On the unequal probability of a price move up or down

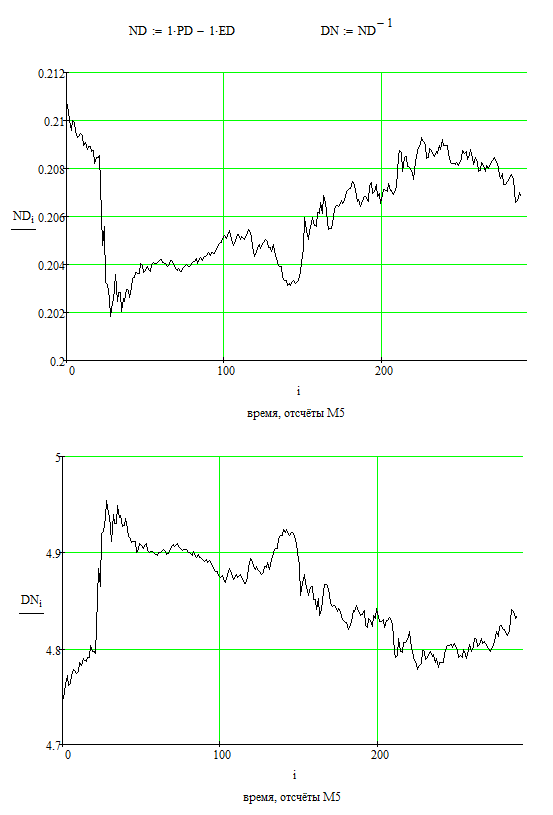

Let's do a simple"coordinate transformation". Namely, let's move from our existing quote currency, the Fed dollar (designated as D in these ED and PD pairs on the charts), to a new quote currency: N.

Let us introduce the new quote currency as follows: ND = PD - ED.

What is the convenience of such a presentation? Two things.

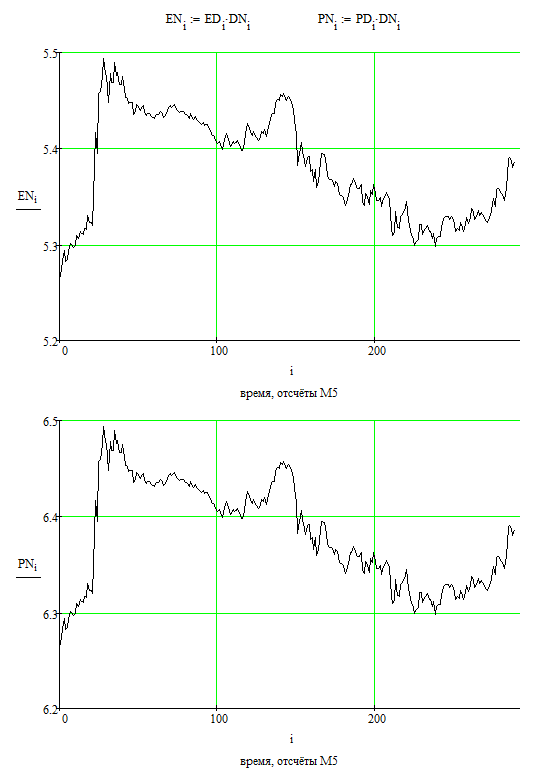

Firstly, the shapes of the graphs of the euro/new currency-quote and pound/new currency-quote pairs will be identical, namely linked by the simple equation PN = EN + 1, following from the definition of the "quote currency" N.

Secondly, these new pairs (EN and PN), and incidentally DN, can be traded directly because it is not difficult to express their increments as linear combinations of ED and PD increments.

Now watch your hands.

Consideration 1. If we consider the EURUSD EURGBP pair chart as an independent value without any notion that we are considering any instruments from which this very EURGBP can be expressed, then it is kind of obvious that the probability of EURGBP going "up" and "down" is the same: 50%.

Consideration 2. Nothing prevents us from considering the EN instrument chart as an independent variable. Exactly on the same grounds, with the same conclusion: the probabilities of upward and downward movements are the same.

