Simplify

- 专家

- Tomas Michalek

- 版本: 2.0

- 更新: 21 五月 2021

- 激活: 10

Trading has never been easier.

Simplify makes trading effordless. Your only work here is to buy it, attach to the EURUSD on H1, set your risk and wait for results.

Strategy was developed by genetic algorithms and of course tested by advanced robustness tests and delivered to you.

It is great addon to your portfolio or as standalone strategy.

Benefits for you

Amazing Plug & Play system - studying configuration and finding the best optimization is history. This work is included in the price and I did it for you already.

Every position has predefined configurable stoploss as a fixed amount per trade (you can risk fixed percenage of your initial balance).

Strategy is developed by genetic algorithms on long data period and as always, it passed all 9 robustness tests, so you know what you can expect from future trades.

Technical parameters

· CustomComment - choose your comment to distinguish strategy, or keep default

· MagicNumber - choose your number to distinguish strategy, or keep default

· mmRiskedMoney - configurable fixed amount, so you can risk portion of your initial balance

Screenshots

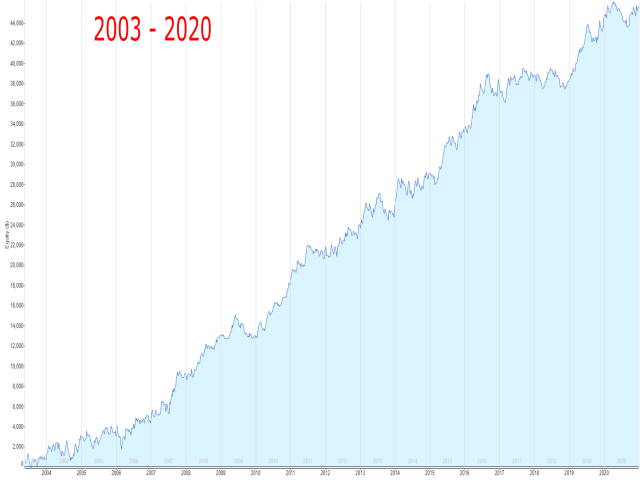

· Strategy equity for 17 years: nicely looking equity curve of backtest, which was done on precise data from Dukascopy from 2003 to 2020. Used default MM (300$).

· Strategy statistics for 17 years: see the results over 17 years long backtest - on historical data strategy had great Return/DD ratio, Profit Factor and stability.

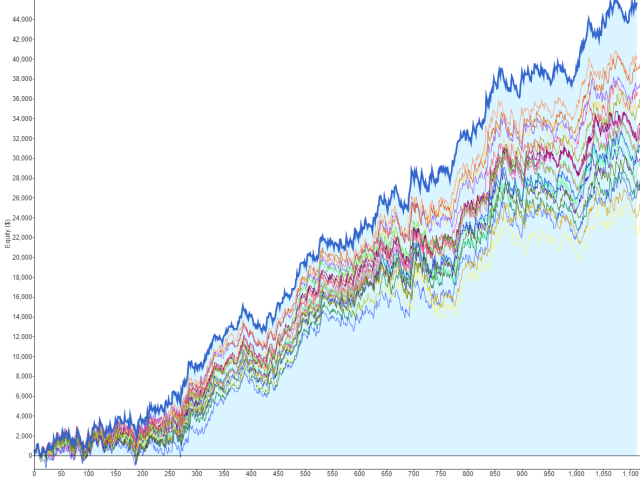

· Monte Carlo analysis - randomized slippage, spread and historical data: simulation of real market conditions and test of strategy sensitivity to market volatility and liquidity. Lines similar to original backtest means good robustness of the strategy.

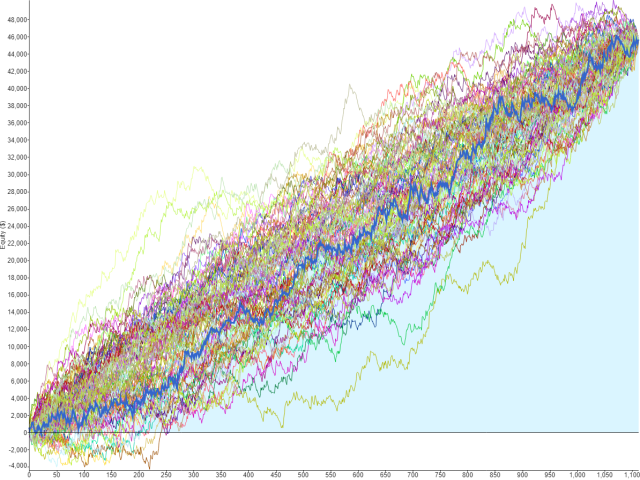

· Monte Carlo analysis - randomized trades order: test, which tells us whether the strategy is sensitive to specific market cycles. According to the picture, the strategy is not sensitive to the specific order of trades.

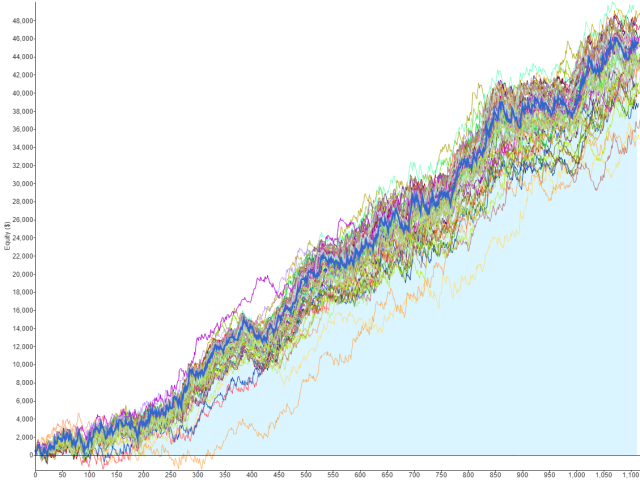

· Monte Carlo analysis - randomized strategy parameters: test against over-fitted strategy, even with randomly changed indicator parameters the strategy showed profitable results.

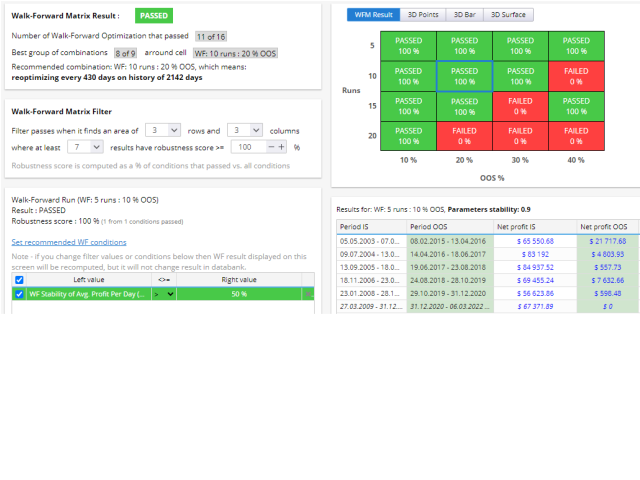

· Walk-forward matrix - complex series of simulations, where we optimize strategy parameters based on one period and then do the backtest on another period, comparing whether results are profitable. These steps are then repeated for the next time periods, which leads to the creation of a matrix of executed tests. The goal of this test is to find out, whether the strategy is over-fitted. If strategy won't work with slightly different parameters, it is most probably over-fitted and won't work in the future. You can see on the screenshot that the strategy was profitable for a lot of various optimization iteration on historical data.

用户没有留下任何评级信息