symbol_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_SYM_OBJ)); return false; } //--- Get a trading object from a symbol object CTradeObj *trade_obj=symbol_obj.GetTradeObj(); if(trade_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_TRADE_OBJ)); return false; } //--- Set the prices //--- If failed to set - write the "internal error" flag, set the error code in the return structure, //--- display the message in the journal and return 'false' if(!this.SetPrices(order_type,price_stop,sl,tp,price_limit,DFUN,symbol_obj)) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; trade_obj.SetResultRetcode(10021); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(10021)); // No quotes to process the request return false; } //--- In case of trading limitations, funds insufficiency, //--- there are limitations on StopLevel - play the error sound and exit this.m_request.volume=volume; this.m_request.type_filling=type_filling; this.m_request.type_time=type_time; this.m_request.expiration=expiration; ENUM_ERROR_CODE_PROCESSING_METHOD method=this.CheckErrors(this.m_request.volume, this.m_request.price, action, order_type, symbol_obj, trade_obj, DFUN, this.m_request.stoplimit, this.m_request.sl, this.m_request.tp); if(method!=ERROR_CODE_PROCESSING_METHOD_OK) { //--- If trading is completely disabled if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TRADING_DISABLE); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_DISABLE)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "abort trading operation" - set the last error code to the return structure, //--- display a journal message, play the error sound and exit if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_OPERATION_ABORTED)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "waiting" - set the last error code to the return structure and display the message in the journal if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); //--- Instead of creating a pending request, we temporarily wait the required time period (the CheckErrors() method result is returned) ::Sleep(method); symbol_obj.Refresh(); } //--- If the check result is "create a pending request", do nothing temporarily if(this.m_err_handling_behavior==ERROR_HANDLING_BEHAVIOR_PENDING_REQUEST) { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); } } //--- In the loop by the number of attempts for(int i=0;i<this.m_total_try;i++) { //--- Send the request res=trade_obj.SetOrder(order_type, this.m_request.volume, this.m_request.price, this.m_request.sl, this.m_request.tp, this.m_request.stoplimit, magic, comment, this.m_request.expiration, this.m_request.type_time, this.m_request.type_filling); //--- If the request is executed successfully or the asynchronous order sending mode is set, play the success sound //--- set for a symbol trading object for this type of trading operation and return 'true' if(res || trade_obj.IsAsyncMode()) { if(this.IsUseSounds()) trade_obj.PlaySoundSuccess(action,order_type); return true; } //--- If the request is not successful, play the error sound set for a symbol trading object for this type of trading operation else { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRY_N),string(i+1),". ",CMessage::Text(MSG_LIB_SYS_ERROR),": ",CMessage::Text(trade_obj.GetResultRetcode())); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); method=this.ResultProccessingMethod(trade_obj.GetResultRetcode()); //--- If "Disable trading for the EA" is received as a result of sending a request, enable the disabling flag and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { this.SetTradingDisableFlag(true); break; } //--- If "Exit the trading method" is received as a result of sending a request, end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { break; } //--- If "Correct the parameters and repeat" is received as a result of sending a request - //--- correct the parameters and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_CORRECT) { this.RequestErrorsCorrecting(this.m_request,order_type,trade_obj.SpreadMultiplier(),symbol_obj,trade_obj); continue; } //--- If "Update data and repeat" is received as a result of sending a request - //--- update data and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_REFRESH) { symbol_obj.Refresh(); continue; } //--- If "Wait and repeat" is received as a result of sending a request - //--- in this implementation, we wait the number of milliseconds equal to the 'method' value and move on to the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_WAIT) { Sleep(method); continue; } //--- If "Create a pending request" is received as a result of sending a request - //--- create a pending request with the trading request parameters and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_PENDING) { break; } } } //--- Return the result of sending a trading request in a symbol trading object return res; } //+------------------------------------------------------------------+

Este método ha sido comentado con detalle directamente en el listado, y será utilizado para establecer distintos tipos de órdenes pendientes:

//+------------------------------------------------------------------+ //| Place BuyStop pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceBuyStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_BUY_STOP,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place BuyLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceBuyLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_BUY_LIMIT,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place BuyStopLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename PL,typename SL,typename TP> bool CTrading::PlaceBuyStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { #ifdef __MQL5__ //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_BUY_STOP_LIMIT,volume,symbol,price_stop,price_limit,sl,tp,magic,comment,expiration,type_time,type_filling); //--- MQL4 #else return true; #endif } //+------------------------------------------------------------------+ //| Place SellStop pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceSellStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_SELL_STOP,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place SellLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceSellLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_SELL_LIMIT,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place SellStopLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename PL,typename SL,typename TP> bool CTrading::PlaceSellStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { #ifdef __MQL5__ //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_SELL_STOP_LIMIT,volume,symbol,price_stop,price_limit,sl,tp,magic,comment,expiration,type_time,type_filling); //--- MQL4 #else return true; #endif } //+------------------------------------------------------------------+

