LiteFinance / Profil

The online ECN broker LiteFinance (ex. LiteForex) has been providing its clients access to Tier 1 liquidity in the currency, commodity, and stock market since 2005. All major currency pairs and cross rates, oil, precious metals, stock indexes, blue chips, and the largest set of cryptocurrency pairs can be traded at LiteFinance (ex. LiteForex).

LiteFinance

Forecast for EUR/USD: whose grave is deeper?

Fundamental forecast for dollar for today

Will euro continue to rally or will EUR/USD consolidate?

The Fed was the main player to fight previous recessions, but now it plays a supporting role. Only the public health sector’s advancement will indicate an economic recovery. No easy money will protect people from COVID-19. At the latest FOMC’s meeting Jerome Powell said that “social distancing measures and a fast reopening of the economy actually go together. They’re not in competition with each other.” The Fed didn’t ask for a new lockdown but admitted that leading indicators started blinking red amid the worsening epidemiological situation. That’s good news for US stocks but bad news for the US dollar.

The Fed made it clear that unprecedented economic support measures would be sustained by extending repurchase agreements and temporary U.S. dollar liquidity swap lines through March 2021. Sellers of securities are having difficulties going against the aggressively disposed Fed, so S&P 500’s growth and the fall of treasuries yield to historical lows look logical. The greenback fell too, but EUR/USD’s failure to break an important level of 1.18 makes us doubt that big speculators are ready to continue the rally. At least now.

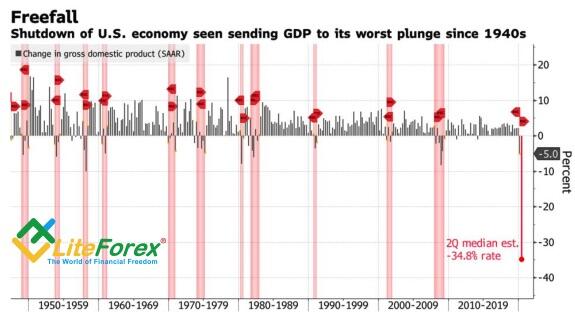

The euro’s fast growth in July attracted much attention and the number of bulls is growing. The main question is whether we should buy “at market” or wait for a pullback. The answer should be looked for in the stats on the US and German GDPs in Q2. The Reuters experts expect that the German economy will decline 9% q/q and 11.3% y-o-y. These are terrible expectations, but compare them with minus 34.1% in the USA and you’ll remember that it’s all relative. It’s been the worst result in the after-war period, which is three times worse than the 1958 anti-record of 10%.

No, it doesn’t mean the US GDP will lose a third of its value: for that to happen, 1 year will be required because its performance will be compared with April-June 2019. Still, the scale of recession is a question of principle for EUR/USD. A deeper hole makes is harder to get out. The euro will grow to $1.182 and $1.187 only if upbeat data on Germany are combined with pessimistic stats on the US. Otherwise, we have to be ready for higher volatility and consolidation.

Bulls will start fixing profits due to anxious signals from Europe and Asia. The number of new coronavirus cases and the unemployment rate in Spain are growing while in France, consumer confidence is falling. The Chinese economy slowed down in July according to the Bloomberg leading indicators. The US-China tense relations should be considered too: the trading conflict risks resuming as Beijing isn’t rushing to meet its obligation to increase imports of U.S. goods.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/forecast-for-eurusd-whose-grave-is-deeper/?uid=285861726&cid=79634

US GDP dynamics

Fundamental forecast for dollar for today

Will euro continue to rally or will EUR/USD consolidate?

The Fed was the main player to fight previous recessions, but now it plays a supporting role. Only the public health sector’s advancement will indicate an economic recovery. No easy money will protect people from COVID-19. At the latest FOMC’s meeting Jerome Powell said that “social distancing measures and a fast reopening of the economy actually go together. They’re not in competition with each other.” The Fed didn’t ask for a new lockdown but admitted that leading indicators started blinking red amid the worsening epidemiological situation. That’s good news for US stocks but bad news for the US dollar.

The Fed made it clear that unprecedented economic support measures would be sustained by extending repurchase agreements and temporary U.S. dollar liquidity swap lines through March 2021. Sellers of securities are having difficulties going against the aggressively disposed Fed, so S&P 500’s growth and the fall of treasuries yield to historical lows look logical. The greenback fell too, but EUR/USD’s failure to break an important level of 1.18 makes us doubt that big speculators are ready to continue the rally. At least now.

The euro’s fast growth in July attracted much attention and the number of bulls is growing. The main question is whether we should buy “at market” or wait for a pullback. The answer should be looked for in the stats on the US and German GDPs in Q2. The Reuters experts expect that the German economy will decline 9% q/q and 11.3% y-o-y. These are terrible expectations, but compare them with minus 34.1% in the USA and you’ll remember that it’s all relative. It’s been the worst result in the after-war period, which is three times worse than the 1958 anti-record of 10%.

No, it doesn’t mean the US GDP will lose a third of its value: for that to happen, 1 year will be required because its performance will be compared with April-June 2019. Still, the scale of recession is a question of principle for EUR/USD. A deeper hole makes is harder to get out. The euro will grow to $1.182 and $1.187 only if upbeat data on Germany are combined with pessimistic stats on the US. Otherwise, we have to be ready for higher volatility and consolidation.

Bulls will start fixing profits due to anxious signals from Europe and Asia. The number of new coronavirus cases and the unemployment rate in Spain are growing while in France, consumer confidence is falling. The Chinese economy slowed down in July according to the Bloomberg leading indicators. The US-China tense relations should be considered too: the trading conflict risks resuming as Beijing isn’t rushing to meet its obligation to increase imports of U.S. goods.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/forecast-for-eurusd-whose-grave-is-deeper/?uid=285861726&cid=79634

US GDP dynamics

LiteFinance

Forecast for EUR/USD: Dollar breaks the mould

Fundamental forecast for dollar for today

Every recession has its own trick

Crises are the moments of breaking memory patterns. The current economic recession provoked by the pandemic is no exception. Take the Dollar smile theory, for example. According to it, the greenback grows on a bigger demand for safe haven assets, falls on the Fed’s large monetary stimuli and rises again on expectations of the US GDP’s better performance versus its peers. July may become the worst month for the USD index in the past decade, even more so because something went wrong at the last stage. The mould is broken. The divergence in economic growths is favourable to EUR/USD.

Investors inevitably turn back to past experience: the 2007-2009 global economic crisis, the Great Depression of 1930, the 1918 flu pandemic. The previous recession is still fresh in our minds, so the Fed reacted naturally with a large monetary stimulus. Financial markets thought of the central bank’s 2008 success, put on rose-coloured glasses and believed it was time to buy risks. Now S&P 500 is concerned about what will happen to the economy and corporate benefits in Q3. The stocks have been outrunning themselves for a long time. The question is whether they have got too high.

Crises do break memory patterns, but there is a moment when a new consensus opinion of risk premiums is reached as investors react to a new global picture. I suppose the French-German fiscal stimulus project was that kind of a moment. Before the pandemic, Europe had been considered as the world’s main economic brake. Fiscal consolidation programs, Brexit, EU-scepticism, rumours of EU disintegration and, finally, the export-oriented region’s distress caused by the US-China trade wars urged speculators to sell the euro actively. The pandemic turned everything upside down, which is clearly seen in the forward market.

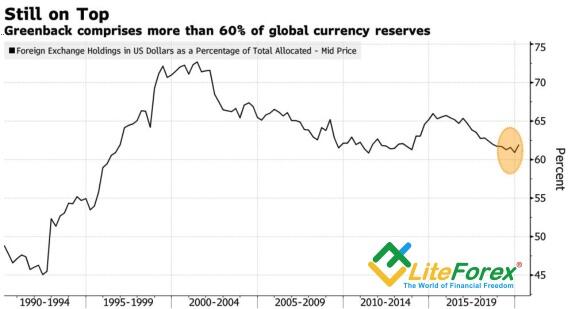

The single European currency isn’t led by American stock indexes any longer. What’s more, it is ready to withstand an eventual sell-out in the US stock market. International investors will move money from America to Europe because of S&P 500’s correction. Meanwhile, the dollar’s status of the world’s reserve currency will be undermined - this is what Goldman Sachs is trumpeting. GS believes that growing inflation and excessive government debt are the main reasons for the USD losing predominance in Fx transactions (88%) and gold reserves (62%).

