NightBird Scalp

- Experts

- Enric Paulo Pedreny

- Versão: 1.4

- Ativações: 10

NighBird Scalp:

It is an algorithm developed for low volatility scenarios, where the market is in a small rank period. The algorithm will look for a small target with an adjustable risk. It works in 15 minute temporalities. (Only one order is executed at the same time by Set)

Filters and conditionals are incorporated into the code, so they will not be disclosed to the public for copyright reasons. In robot properties you can see that there are only time and maximum risk parameters per operation, making it very easy to optimize. (Likewise the output of the algorithm either by TakeProfit or StopLoss, is incorporated into the algorithm, at most it will lose the maximum% per operation)

Parameters of the Indicator:

- Monday: daily filter (true / false)

- Tuesday: daily filter (true / false)

- Wednsesday: daily filter (true / false)

- Thursday: daily filter (true / false)

- Friday: daily filter (true / false)

- HoursFrom: time filter (0-24)

- HoursTo: time filter (0-24)

- BalanceRiskPercentBuy: Risk for purchase operations (0.01-5)

- BalanceRiskPercentSell: Risk for sales operations (0.01-5)

- StopLossPips: StopLoss measured in pips (With this parameter it will be calculated how much input volume according to the percentage of risk "StopLossPips >= 15 pips & StopLossPips <= 200 pips" )

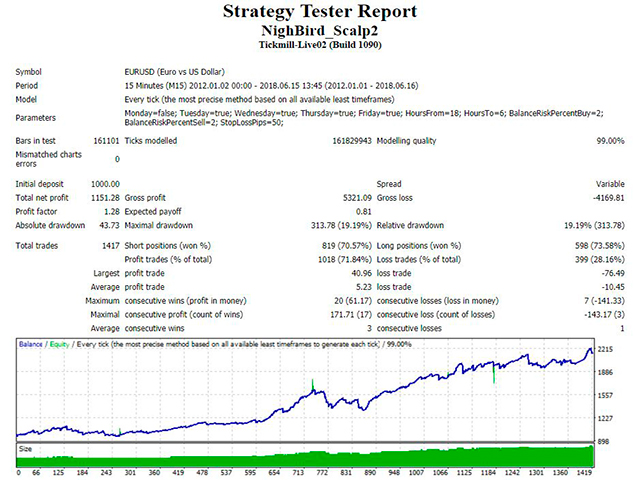

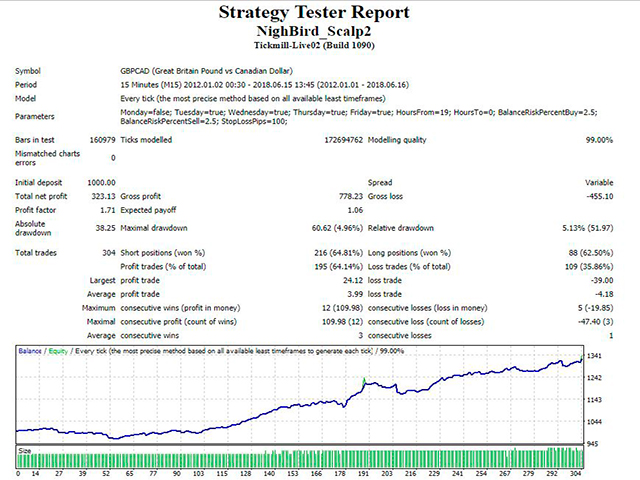

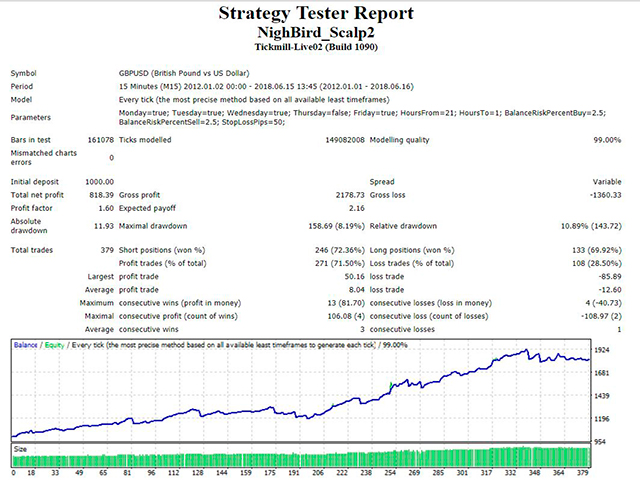

The tests were conducted on the EURUSD, GBPUSD and GBPCAD, on M15, with variable Spread conditions and a MarkUp of $ 4, at GMT + 3. Likewise, the quality of the modeling is 99%, data purchased from TickData Suite 2.

For small and large capitals.

Attention: it is advisable to execute the algorithm in brokers with low spread and commission conditions.

"Modifications will be added in new versions at the request of users"Currently the pairs with JPY and for Commodities are deactivated, in the next update they will be incorporated.