Currency crosses

- Experts

- Fuguang Liu

- Versão: 1.1

- Atualizado: 26 agosto 2024

- Ativações: 5

The classic never goes out of style, and the triple currency balance hedging arbitrage is a common currency arbitrage method in the original quantitative trading, but the conventional triangle arbitrage is not easy to achieve due to spreads, slippage, swaps, handling fees, etc.

In order to achieve profits, we have made optimizations in this strategy, breaking the concept of balanced arbitrage, using factors such as the judgment of entry opportunities, the staggered entry time, and increasing or decreasing the position of currency pairs, etc., to break the balance but maintain relative stability, and then realize the unbalanced indirect arbitrage, which has been tested for many years and has been tested by the market.

Strategy Features:

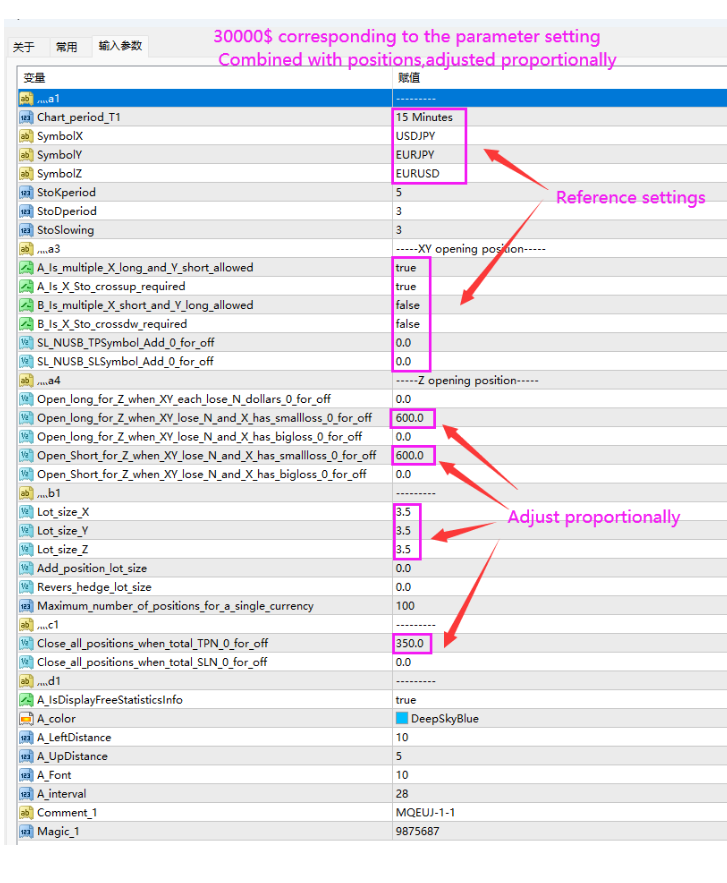

1. The strategic target currency pairs USDJPY, EURJPY, EURUSD, enable the logical USDJPY and EURJPY priority hedging, generate profits and exit the target value, otherwise, when there is a loss, calculate the strength of EUR and USD, and start the EURUSD currency to hedge again.

2. Assuming that arbitrage cannot be achieved for a long time, the strategy has the function of further increasing (or decreasing) USDJPY and EURJPY positions.

3. Instead of brainless hedging, you can enter the market after judging the direction according to the trend inflection point of different cycles, which increases the possibility of rapid arbitrage after entering the market

4. When you use it, you can load it on a currency of USDJPY, select the period you want to operate, and choose the 15-minute chart

5. Although there are no strict requirements, low spreads, low overnight fees, and low handling fees will be more friendly to the strategy