According to the Goldman analysts, at the initial stage of recession Wall Street didn’t dare to say the Fed’s monetary stimulus would speed up PCE and CPI because they had already made a similar erroneous forecast in 2007-2009. However, investors’ are changing their minds. Inflation expectations are growing by leaps and bounds, real US bond yields are falling and the dollar is growing weaker. If the Fed shows tolerance of consumer prices growth at July’s meeting, a breakout of resistance levels at 1.1765 and 1.178 will allow EUR/USD to continue the rally.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/forecast-for-eurusd-dollar-breaks-the-mould/?uid=285861726&cid=79634

Dynamics of speculative positions in euro

Fundamental forecast for dollar for today

Every recession has its own trick

Crises are the moments of breaking memory patterns. The current economic recession provoked by the pandemic is no exception. Take the Dollar smile theory, for example. According to it, the greenback grows on a bigger demand for safe haven assets, falls on the Fed’s large monetary stimuli and rises again on expectations of the US GDP’s better performance versus its peers. July may become the worst month for the USD index in the past decade, even more so because something went wrong at the last stage. The mould is broken. The divergence in economic growths is favourable to EUR/USD.

Investors inevitably turn back to past experience: the 2007-2009 global economic crisis, the Great Depression of 1930, the 1918 flu pandemic. The previous recession is still fresh in our minds, so the Fed reacted naturally with a large monetary stimulus. Financial markets thought of the central bank’s 2008 success, put on rose-coloured glasses and believed it was time to buy risks. Now S&P 500 is concerned about what will happen to the economy and corporate benefits in Q3. The stocks have been outrunning themselves for a long time. The question is whether they have got too high.

Crises do break memory patterns, but there is a moment when a new consensus opinion of risk premiums is reached as investors react to a new global picture. I suppose the French-German fiscal stimulus project was that kind of a moment. Before the pandemic, Europe had been considered as the world’s main economic brake. Fiscal consolidation programs, Brexit, EU-scepticism, rumours of EU disintegration and, finally, the export-oriented region’s distress caused by the US-China trade wars urged speculators to sell the euro actively. The pandemic turned everything upside down, which is clearly seen in the forward market.

The single European currency isn’t led by American stock indexes any longer. What’s more, it is ready to withstand an eventual sell-out in the US stock market. International investors will move money from America to Europe because of S&P 500’s correction. Meanwhile, the dollar’s status of the world’s reserve currency will be undermined - this is what Goldman Sachs is trumpeting. GS believes that growing inflation and excessive government debt are the main reasons for the USD losing predominance in Fx transactions (88%) and gold reserves (62%).

According to the Goldman analysts, at the initial stage of recession Wall Street didn’t dare to say the Fed’s monetary stimulus would speed up PCE and CPI because they had already made a similar erroneous forecast in 2007-2009. However, investors’ are changing their minds. Inflation expectations are growing by leaps and bounds, real US bond yields are falling and the dollar is growing weaker. If the Fed shows tolerance of consumer prices growth at July’s meeting, a breakout of resistance levels at 1.1765 and 1.178 will allow EUR/USD to continue the rally.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/forecast-for-eurusd-dollar-breaks-the-mould/?uid=285861726&cid=79634

Dynamics of speculative positions in euro

LiteFinance

Forecast for EUR/USD: Will dollar correct?

Fundamental forecast for dollar for today

EUR/USD bears think a major part of negative information is factored in the quotes

The States’ inability to put an end to the pandemic may lead to the USD’s worst dynamics in the past 9 years. Not only gold has grown against the greenback in July, reaching a new record value. Almost everything has grown against the greenback. An increasing number of new Covid cases lets us think that controlling the virus in the USA is harder than in other countries. It cuts the efficiency of the US economy.

The main factors in the USD’s weakness are a bad epidemiological situation, China’s probable sales of US Treasuries, presidential election uncertainty, and fears that the Fed will continue monetary expansion and drop the federal funds rate below zero. It will hardly happen at FOMC’s meeting on 28-29 July, but obviously, the situation has changed for the worst since the last meeting.

Back in June, the number of Covid cases got stable. It was falling in New York and New Jersey, while Texas, Florida and California didn’t face the virus terror that they are in now. Still, the Fed’s forecast had already been pessimistic. Jerome Powell and his peers didn’t see any signs of the V-shape recovery the White House had been talking about. They rather appealed for fiscal stimulus and said the Central bank wasn’t able to deal alone with the pandemic. the Boston Fed President Eric Rosengren said in his latest interviews that he expected the same inflationary decline as in Europe, but the States weren’t as successful. American macro-indicators are still far from pre-crisis levels while the German Ifo Business Climate Index has exceeded them already.

The longer the epidemic lasts, the harder it will be for some sectors to recover. Millions of Americans will become jobless, businesses will go bankrupt and the banking system will be under a great stress. The economy is becoming less efficient, compared with competitors. This cannot but affect the currency rate. In the week ended 22 July, net USD shorts reached the highest level against 8 major currencies since April 2018.

The uncertainty around fiscal stimulus puts pressure on the greenback too. The Republicans proposed to increase the relief package by $1 trillion, cutting weekly unemployment benefits from $600 to $200. They believe the US has one foot in the pandemic and one foot in the recovery.

Still, no trend can do without correction. According to Rabobank, EUR/USD quotes have already considered both the probable worsening of US macro-statistics and the Fed’s downbeat expectations for GDP. The greenback may be given preference as a safe haven currency at any time, especially when US stock indexes aren’t willing to continue a rally. And that’s good for bulls! Retracements to $1.1655 and $1.158 will allow them to buy the euro cheaper.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/forecast-for-eurusd-will-dollar-correct/?uid=285861726&cid=79634

Dynamics of German business climate indexes

Fundamental forecast for dollar for today

EUR/USD bears think a major part of negative information is factored in the quotes

The States’ inability to put an end to the pandemic may lead to the USD’s worst dynamics in the past 9 years. Not only gold has grown against the greenback in July, reaching a new record value. Almost everything has grown against the greenback. An increasing number of new Covid cases lets us think that controlling the virus in the USA is harder than in other countries. It cuts the efficiency of the US economy.

The main factors in the USD’s weakness are a bad epidemiological situation, China’s probable sales of US Treasuries, presidential election uncertainty, and fears that the Fed will continue monetary expansion and drop the federal funds rate below zero. It will hardly happen at FOMC’s meeting on 28-29 July, but obviously, the situation has changed for the worst since the last meeting.

Back in June, the number of Covid cases got stable. It was falling in New York and New Jersey, while Texas, Florida and California didn’t face the virus terror that they are in now. Still, the Fed’s forecast had already been pessimistic. Jerome Powell and his peers didn’t see any signs of the V-shape recovery the White House had been talking about. They rather appealed for fiscal stimulus and said the Central bank wasn’t able to deal alone with the pandemic. the Boston Fed President Eric Rosengren said in his latest interviews that he expected the same inflationary decline as in Europe, but the States weren’t as successful. American macro-indicators are still far from pre-crisis levels while the German Ifo Business Climate Index has exceeded them already.

The longer the epidemic lasts, the harder it will be for some sectors to recover. Millions of Americans will become jobless, businesses will go bankrupt and the banking system will be under a great stress. The economy is becoming less efficient, compared with competitors. This cannot but affect the currency rate. In the week ended 22 July, net USD shorts reached the highest level against 8 major currencies since April 2018.

The uncertainty around fiscal stimulus puts pressure on the greenback too. The Republicans proposed to increase the relief package by $1 trillion, cutting weekly unemployment benefits from $600 to $200. They believe the US has one foot in the pandemic and one foot in the recovery.

Still, no trend can do without correction. According to Rabobank, EUR/USD quotes have already considered both the probable worsening of US macro-statistics and the Fed’s downbeat expectations for GDP. The greenback may be given preference as a safe haven currency at any time, especially when US stock indexes aren’t willing to continue a rally. And that’s good for bulls! Retracements to $1.1655 and $1.158 will allow them to buy the euro cheaper.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/forecast-for-eurusd-will-dollar-correct/?uid=285861726&cid=79634

Dynamics of German business climate indexes

LiteFinance

Forecast for EUR/USD: Euro will put eggs in different baskets

Fundamental forecast for euro for today

EUR/USD may continue to rally on diversification of investment portfolios and gold/forex reserves

I’m pleased when my forecasts hit the bullseye, and even more so when they are fundamentally based. In June, I bet on the difference between Europe’s and the US’ epidemiological states, which suggested a faster economic recovery of the eurozone . The epic French-German fiscal stimulus project allowed me to suppose that EUR/USD would have new growth drivers: a flow of capital from the New World to the Old World and diversification of gold/forex reserves to the advantage of the euro. I’m pleased that my forecasts have worked.