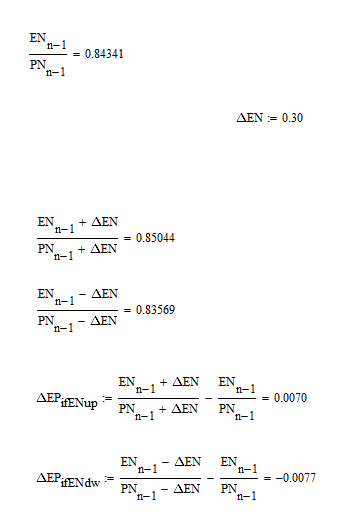

Consideration 3. The above considerations 1 and 2 are not consistent with each other. Let us show this.

My counter i here varies from 0 to n-1, where n = 289, the value 0 corresponds to the "leftmost" count, farthest in the past, the value 288 corresponds to the "rightmost" count, the freshest in the consideration.

So. Rightmost" value of EURGBP: 0.84341. Let's check EN for some deltaEN = 0.3 (in plus and minus). What do we see? That the values of deltaEP, that correspond to the increasing EN (i.e. positive deltaEN = 0.3) and declining EN (i.e. negative deltaEN = -0.3) are not equal to each other:

Question: how is this possible? If we consider that movements of some magnitude up or down for EN are equally probable, we have asymmetry in EP. If we assume that the movements in the EP pair by some value are equally probable, we have asymmetry in EN.

The answer is that the market is a very clever construct. It is efficient, in the sense of strictly making sure that naive "traders" do not have any opportunity to make money. Therefore, the probabilities of "up" and "down" are not really equal, neither in the EP pair, nor in the EN pair, nor in any other pair. Only the possibilities to make or lose money are equal (without taking into account spreads, commissions, etc.). Simply put, it is necessary to take into account the change in the value of the quote currency.

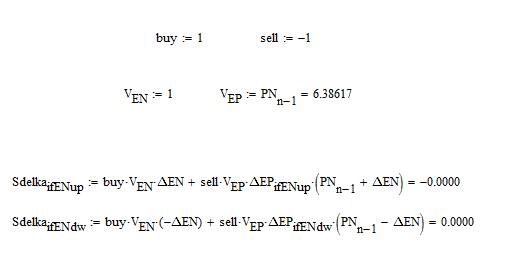

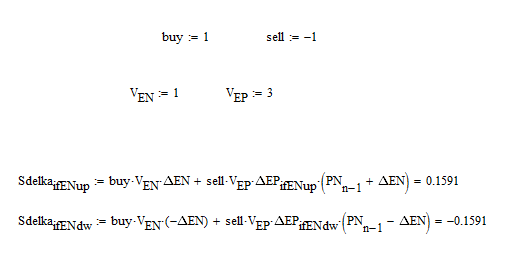

To make it clear, let's form a virtual transaction to buy EN, and simultaneously sell EP, and we will calculate profit or loss in "pips" of the currency N (it does not matter, we can go to "pips" of dollar):

If the volume of transaction on EURGBP pair make PN-right-edge times more than the volume of transaction on EN pair, then we will have a perfect match: zero profits and losses. For unequal movements of EURGBP (by 70 and 77 pips).

For other ratios there will be non zeros:

Thus, it is obvious that the probabilities of "up" and "down" (by some predetermined amount) are not equal (for any pair).

This simplest conclusion is non-obvious to the masses, and I suppose will provoke discussion.

In my opinion, the asymmetry is so minuscule that there is no point in taking it into account.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

Good afternoon.

On the eve of the new year, I have decided to make one of the obvious conclusions about the nature of the market public. This is particularly useful as there are very few any physically meaningful ideas on the forum.

Today I intend to refute with simple considerations one of the common fallacies, that a chart of an arbitrarily taken currency pair has equal probabilities (50% each) of going up and down when considered over a sufficiently long time interval.

Let us consider 289 samples in the M5 timeframe (i.e. 1 day) of EURUSD and GBPUSD price charts: