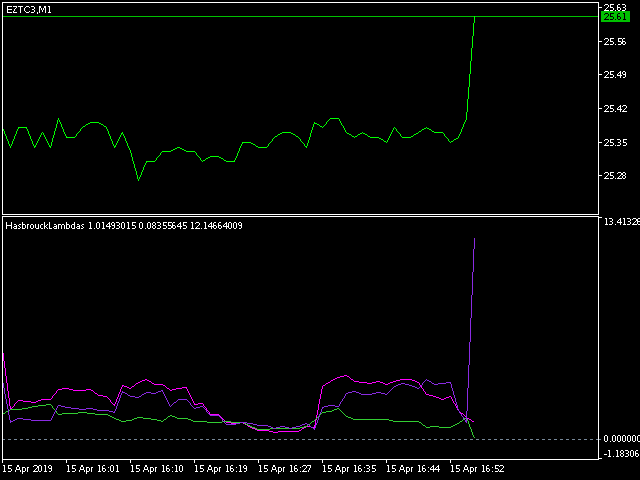

Hasbrouck Lambdas Estimator

- Индикаторы

- Roberto Spadim

- Версия: 1.0

- Активации: 5

Hasbrouck follows up on Kyle’s and Amihud’s ideas, and applies them to estimating the price impact coefficient based on trade-and-quote (TAQ) data.

Consistent with most of the literature, Hasbrouck recommends 5-minute time-bars for sampling ticks.

This indicator is based on Advances in Financial Machine Learning 2018 - Marcos Lopez de Prado book, Page 289.

---

This code can run slow when using big timeframes, it use copytick to get dollar volume, in a next version I will implement a temporary indicator to cumulative sum this values as a buffer