The States’ inability to combat the pandemic put it at a disadvantage. According to Markit, the US business activity in July fell short of Bloomberg’s forecasts while Purchasing managers’ index of the eurozone was a feast to the eye. True, Europe’s GDP must have drawn down deeper than the US peer, but it’s likely to return to pre-crisis levels faster. Divergence in economic growths is an important factor in pricing in both Forex and stock markets.

Global investors haven’t needed to diversify their portfolios in the recent years. The bet on American high-tech stocks worked really well. However, the higher S&P 500 gets, the more overbought it looks - even more so because of the complicated epidemiological situation and growing risks of the US GDP’s W-shape recovery. As a result, one wants to put eggs in different baskets, and European stocks look attractive after the EU has accepted the French-German offer. According to Goldman Sachs, the EU stocks will have grown 13% in dollar terms and outperformed American peers within 12 months.

The idea of replacing the USD with the single European currency in the central banks’ reserves looks interesting too. A famous billionaire Ray Dalio thinks that besides a trade war, a technology war and a geopolitical war, there can be a capital war between the U.S. and China. People’s Bank of China’s active diversification of over $3 trillion gold/forex reserves won’t do any good for the greenback. The USA’s refusal to pay back Chinese-held treasury debt will only speed up the process.

No doubt, some pitfalls should be considered when it comes to EUR/USD’s bullish trend. Growth of new Covid cases in some areas of Spain and South-Eastern Europe suggests that a recovery won’t be as smooth as one would want to. A weaker dollar is a boon for American technological companies that earn most of their profits from abroad, which makes investment portfolio diversification less necessary. The White House continues to hope for a V-shape recovery. However, all those arguments have looked unconvincing so far while the euro’s bullish trend is obvious. Continue using retracements for opening long-term long positions with targets at $1.18 and $1.22.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/forecast-for-eurusd-euro-will-put-eggs-in-different-baskets/?uid=285861726&cid=79634

Evolution of European and American stocks

Fundamental forecast for euro for today

EUR/USD may continue to rally on diversification of investment portfolios and gold/forex reserves

I’m pleased when my forecasts hit the bullseye, and even more so when they are fundamentally based. In June, I bet on the difference between Europe’s and the US’ epidemiological states, which suggested a faster economic recovery of the eurozone . The epic French-German fiscal stimulus project allowed me to suppose that EUR/USD would have new growth drivers: a flow of capital from the New World to the Old World and diversification of gold/forex reserves to the advantage of the euro. I’m pleased that my forecasts have worked.

The States’ inability to combat the pandemic put it at a disadvantage. According to Markit, the US business activity in July fell short of Bloomberg’s forecasts while Purchasing managers’ index of the eurozone was a feast to the eye. True, Europe’s GDP must have drawn down deeper than the US peer, but it’s likely to return to pre-crisis levels faster. Divergence in economic growths is an important factor in pricing in both Forex and stock markets.

Global investors haven’t needed to diversify their portfolios in the recent years. The bet on American high-tech stocks worked really well. However, the higher S&P 500 gets, the more overbought it looks - even more so because of the complicated epidemiological situation and growing risks of the US GDP’s W-shape recovery. As a result, one wants to put eggs in different baskets, and European stocks look attractive after the EU has accepted the French-German offer. According to Goldman Sachs, the EU stocks will have grown 13% in dollar terms and outperformed American peers within 12 months.

The idea of replacing the USD with the single European currency in the central banks’ reserves looks interesting too. A famous billionaire Ray Dalio thinks that besides a trade war, a technology war and a geopolitical war, there can be a capital war between the U.S. and China. People’s Bank of China’s active diversification of over $3 trillion gold/forex reserves won’t do any good for the greenback. The USA’s refusal to pay back Chinese-held treasury debt will only speed up the process.

No doubt, some pitfalls should be considered when it comes to EUR/USD’s bullish trend. Growth of new Covid cases in some areas of Spain and South-Eastern Europe suggests that a recovery won’t be as smooth as one would want to. A weaker dollar is a boon for American technological companies that earn most of their profits from abroad, which makes investment portfolio diversification less necessary. The White House continues to hope for a V-shape recovery. However, all those arguments have looked unconvincing so far while the euro’s bullish trend is obvious. Continue using retracements for opening long-term long positions with targets at $1.18 and $1.22.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/forecast-for-eurusd-euro-will-put-eggs-in-different-baskets/?uid=285861726&cid=79634

Evolution of European and American stocks

LiteFinance

Euro brings happiness

Fundamental Euro forecast for today

The EUR/USD surge to 18-month highs made the world’s authorities happy

How little it takes to make people happy! First, lose something important, and then get it back to feel good. The EUR/USD has been back to the levels of early 2019, and so the high and mighty are satisfied. For example, Donald Trump is happy, as he has many times criticized the strong dollar. The EU governments are happy as the strong euro signals the euro-area unity. The IMF is happy as it says the too high dollar’s value hampers the global economic recovery. The euro bears may argue that the ECB won’t let the rally continue as it is not beneficial for the export-let euro area. I, however, do not agree. When the authorities try to support the domestic demand cheap import becomes a more important factor than the interests of foreign buyers.

The leading Wall Street banks share the same opinion. Just yesterday, I noted that the approval of the French-German stimulus plan will support European stock in the competition with the US peers. It will increase the capital inflow to the euro-area markets, and so, the proportion of the euro in the FX reserves of the central banks will grow, just like its value. For example, Credit Suisse stresses that the percentage of the dollar in the global currency reserves can drop to the levels recorded in the early 1990s. The bank sees the EUR/USD at 1.18 and higher.

According to Mizuho, the current fair value of the euro is $1.22 and its rate may rise to $1.3 within 12 months due to large-scale purchases of high-yield bonds of the euro-area peripheral countries. The risks of the defaults have lowered after the EU governments agreed on the €1.8-trillion fiscal stimulus. AG Bisset Associates, which has been bearish on the US dollar for a long time, believes that the EUR/USD will be 30% in the next 16 months.

I believe the market continues working out the idea of the divergence in economic growth. The EU approval of the fiscal stimulus should speed up the euro-area GDP recovery trend. The US growth, however, is set back by disputes between the members of Congress and the White House. Democrats are willing to do even more than they were before (the House of Representatives approved a $3.5 trillion stimulus package). The Republicans, however, reject this proposal suggesting a package of $1 trillion, including payroll tax cuts to encourage people to return to jobs.

According to Bloomberg’s leading indicators, the gap in the recovery paces of the euro area and the US widened over the past week. The lack of agreement on the US new fiscal stimulus plan will widen it even more.

So, the bet on the divergence in the epidemiological situation and economic growth in the euro area and the US is working and should continue working. The EUR/USD upside target is at 1.17 by the year’s end. I recommend buying the euro on the corrections down.

Dynamics of the US dollar proportion in the global FX reserves

Fundamental Euro forecast for today

The EUR/USD surge to 18-month highs made the world’s authorities happy

How little it takes to make people happy! First, lose something important, and then get it back to feel good. The EUR/USD has been back to the levels of early 2019, and so the high and mighty are satisfied. For example, Donald Trump is happy, as he has many times criticized the strong dollar. The EU governments are happy as the strong euro signals the euro-area unity. The IMF is happy as it says the too high dollar’s value hampers the global economic recovery. The euro bears may argue that the ECB won’t let the rally continue as it is not beneficial for the export-let euro area. I, however, do not agree. When the authorities try to support the domestic demand cheap import becomes a more important factor than the interests of foreign buyers.

The leading Wall Street banks share the same opinion. Just yesterday, I noted that the approval of the French-German stimulus plan will support European stock in the competition with the US peers. It will increase the capital inflow to the euro-area markets, and so, the proportion of the euro in the FX reserves of the central banks will grow, just like its value. For example, Credit Suisse stresses that the percentage of the dollar in the global currency reserves can drop to the levels recorded in the early 1990s. The bank sees the EUR/USD at 1.18 and higher.

