Turtle Signal

- Indicadores

- Vu Duy Hoang

- Versão: 1.0

- Ativações: 20

* Who were the Turtle Traders?

The Turtle Trader legend began with a bet between American multi-millionaire commodities trader, Richard Dennis and his business partner, William Eckhardt. Dennis believed that traders could be taught to be great;

Eckhardt disagreed asserting that genetics were the determining factor and that skilled traders were born with an innate sense of timing and a gift for reading market trends. What transpired in 1983-1984 became one of the most famous experiments in trading history. Averaging 80% per year, the program was a success, showing that anyone with a good set of rules and sufficient funds could be a successful trader.

In mid-1983, Richard Dennis put an advertisement in the Wall Street Journal stating that he was seeking applicants to train in his proprietary trading concepts and that experience was unnecessary. In all he took on around 21 men and two women from diverse backgrounds. The group of traders were shoved into a large sparsely furnished room in downtown Chicago and for two weeks Dennis taught them the rudiments of futures trading. Almost every single one of them became a profitable trader, and made a little fortune in the years to come.

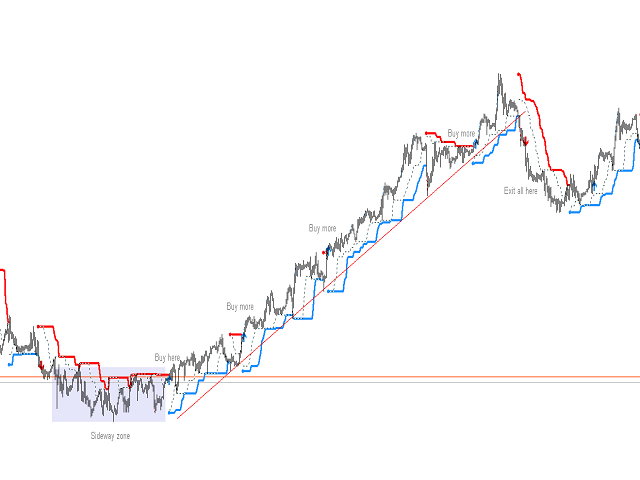

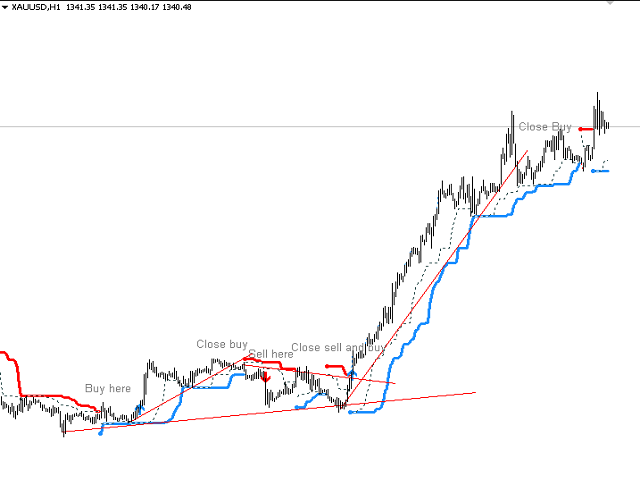

* The entry strategy

The Turtles learned two breakout variants or "systems". System One (S1) used a 20-day price breakout for entry. However, the entry was filtered by a rule that was designed to increase the odds of catching a big trend, which states that a trading signal should be ignored if the last signal was profitable. But this filter rule had a built-in problem. What if the Turtles skipped the entry breakout and that skipped breakout was the beginning of a huge and profitable trend that roared up or down? Not good to be on the sidelines with a market taking off! If the Turtles skipped a System One 20-day breakout and the market kept trending, they could and would get back in at the System Two (S2) 55-day breakout. This fail-safe System Two breakout was how the Turtles kept from missing big trends that were filtered out. The entry strategy using System Two is as follows: Buy a 55-day breakout if we are not in the market Short a 55-day breakout if we are not in the market The entry strategy using System One is as follows: Buy a 20-day breakouts if last S1 signal was a loss Short a 20-day breakouts if last S1 signal was a loss The Turtles calculated the stop-loss for all trades using the Average True Range of the last 30 days, a value which they called N. Initial stop-loss was always ATR(30) * 2, or in their words, two volatility units. Additionally, the Turtles would pile profits back into winning trades to maximize their winnings, commonly known as pyramiding. They could pyramid a maximum of 4 trades separated from each other by 1/2 volatility unit.

* The exit strategy

The Turtles learned to exit their trades using breakouts in the opposite direction, which allowed them to ride very long trends.

The exit strategy using System Two is as follows: Exit long positions when the price touches a 20-day low Close shorts positions when the price touches a 20-day high The exit strategy using System One is as follows: Close long positions if/when the price touches 10-day low Close short positions if/when the price touches a 10-day high