Los demás métodos para el cierre de posiciones y la eliminación de órdenes pendientes, así como los métodos de modificación de posiciones y órdenes han sido creados de forma análoga a los métodos privados para la apertura de posiciones/colocación de órdenes pendientes. Todos los códigos han sido comentados con detalle, por lo que el lector los podrá estudiar por sí mismo en los archivos adjuntos al final del artículo.

Podemos dar por finalizado el trabajo con la clase comercial en esta etapa.

Ahora, debemos introducir unos pequeños cambios en la clase del objeto principal de la biblioteca CEngine.

Si el nivel mínimo de colocación de órdenes stop y órdenes pendientes (StopLevel) tiene una magnitud flotante, deberemos indicar el

multiplicador de spread, porque con frecuencia en semejantes situaciones se usa un spread multiplicado por cierta magnitud para indicar

la distancia permitida en la colocación de stops. Partiendo de esto, necesitaremos un método que nos permita establecer un multiplicador

de spread, para indicarlo en la clase comercial.

En la sección pública de la clase, declaramos

este método:

//--- Set the spread multiplier for symbol trading objects in the symbol collection void SetSpreadMultiplier(const uint value=1,const string symbol=NULL) { this.m_trading.SetSpreadMultiplier(value,symbol); } //--- Open (1) Buy, (2) Sell position

El método simplemente llama al método homónimo de la clase comercial que hemos analizado en el artículo anterior, y permite establecer tanto un multiplicador común para todos los símbolos utilizados, como multiplicadores individuales para los símbolos indicados.

Dado que la clase comercial en breve usará un temporizador para trabajar con solicitudes pendientes,

vamos a crear

en el constructor de la clase CEngine un nuevo contador del temporizador para la

clase comercial:

//+------------------------------------------------------------------+ //| CEngine constructor | //+------------------------------------------------------------------+ CEngine::CEngine() : m_first_start(true), m_last_trade_event(TRADE_EVENT_NO_EVENT), m_last_account_event(WRONG_VALUE), m_last_symbol_event(WRONG_VALUE), m_global_error(ERR_SUCCESS) { this.m_is_hedge=#ifdef __MQL4__ true #else bool(::AccountInfoInteger(ACCOUNT_MARGIN_MODE)==ACCOUNT_MARGIN_MODE_RETAIL_HEDGING) #endif; this.m_is_tester=::MQLInfoInteger(MQL_TESTER); this.m_list_counters.Sort(); this.m_list_counters.Clear(); this.CreateCounter(COLLECTION_ORD_COUNTER_ID,COLLECTION_ORD_COUNTER_STEP,COLLECTION_ORD_PAUSE); this.CreateCounter(COLLECTION_ACC_COUNTER_ID,COLLECTION_ACC_COUNTER_STEP,COLLECTION_ACC_PAUSE); this.CreateCounter(COLLECTION_SYM_COUNTER_ID1,COLLECTION_SYM_COUNTER_STEP1,COLLECTION_SYM_PAUSE1); this.CreateCounter(COLLECTION_SYM_COUNTER_ID2,COLLECTION_SYM_COUNTER_STEP2,COLLECTION_SYM_PAUSE2); this.CreateCounter(COLLECTION_REQ_COUNTER_ID,COLLECTION_REQ_COUNTER_STEP,COLLECTION_REQ_PAUSE); ::ResetLastError(); #ifdef __MQL5__ if(!::EventSetMillisecondTimer(TIMER_FREQUENCY)) { ::Print(DFUN_ERR_LINE,CMessage::Text(MSG_LIB_SYS_FAILED_CREATE_TIMER),(string)::GetLastError()); this.m_global_error=::GetLastError(); } //---__MQL4__ #else if(!this.IsTester() && !::EventSetMillisecondTimer(TIMER_FREQUENCY)) { ::Print(DFUN_ERR_LINE,CMessage::Text(MSG_LIB_SYS_FAILED_CREATE_TIMER),(string)::GetLastError()); this.m_global_error=::GetLastError(); } #endif //--- } //+------------------------------------------------------------------+

En el temporizador de la clase CEngine, añadimos el bloque de trabajo con el temporizador de la clase comercial:

//+------------------------------------------------------------------+ //| CEngine timer | //+------------------------------------------------------------------+ void CEngine::OnTimer(void) { //--- Timer of the collections of historical orders and deals, as well as of market orders and positions int index=this.CounterIndex(COLLECTION_ORD_COUNTER_ID); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If unpaused, work with the order, deal and position collections events if(counter.IsTimeDone()) this.TradeEventsControl(); } //--- If this is a tester, work with collection events by tick else this.TradeEventsControl(); } } //--- Account collection timer index=this.CounterIndex(COLLECTION_ACC_COUNTER_ID); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If unpaused, work with the account collection events if(counter.IsTimeDone()) this.AccountEventsControl(); } //--- If this is a tester, work with collection events by tick else this.AccountEventsControl(); } } //--- Timer 1 of the symbol collection (updating symbol quote data in the collection) index=this.CounterIndex(COLLECTION_SYM_COUNTER_ID1); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If the pause is over, update quote data of all symbols in the collection if(counter.IsTimeDone()) this.m_symbols.RefreshRates(); } //--- In case of a tester, update quote data of all collection symbols by tick else this.m_symbols.RefreshRates(); } } //--- Timer 2 of the symbol collection (updating all data of all symbols in the collection and tracking symbl and symbol search events in the market watch window) index=this.CounterIndex(COLLECTION_SYM_COUNTER_ID2); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If the pause is over if(counter.IsTimeDone()) { //--- update data and work with events of all symbols in the collection this.SymbolEventsControl(); //--- When working with the market watch list, check the market watch window events if(this.m_symbols.ModeSymbolsList()==SYMBOLS_MODE_MARKET_WATCH) this.MarketWatchEventsControl(); } } //--- If this is a tester, work with events of all symbols in the collection by tick else this.SymbolEventsControl(); } } //--- Trading class timer index=this.CounterIndex(COLLECTION_REQ_COUNTER_ID); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If unpaused, work with the list of pending requests if(counter.IsTimeDone()) this.m_trading.OnTimer(); } //--- In case of the tester, work with the list of pending orders by tick else this.m_trading.OnTimer(); } } } //+------------------------------------------------------------------+

Cambiamos ligeramente el método de cierre total de posiciones:

//+------------------------------------------------------------------+ //| Close a position in full | //+------------------------------------------------------------------+ bool CEngine::ClosePosition(const ulong ticket,const string comment=NULL,const ulong deviation=ULONG_MAX) { return this.m_trading.ClosePosition(ticket,WRONG_VALUE,comment,deviation); } //+------------------------------------------------------------------+

Dado que el método de cierre de posiciones es ahora único para el cierre parcial y total, deberemos transmitir -1 como volumen para cerrar una

posición por completo, lo cual hacemos aquí.

Aquí finalizan los cambios y mejoras en cuanto a la implementación del procesamiento de los códigos de retorno del servidor comercial.

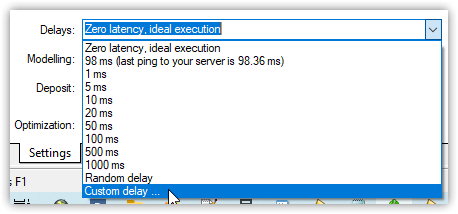

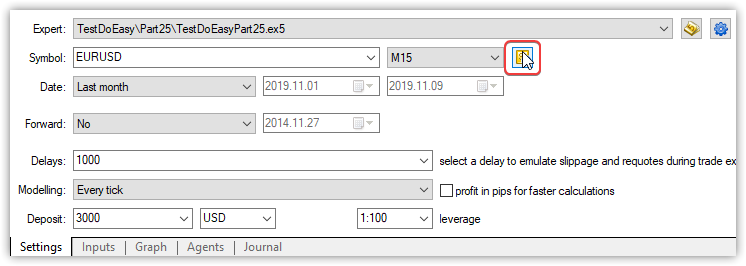

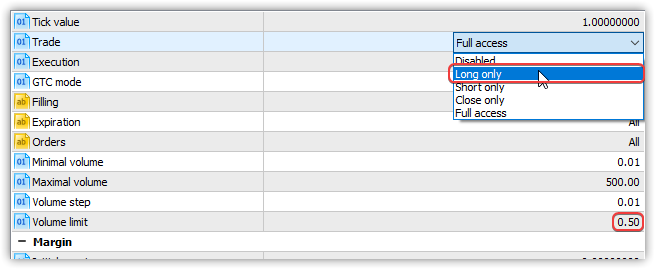

Simulación