According to Mizuho, the current fair value of the euro is $1.22 and its rate may rise to $1.3 within 12 months due to large-scale purchases of high-yield bonds of the euro-area peripheral countries. The risks of the defaults have lowered after the EU governments agreed on the €1.8-trillion fiscal stimulus. AG Bisset Associates, which has been bearish on the US dollar for a long time, believes that the EUR/USD will be 30% in the next 16 months.

I believe the market continues working out the idea of the divergence in economic growth. The EU approval of the fiscal stimulus should speed up the euro-area GDP recovery trend. The US growth, however, is set back by disputes between the members of Congress and the White House. Democrats are willing to do even more than they were before (the House of Representatives approved a $3.5 trillion stimulus package). The Republicans, however, reject this proposal suggesting a package of $1 trillion, including payroll tax cuts to encourage people to return to jobs.

According to Bloomberg’s leading indicators, the gap in the recovery paces of the euro area and the US widened over the past week. The lack of agreement on the US new fiscal stimulus plan will widen it even more.

So, the bet on the divergence in the epidemiological situation and economic growth in the euro area and the US is working and should continue working. The EUR/USD upside target is at 1.17 by the year’s end. I recommend buying the euro on the corrections down.

Dynamics of the US dollar proportion in the global FX reserves

LiteFinance

XAU/USD forecast: Four nuts for gold

Fundamental gold price forecast for today

Gold can still break through its all-time highs

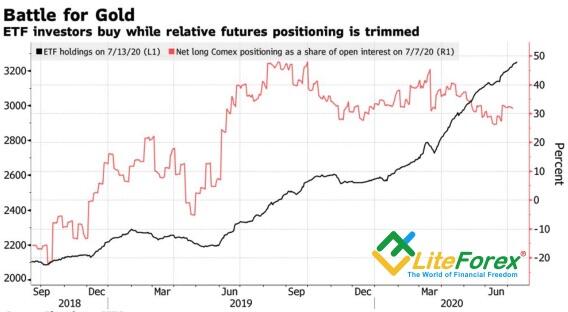

The huge monetary stimulus provided by the world’s leading central banks, and the weakness of the world’s major currencies have driven the gold price to the levels it was last seen in 2011. Will the growth of the inflation, or, maybe, stagflation, help gold to break through the all-time highs. When the XAU/USD bears are tired of fighting and are giving in, it doesn’t look like something unreal. According to Citigroup, the record high will be updated during 6-9 months. Besides, there is a 30% chance that the gold price will go up higher than $2000 per ounce in 3-5 months.

Ultra-low monetary policies of the central banks, the drop in the bonds real yields, a big flow of capitals into the gold ETFs, and the redistribution of assets in the investors’ portfolios allow the XAU/USD bulls to go ahead. Gold has already hot mew all-time highs against all G10 currencies except for the US dollar. It seems that the gold will soon break through the local high in trading versus the greenback. In addition to the high demand for ETF products, there is a rise in the demand for the inflation-protected bonds in July, as well as the drop in the USD index. All three factors are positive for gold.

The ETF gold holdings have increased by 450 tons, or $27 billion, since mid-July. It has become one of the major benefits of gold. The indicator has reached a record high of more than 3200 tons. During six months, investors bought the gold ETF products more than all central banks together in 2018-2019.

Earlier, bulls the XAU/USD bulls bet on the weakness of the world’s major currencies resulted from the huge monetary stimulus. Now, they are focused on inflation. Although the US PCE is far from the Fed’s target of 2%, 30-year Treasury inflation-protected securities are close to an all-time low, the yields on the 5-year and 10-year TIPS are close to the lowest levels since 2013 and 2012. In the week through July 8, investors invested about $5 billion in the related ETFs, having turned the trend of the capital outflow from the exchange-traded funds. The market expects the growth of the inflation rate, it is not confused by the current levels of the PCE and CPI. BofA Merrill Lynch says the US economy may face stagflation when the GDP is not recovering but the prices are growing.

In addition to the weakness of the world major currencies, including the US dollar, low Treasury real yields, and the expectations for the growth in consumer prices, another important growth driver for the XAU/USD is the redistribution of the investors’ assets. Stocks look too expensive according to the P/E ratio. Therefore, even strong US domestic data do not encourage the S&P 500 bulls. Bonds, unlike the stock indexes trading in the green, are trading in the red area and also look overbought. Gold seems much more promising under the current conditions. So, one could think of increasing the share of gold in the investment portfolio. If the price breaks through the resistance zone of $1820-$1825, it makes sense to enter gold longs and take part in the LiteForex contest devoted to the LiteForex 15th anniversary with excellent prizes.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/xauusd-forecast-four-nuts-for-gold/?uid=285861726&cid=79634

Dynamics of gold and ETF holdings

Fundamental gold price forecast for today

Gold can still break through its all-time highs

The huge monetary stimulus provided by the world’s leading central banks, and the weakness of the world’s major currencies have driven the gold price to the levels it was last seen in 2011. Will the growth of the inflation, or, maybe, stagflation, help gold to break through the all-time highs. When the XAU/USD bears are tired of fighting and are giving in, it doesn’t look like something unreal. According to Citigroup, the record high will be updated during 6-9 months. Besides, there is a 30% chance that the gold price will go up higher than $2000 per ounce in 3-5 months.

Ultra-low monetary policies of the central banks, the drop in the bonds real yields, a big flow of capitals into the gold ETFs, and the redistribution of assets in the investors’ portfolios allow the XAU/USD bulls to go ahead. Gold has already hot mew all-time highs against all G10 currencies except for the US dollar. It seems that the gold will soon break through the local high in trading versus the greenback. In addition to the high demand for ETF products, there is a rise in the demand for the inflation-protected bonds in July, as well as the drop in the USD index. All three factors are positive for gold.

The ETF gold holdings have increased by 450 tons, or $27 billion, since mid-July. It has become one of the major benefits of gold. The indicator has reached a record high of more than 3200 tons. During six months, investors bought the gold ETF products more than all central banks together in 2018-2019.

Earlier, bulls the XAU/USD bulls bet on the weakness of the world’s major currencies resulted from the huge monetary stimulus. Now, they are focused on inflation. Although the US PCE is far from the Fed’s target of 2%, 30-year Treasury inflation-protected securities are close to an all-time low, the yields on the 5-year and 10-year TIPS are close to the lowest levels since 2013 and 2012. In the week through July 8, investors invested about $5 billion in the related ETFs, having turned the trend of the capital outflow from the exchange-traded funds. The market expects the growth of the inflation rate, it is not confused by the current levels of the PCE and CPI. BofA Merrill Lynch says the US economy may face stagflation when the GDP is not recovering but the prices are growing.

In addition to the weakness of the world major currencies, including the US dollar, low Treasury real yields, and the expectations for the growth in consumer prices, another important growth driver for the XAU/USD is the redistribution of the investors’ assets. Stocks look too expensive according to the P/E ratio. Therefore, even strong US domestic data do not encourage the S&P 500 bulls. Bonds, unlike the stock indexes trading in the green, are trading in the red area and also look overbought. Gold seems much more promising under the current conditions. So, one could think of increasing the share of gold in the investment portfolio. If the price breaks through the resistance zone of $1820-$1825, it makes sense to enter gold longs and take part in the LiteForex contest devoted to the LiteForex 15th anniversary with excellent prizes.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/xauusd-forecast-four-nuts-for-gold/?uid=285861726&cid=79634

Dynamics of gold and ETF holdings

LiteFinance

EUR/USD forecast: Dollar is rising

Fundamental US dollar forecast for today

How deep will the EUR/USD fall?

The less you know, the better. The European Central Bank President Christine Lagarde hasn’t mentioned the disputes among the members of the Governing Council. She said the central bank currently expects to spend the full amount of its pandemic bond-buying program unless there isn’t a significant surprise, but the markets suggest something different. According to Bloomberg’s sources familiar with the matter, policymakers didn’t come to an agreement on whether the full program was likely to be used. Some Executive Board members argue that the improving economy may mean bond-buying could end before reaching the current cap. If it was officially announced, it would cancel the ECB’s baseline projection is for an 8.7% contraction in the euro-area economy this year. However, the ECB is not yet prepared to send such a message.

Lagarde stresses that the euro-area recovery remains partial and uneven, with risks still tilted to the downside. She says the ECB’s monetary stimulus will add 1.3% to the GDP and 0.8% to the inflation rate by 2022. The Governing Council is again divided into hawks and doves. The rich North is opposed to the poor South. So it is not surprising that some policymakers suggest the end of the bond-buying program, and other Executive Board members offer to expand it. According to the forecasts of the European Commission, the GDPs of Italy, France, and Spain will be down by approximately 11.5%, and Germany’s economy will lose half as much.

The lack of agreement among the ECB governors could eliminate such a benefit of the euro as the euro-area unity. It is extremely dangerous ahead of the EU summit. If the bloc doesn’t approve of the French-German 750 billion-euro recovery fund will set a date for an extraordinary meeting to continue discussions on this topic, the EUR/USD bulls will be set back.

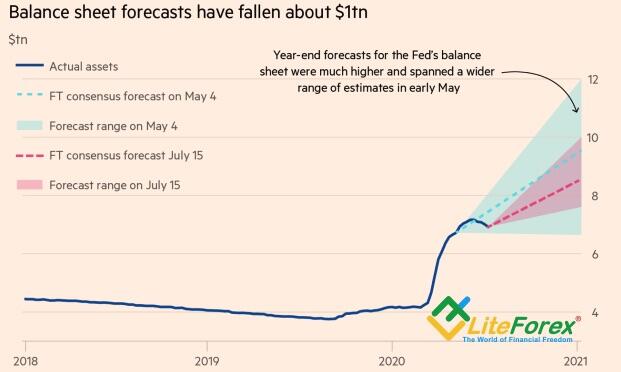

In the US, however, the retail sales data and homebuilders’ outlook are is back at pre-pandemic levels. Furthermore, the Fed’s balance sheet fell by $210 billion since June 10, being back below $7 trillion. If the US economy performs better than it could be expected considering the growth in the daily COVID-19 cases to more than 70,000, then why should the Fed continue taking active measures? According to the forecast of Wall Street experts, the Fed’s balance sheet should rise to $8.5 trillion by the end of 2020, instead of $9.5 trillion expected earlier.

In addition to the improved domestic data in the US, investors consider such a bullish driver for the greenback as the escalation of the US-China trade war. The White House is not happy that the Chinese GDP grew by 3.2% in the second quarter, while the US GDP is likely to be down by 10% in the same period. A faster economic recovery will allow China’s exporters to boost their share in the market, and so, make one more step forward to the world’s leadership.

In my opinion, the down moves of the EUR/USD are nothing more than just a correction. An increase in the number of coronavirus cases will suggest worse economic data of the US for June, which, amid the main investment idea based on the divergence in the economic growth, should encourage the EUR/USD bulls to go ahead. If the EU governments agree on the fiscal stimulus package, the euro buyers will feel more confident. In the meanwhile, the major currency pair meets my expectations and consolidates in the range of 1.11-1.14. The euro is more likely to rise to $1.16 and higher than to fall to $1.11.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/eurusd-forecast-dollar-is-rising/?uid=285861726&cid=79634

Forecasts for Fed balance sheet

Fundamental US dollar forecast for today

How deep will the EUR/USD fall?

The less you know, the better. The European Central Bank President Christine Lagarde hasn’t mentioned the disputes among the members of the Governing Council. She said the central bank currently expects to spend the full amount of its pandemic bond-buying program unless there isn’t a significant surprise, but the markets suggest something different. According to Bloomberg’s sources familiar with the matter, policymakers didn’t come to an agreement on whether the full program was likely to be used. Some Executive Board members argue that the improving economy may mean bond-buying could end before reaching the current cap. If it was officially announced, it would cancel the ECB’s baseline projection is for an 8.7% contraction in the euro-area economy this year. However, the ECB is not yet prepared to send such a message.

Lagarde stresses that the euro-area recovery remains partial and uneven, with risks still tilted to the downside. She says the ECB’s monetary stimulus will add 1.3% to the GDP and 0.8% to the inflation rate by 2022. The Governing Council is again divided into hawks and doves. The rich North is opposed to the poor South. So it is not surprising that some policymakers suggest the end of the bond-buying program, and other Executive Board members offer to expand it. According to the forecasts of the European Commission, the GDPs of Italy, France, and Spain will be down by approximately 11.5%, and Germany’s economy will lose half as much.

The lack of agreement among the ECB governors could eliminate such a benefit of the euro as the euro-area unity. It is extremely dangerous ahead of the EU summit. If the bloc doesn’t approve of the French-German 750 billion-euro recovery fund will set a date for an extraordinary meeting to continue discussions on this topic, the EUR/USD bulls will be set back.

In the US, however, the retail sales data and homebuilders’ outlook are is back at pre-pandemic levels. Furthermore, the Fed’s balance sheet fell by $210 billion since June 10, being back below $7 trillion. If the US economy performs better than it could be expected considering the growth in the daily COVID-19 cases to more than 70,000, then why should the Fed continue taking active measures? According to the forecast of Wall Street experts, the Fed’s balance sheet should rise to $8.5 trillion by the end of 2020, instead of $9.5 trillion expected earlier.

In addition to the improved domestic data in the US, investors consider such a bullish driver for the greenback as the escalation of the US-China trade war. The White House is not happy that the Chinese GDP grew by 3.2% in the second quarter, while the US GDP is likely to be down by 10% in the same period. A faster economic recovery will allow China’s exporters to boost their share in the market, and so, make one more step forward to the world’s leadership.

In my opinion, the down moves of the EUR/USD are nothing more than just a correction. An increase in the number of coronavirus cases will suggest worse economic data of the US for June, which, amid the main investment idea based on the divergence in the economic growth, should encourage the EUR/USD bulls to go ahead. If the EU governments agree on the fiscal stimulus package, the euro buyers will feel more confident. In the meanwhile, the major currency pair meets my expectations and consolidates in the range of 1.11-1.14. The euro is more likely to rise to $1.16 and higher than to fall to $1.11.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/eurusd-forecast-dollar-is-rising/?uid=285861726&cid=79634

Forecasts for Fed balance sheet

LiteFinance

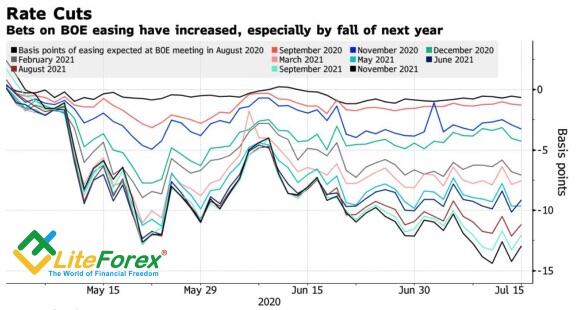

GBP/USD forecast: Pound caught the wind of change

Fundamental Pound forecast for today

Global risk appetite is no longer the main driver of the GBP/USD

For a long time, amid its high volatility, the GBP depended on the changes in the global risk appetite, behaving like an emerging market’s currency. Nonetheless, investors have now changed their point of view, as financial markets are stabilizing, and it is clear that the peak of the global economic recession has been over. Now, the major forex driver is the speed of the recovery trend in a particular country, which is greatly determined by the epidemiological situation. And the epidemiological situation is difficult in the UK.

The UK is likely to be among the European countries worst affected by COVID-19. About 300,000 coronavirus cases and 45,000 deaths, a late strict lockdown made the OECD forecast the UK GDP drop by 11.5% in 2020, which is the worst downturn for the advanced economies. Some improvements in the data on the UK retail sales, PMI, and inflation allowed the BoE Chief Economist Andy Haldane to suggest that the UK GDP should rebound sooner than it was earlier expected. It encouraged the GBP/USD bulls to draw the price to the top of figure 26. However, the success of the sterling buyers has not lasted for long.

The UK GDP report for May showed that the economy expanded by only 1.8%, instead of 5.5% expected by Reuters experts. It prompts that it will take a longer time for the UK GDP rate to return to the trend. The derivatives market expects the BoE will cut the interest rate below zero by March 2022. Economists polled by Bloomberg forecast the QE expansion by £50 billion through the end of 2020. The MPC Member Silvana Tenreyro says she is willing to vote for the further measures to support the UK economic recovery.

The head of the Bank of England Andrew Bailey supports this idea, saying that the central bank will do its best to support the UK GDP growth, and the interest rates should be kept low for a long time.

The pound is weakened because of several fundamental factors. The MPC members sound dovish, investors are disappointed as the UK economy fails to rebound quickly and shift their focus from the risk appetite to the divergence in the GDP growth. Furthermore, the Brexit issue has not been solved, and the breakup in trade relations with the EU will worsen the UK economic state that is already weak. The UK growth, according to Bloomberg is recovering, slower than that of other European countries. It suggests reasons to buy the EUR/GBP with targets at 0.925 and 0.94.

I expect the GBP/USD to consolidate in the trading range of 1.24-1.27. The pair should be responsive to the economic reports in the UK and the USA, as well as the news about Brexit. The epidemiological situation in the USA is worse than in the euro area. Besides, the US dollar long-term outlook is bearish. So, the GBP/USD uptrend could yet recover. Nonetheless, the sterling must have a fresh driver to go up form the trading range.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/gbpusd-forecast-pound-caught-the-wind-of-change/?uid=285861726&cid=79634

Dynamics of the probability of the BoE interest rate changes

Fundamental Pound forecast for today

Global risk appetite is no longer the main driver of the GBP/USD

For a long time, amid its high volatility, the GBP depended on the changes in the global risk appetite, behaving like an emerging market’s currency. Nonetheless, investors have now changed their point of view, as financial markets are stabilizing, and it is clear that the peak of the global economic recession has been over. Now, the major forex driver is the speed of the recovery trend in a particular country, which is greatly determined by the epidemiological situation. And the epidemiological situation is difficult in the UK.

The UK is likely to be among the European countries worst affected by COVID-19. About 300,000 coronavirus cases and 45,000 deaths, a late strict lockdown made the OECD forecast the UK GDP drop by 11.5% in 2020, which is the worst downturn for the advanced economies. Some improvements in the data on the UK retail sales, PMI, and inflation allowed the BoE Chief Economist Andy Haldane to suggest that the UK GDP should rebound sooner than it was earlier expected. It encouraged the GBP/USD bulls to draw the price to the top of figure 26. However, the success of the sterling buyers has not lasted for long.

The UK GDP report for May showed that the economy expanded by only 1.8%, instead of 5.5% expected by Reuters experts. It prompts that it will take a longer time for the UK GDP rate to return to the trend. The derivatives market expects the BoE will cut the interest rate below zero by March 2022. Economists polled by Bloomberg forecast the QE expansion by £50 billion through the end of 2020. The MPC Member Silvana Tenreyro says she is willing to vote for the further measures to support the UK economic recovery.

The head of the Bank of England Andrew Bailey supports this idea, saying that the central bank will do its best to support the UK GDP growth, and the interest rates should be kept low for a long time.

The pound is weakened because of several fundamental factors. The MPC members sound dovish, investors are disappointed as the UK economy fails to rebound quickly and shift their focus from the risk appetite to the divergence in the GDP growth. Furthermore, the Brexit issue has not been solved, and the breakup in trade relations with the EU will worsen the UK economic state that is already weak. The UK growth, according to Bloomberg is recovering, slower than that of other European countries. It suggests reasons to buy the EUR/GBP with targets at 0.925 and 0.94.

I expect the GBP/USD to consolidate in the trading range of 1.24-1.27. The pair should be responsive to the economic reports in the UK and the USA, as well as the news about Brexit. The epidemiological situation in the USA is worse than in the euro area. Besides, the US dollar long-term outlook is bearish. So, the GBP/USD uptrend could yet recover. Nonetheless, the sterling must have a fresh driver to go up form the trading range.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/gbpusd-forecast-pound-caught-the-wind-of-change/?uid=285861726&cid=79634

Dynamics of the probability of the BoE interest rate changes

LiteFinance

EUR/USD forecast: Euro wants to go up

Fundamental Euro forecast for today

EUR/USD bulls pin their hopes on China’s GDP report, the ECB meeting, and the EU summit

When the market is full of optimists, it ignores bad news and lively reacts to the good news. It doesn’t matter that during the test of the COVID-19 vaccine, side effects were observed; what matters is that all the people participating in the experiment produced antibodies. It doesn’t matter that corporate reporting by JP Morgan and Citigroup for the second quarter was gloomy, as the actual data exceeded the forecasts. It doesn’t matter that some FOMC members suggest strong uncertainty around the US economic recovery when some US central bankers still believe in the V-shaped recovery trend. When the glass is half-full, the S&P 500 and the EUR/USD can well continue the rally.

St. Louis Fed President James Bullard says the US economy adapts to the coronavirus, and there is still hope for a quick rebound. A strong jobs report for May and June supports the idea that the US GDP reached its bottom in April, and the forecast for the second quarter has been too grim. Federal Reserve Governor Lael Brainard says one of the main reasons for the improvement in the US employment data is the fiscal stimulus, some of whose programs are coming to an end. Even if the rate of the spread of COVID-19 slows down, the economy “is likely to face headwinds,” she warns, which may result in a double-dip recession.

Brainard’s pessimistic tone hasn’t caused much stress in the financial markets. The liquidity volumes poured by the Fed and other world’s central banks are too big, so the stock indexes won’t stop growing.

The stimulus sizes are so huge that the S&P 500 just can’t fall too deep. Besides, the euro has its own growth drivers, so the EUR/USD is steadily growing. The price has tested the resistance at 1.14, and the euro bulls are expecting more good news provided by the Chinese GDP report, the ECB meeting and the EU summit to drive the price higher.

The markets are going back to the norm and start to feature a correct response to the news. They are rising when the actual data exceed the forecasts and vice versa. With this regard, the pessimistic forecasts suggesting a 45% drop in corporate profits in the second quarter are more likely to support the S&P 500 than to send it down, which has been proven by the reaction of the stock index to the release of the reports by JP Morgan and Citigroup. The S&P 500 should also be supported if the Chinese domestic data are positive. The forecasts for China’s GDP, industrial production, retail sales, and investments are not very strong. It is expected that China’s economy hasn’t yet returned to the pre-crisis levels. What if it isn’t so?

The ECB doesn’t consider further interest rate cuts. Furthermore, it is willing to gradually reduce the volumes of the liquidity poured in the markets, following the example of other central banks. It will be a positive factor for the euro. Another growth driver will appear if the EU governments adopt the French-German fiscal stimulus plan at the EU summit. The EUR/USD has been consolidating in the range of 1.11-1.14 for too long, it is time to go up. If the price retests the resistance at 1.14, the bulls will go ahead. If, of course, everything goes on as expected.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/eurusd-forecast-euro-wants-to-go-up/?uid=285861726&cid=79634

Dynamics of money supply and MSCI World Total Return

Fundamental Euro forecast for today

EUR/USD bulls pin their hopes on China’s GDP report, the ECB meeting, and the EU summit

When the market is full of optimists, it ignores bad news and lively reacts to the good news. It doesn’t matter that during the test of the COVID-19 vaccine, side effects were observed; what matters is that all the people participating in the experiment produced antibodies. It doesn’t matter that corporate reporting by JP Morgan and Citigroup for the second quarter was gloomy, as the actual data exceeded the forecasts. It doesn’t matter that some FOMC members suggest strong uncertainty around the US economic recovery when some US central bankers still believe in the V-shaped recovery trend. When the glass is half-full, the S&P 500 and the EUR/USD can well continue the rally.

St. Louis Fed President James Bullard says the US economy adapts to the coronavirus, and there is still hope for a quick rebound. A strong jobs report for May and June supports the idea that the US GDP reached its bottom in April, and the forecast for the second quarter has been too grim. Federal Reserve Governor Lael Brainard says one of the main reasons for the improvement in the US employment data is the fiscal stimulus, some of whose programs are coming to an end. Even if the rate of the spread of COVID-19 slows down, the economy “is likely to face headwinds,” she warns, which may result in a double-dip recession.

Brainard’s pessimistic tone hasn’t caused much stress in the financial markets. The liquidity volumes poured by the Fed and other world’s central banks are too big, so the stock indexes won’t stop growing.

The stimulus sizes are so huge that the S&P 500 just can’t fall too deep. Besides, the euro has its own growth drivers, so the EUR/USD is steadily growing. The price has tested the resistance at 1.14, and the euro bulls are expecting more good news provided by the Chinese GDP report, the ECB meeting and the EU summit to drive the price higher.

The markets are going back to the norm and start to feature a correct response to the news. They are rising when the actual data exceed the forecasts and vice versa. With this regard, the pessimistic forecasts suggesting a 45% drop in corporate profits in the second quarter are more likely to support the S&P 500 than to send it down, which has been proven by the reaction of the stock index to the release of the reports by JP Morgan and Citigroup. The S&P 500 should also be supported if the Chinese domestic data are positive. The forecasts for China’s GDP, industrial production, retail sales, and investments are not very strong. It is expected that China’s economy hasn’t yet returned to the pre-crisis levels. What if it isn’t so?

The ECB doesn’t consider further interest rate cuts. Furthermore, it is willing to gradually reduce the volumes of the liquidity poured in the markets, following the example of other central banks. It will be a positive factor for the euro. Another growth driver will appear if the EU governments adopt the French-German fiscal stimulus plan at the EU summit. The EUR/USD has been consolidating in the range of 1.11-1.14 for too long, it is time to go up. If the price retests the resistance at 1.14, the bulls will go ahead. If, of course, everything goes on as expected.

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/eurusd-forecast-euro-wants-to-go-up/?uid=285861726&cid=79634

Dynamics of money supply and MSCI World Total Return

LiteFinance

EUR/USD forecast: Dollar lost the fear

Fundamental US dollar forecast for today

What was the benefit of the USD index yesterday can become its flaw tomorrow

What is good for the entire world is bad for the US dollar. The pandemic is still the major growth driver of the greenback. The US stock indexes are weighed on by the difficult epidemiological situation in the U.S. and the news that California cancels plans to open economy. It supports the demand for safe havens and so, the dollar remains strong. However, based on the assumption that COVID-19 will be defeated, the long-term prospects for the US dollar look gloomy.

During the turmoil, investors buy out safe havens. However, once the markets calm down, the safe havens lose their appeal. The balance of the Fed's foreign exchange swaps with other central banks, designed to provide them with the dollar liquidity, dropped to $153 billion from $449 billion in late May. Global stock indexes have stabilized, nobody needs the greenback any more.

Having cut the interest rates to 0%-0.25%, the Fed returned the US dollar the status of the main safe haven, which strengthened the greenback when investors were guided by fear. However, when the global GDP started to recover from the recession, yesterday’s benefit turns into a flaw. The dollar has lost such a growth driver as high government bond yields, which sets back the capital inflow into the US. Foreign investors become more interested in China’s assets than in US securities. Foreign investors bought $619 billion of Chinese government bonds in the second quarter, it is the highest amount on record.

And the US desperately needs money! The U.S. budget deficit reached $3 trillion in the 12 months through June. The Congressional Budget Office expects it will be $ 3.7 billion this fiscal year. Besides, another round of emergency spending, suggested by the White House, will increase the US budget deficit, as well as the issuance volumes. How can they raise resources if foreign investors are increasingly buying bonds issued by the Chinese government?

In addition to the drop in the demand for safe havens and dollar liquidity, low Treasury yields, and problems with raising capital, the greenback is weighed on by growing Joe Biden's approval ratings and concerns about a decline in the US domestic data. It is expected that the Democratic president will not attack Beijing so much and write provocative tweets as Donald Trump does. Remember, the US-China trade war was one of the major dollar’s growth drivers in 2018-2019.

Therefore, there are quite many long-term negative factors affecting the US dollar, that is why its one-year risk reversals are down.

In the short run, the greenback is supported by the pandemic, and the euro is weighed on by the uncertainty around the outcomes of the ECB meeting and the EU summit, as well as the upcoming report on the Chinese GDP. The current EUR/USD consolidation in the narrow range of 1.125-1.14 is quite natural. Investors do not want to take important decisions ahead of the release of the important information in the week through July 17. We shall also wait and see.

Dynamics of the balance of the Fed's foreign exchange swaps

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/eurusd-forecast-dollar-lost-the-fear/?uid=285861726&cid=79634

Fundamental US dollar forecast for today

What was the benefit of the USD index yesterday can become its flaw tomorrow

What is good for the entire world is bad for the US dollar. The pandemic is still the major growth driver of the greenback. The US stock indexes are weighed on by the difficult epidemiological situation in the U.S. and the news that California cancels plans to open economy. It supports the demand for safe havens and so, the dollar remains strong. However, based on the assumption that COVID-19 will be defeated, the long-term prospects for the US dollar look gloomy.

During the turmoil, investors buy out safe havens. However, once the markets calm down, the safe havens lose their appeal. The balance of the Fed's foreign exchange swaps with other central banks, designed to provide them with the dollar liquidity, dropped to $153 billion from $449 billion in late May. Global stock indexes have stabilized, nobody needs the greenback any more.

Having cut the interest rates to 0%-0.25%, the Fed returned the US dollar the status of the main safe haven, which strengthened the greenback when investors were guided by fear. However, when the global GDP started to recover from the recession, yesterday’s benefit turns into a flaw. The dollar has lost such a growth driver as high government bond yields, which sets back the capital inflow into the US. Foreign investors become more interested in China’s assets than in US securities. Foreign investors bought $619 billion of Chinese government bonds in the second quarter, it is the highest amount on record.

And the US desperately needs money! The U.S. budget deficit reached $3 trillion in the 12 months through June. The Congressional Budget Office expects it will be $ 3.7 billion this fiscal year. Besides, another round of emergency spending, suggested by the White House, will increase the US budget deficit, as well as the issuance volumes. How can they raise resources if foreign investors are increasingly buying bonds issued by the Chinese government?

In addition to the drop in the demand for safe havens and dollar liquidity, low Treasury yields, and problems with raising capital, the greenback is weighed on by growing Joe Biden's approval ratings and concerns about a decline in the US domestic data. It is expected that the Democratic president will not attack Beijing so much and write provocative tweets as Donald Trump does. Remember, the US-China trade war was one of the major dollar’s growth drivers in 2018-2019.

Therefore, there are quite many long-term negative factors affecting the US dollar, that is why its one-year risk reversals are down.

In the short run, the greenback is supported by the pandemic, and the euro is weighed on by the uncertainty around the outcomes of the ECB meeting and the EU summit, as well as the upcoming report on the Chinese GDP. The current EUR/USD consolidation in the narrow range of 1.125-1.14 is quite natural. Investors do not want to take important decisions ahead of the release of the important information in the week through July 17. We shall also wait and see.

Dynamics of the balance of the Fed's foreign exchange swaps

For more information follow the link to the website of the LiteForex

https://www.liteforex.com/blog/analysts-opinions/eurusd-forecast-dollar-lost-the-fear/?uid=285861726&cid=79634

LiteFinance

EUR/USD forecast: Dollar is grasping at straws

Fundamental US dollar forecast for today

The growth in the number of COVID-19 cases in the USA sets back the EUR/USD uptrend

The EU governments used to be accused of inefficient management, but the pandemic changed everything. The success of European medical services, quick actions to provide monetary and fiscal stimulus, and Germany’s willingness to take responsibility for poorer euro-area states have encouraged the EUR/USD bulls to go ahead. The euro risk reversals are growing as the epidemiological situation in the USA, unlike that in the euro area, is deteriorating, and the local rises of the US dollar are used to sell the greenback off. According to Bloomberg’s option probability calculator, based on the options market pricing, the EUR/USD is more likely to trade above 1.15 in a week’s time than to drop below 1.12.

The median gauge of the Wall Street 11 biggest banks also suggest the eurodollar should be at 1.15 by the end of 2020. BofA Merrill Lynch suggests the most bearish forecast, saying the EUR/USD should be down to 1.05. They say the Fed will hardly boost its balance sheet significantly, while the ECB will continue easing its monetary policy. According to 64% of Bloomberg experts, Christine Lagarde and her colleagues will boost the ECB’s QE program by €400-€600 billion by the end of the year. However, I believe it is not very wise to bet solely on the divergence in views from policymakers in the U.S. and EU. Markets are likely to be more influenced by the trade wars or the COVID-19 news, than the decisions on monetary policies.

Investors should take into account different factors and build their own trading strategies based on the strongest drivers. In 2018-2019, the determining forex pricing factor was the US-China trade war, in 2020, it is the coronavirus pandemic and economic lockdowns. With this regard, a better epidemiological situation in Europe suggests a quicker rebound of the euro-area economy, which should support the growing demand for European assets. The liquidity is flowing out of the US, and so, the greenback is weakening.

One shouldn’t be confused by the growth of Citigroup's US Economic Surprise Index. The US positive economic data under current conditions are like fast food. It looks appealing but it is bad for your health.

The euro is also supported by the yuan that is growing in value now. The matter is not only in the market important for the Eurozone. When investors are willing to buy anything but for the US assets, the greenback's rivals are growing in price.

The drop of the USD/CNY has resulted from both a quick recovery of the Chinese economy and the weakness of the world’s major currencies weighed on by the huge fiscal stimulus. The yuan positively responds to the growth of the approval ratings of democratic presidential candidate Joe Biden, whose policy is likely to be less aggressive than that of Donald Trump.

Of course, one should not fully give up on the US dollar as a safe haven amid the growth in the number of coronavirus cases in the USA. However, the middle-term and long-term outlook of the greenback is bearish. Therefore, one should use the drop of the EUR/USD to the bottom of the trading range of 1.11-1.14, I suggested earlier, to add to the long positions.

Dynamics the ratio of U.S. versus Germany COVID-19 cases and the euro risk reversals

Fundamental US dollar forecast for today

The growth in the number of COVID-19 cases in the USA sets back the EUR/USD uptrend

The EU governments used to be accused of inefficient management, but the pandemic changed everything. The success of European medical services, quick actions to provide monetary and fiscal stimulus, and Germany’s willingness to take responsibility for poorer euro-area states have encouraged the EUR/USD bulls to go ahead. The euro risk reversals are growing as the epidemiological situation in the USA, unlike that in the euro area, is deteriorating, and the local rises of the US dollar are used to sell the greenback off. According to Bloomberg’s option probability calculator, based on the options market pricing, the EUR/USD is more likely to trade above 1.15 in a week’s time than to drop below 1.12.

The median gauge of the Wall Street 11 biggest banks also suggest the eurodollar should be at 1.15 by the end of 2020. BofA Merrill Lynch suggests the most bearish forecast, saying the EUR/USD should be down to 1.05. They say the Fed will hardly boost its balance sheet significantly, while the ECB will continue easing its monetary policy. According to 64% of Bloomberg experts, Christine Lagarde and her colleagues will boost the ECB’s QE program by €400-€600 billion by the end of the year. However, I believe it is not very wise to bet solely on the divergence in views from policymakers in the U.S. and EU. Markets are likely to be more influenced by the trade wars or the COVID-19 news, than the decisions on monetary policies.

Investors should take into account different factors and build their own trading strategies based on the strongest drivers. In 2018-2019, the determining forex pricing factor was the US-China trade war, in 2020, it is the coronavirus pandemic and economic lockdowns. With this regard, a better epidemiological situation in Europe suggests a quicker rebound of the euro-area economy, which should support the growing demand for European assets. The liquidity is flowing out of the US, and so, the greenback is weakening.

One shouldn’t be confused by the growth of Citigroup's US Economic Surprise Index. The US positive economic data under current conditions are like fast food. It looks appealing but it is bad for your health.

The euro is also supported by the yuan that is growing in value now. The matter is not only in the market important for the Eurozone. When investors are willing to buy anything but for the US assets, the greenback's rivals are growing in price.

The drop of the USD/CNY has resulted from both a quick recovery of the Chinese economy and the weakness of the world’s major currencies weighed on by the huge fiscal stimulus. The yuan positively responds to the growth of the approval ratings of democratic presidential candidate Joe Biden, whose policy is likely to be less aggressive than that of Donald Trump.

Of course, one should not fully give up on the US dollar as a safe haven amid the growth in the number of coronavirus cases in the USA. However, the middle-term and long-term outlook of the greenback is bearish. Therefore, one should use the drop of the EUR/USD to the bottom of the trading range of 1.11-1.14, I suggested earlier, to add to the long positions.

Dynamics the ratio of U.S. versus Germany COVID-19 cases and the euro risk reversals

LiteFinance

EUR/USD forecast: Euro has caught a tail-wind

Fundamental Euro forecast for today

The EUR/USD bulls are supported by good news from Asia and the stabilization of European financial markets.

For a long time, the entire financial world has been following the US, depending on the US stock indexes. However, the economic situation in the US is like “hope for the better but prepare for the worse”, and other countries are now coming in the game. The continuous growth of the Chinese stocks over the last seven days and the yuan’s rise to its four-month highs indicate the strength of China’s economy, which might become the world’s financial leader in the future. At the beginning of July, the Shanghai Composite, not the S&P 500, is the best indicator of the global risk appetite, the US stock index is following the Chinese and not vice versa.

When they were moving in opposite directions in 2018-2019, investors saw this as a signal that the US was winning the trade war. Donald Trump could afford to use a carrot-and-stick policy to force China to sign the trade deal profitable for the US. Now, Washington can only use minor threats, including hints at bans on TikTok or the entry of Chinese students into the USA, as well as the decision to unpeg the Hong Kong dollar to the US dollar, which would create problems for foreigners working with the Chinese markets. Beijing, which didn’t respond to the US attacks earlier, now makes loud statements that the current US policy, based on strategic misjudgments that lack factual evidence, is a paranoia.

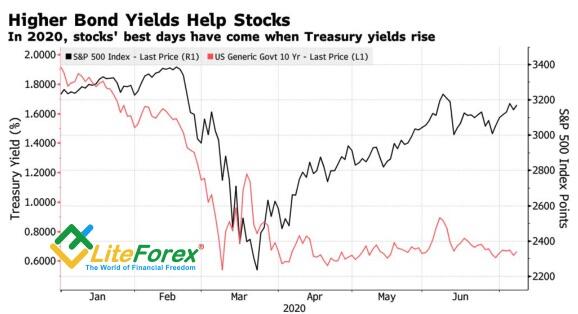

China is now more confident, gaining strength also because the Shanghai Composite is steadily growing, and Donald Trump’s approval ratings are falling. According to Goldman Sachs, the probabilities that Joe Biden will capture the White House, and Democrats will gain control of the Senate, are 43% and 62%, up from 30% and 61% in February. If Trump hints at the escalation of the US-China trade war under the current conditions, the S&P 500 drop will ruin his plans for re-election. The US stock index is now following its China’s peer, and experts say the S&P 500 is not responsive to the deterioration of the epidemiological situation in the USA. They explain it by the Fed’s huge monetary stimulus that has pressed the Treasury yields down. However, the US stock market rose when the Treasury yields were growing. This signals that the S&P 500 reacts to the US economic state, not to the low interest rates.

A tail-wind from Asia followed by growth of the risk appetite is a reason to sell safe havens, including the US dollar. The EUR/USD has hit its monthly highs also because of Angela Merkel's statement. Germany's chancellor says the eurozone has seen “huge economic upheaval” and the governments cannot afford to “waste any time” discussing the plans to protect the euro-area economy. Merkel underlined the need to swiftly adopt the French-German €750-billion recovery plan. The decline in the yield spread between the bonds of the euro-area peripheral countries and Germany to the lowest levels since March signals that the financial stress has eased.

Euro looks strong, it should try to break out the resistances at $1.1385 and $1.1405. If the resistances are broken out, the bulls will go ahead, and the price will continue rising.

Dynamics of S&P 500 and Treasury yields

Fundamental Euro forecast for today

The EUR/USD bulls are supported by good news from Asia and the stabilization of European financial markets.

For a long time, the entire financial world has been following the US, depending on the US stock indexes. However, the economic situation in the US is like “hope for the better but prepare for the worse”, and other countries are now coming in the game. The continuous growth of the Chinese stocks over the last seven days and the yuan’s rise to its four-month highs indicate the strength of China’s economy, which might become the world’s financial leader in the future. At the beginning of July, the Shanghai Composite, not the S&P 500, is the best indicator of the global risk appetite, the US stock index is following the Chinese and not vice versa.

When they were moving in opposite directions in 2018-2019, investors saw this as a signal that the US was winning the trade war. Donald Trump could afford to use a carrot-and-stick policy to force China to sign the trade deal profitable for the US. Now, Washington can only use minor threats, including hints at bans on TikTok or the entry of Chinese students into the USA, as well as the decision to unpeg the Hong Kong dollar to the US dollar, which would create problems for foreigners working with the Chinese markets. Beijing, which didn’t respond to the US attacks earlier, now makes loud statements that the current US policy, based on strategic misjudgments that lack factual evidence, is a paranoia.