|

10+ años

experiencia

|

0

productos

|

0

versiones demo

|

|

0

trabajos

|

0

señales

|

0

suscriptores

|

Tobias Fedier

· 4

Mostrar todos los comentarios (5)

Matthew Todorovski

2014.12.14

Depends on the question. Some SD requests are still open for me for months... have they forgotten?

Tobias Fedier

· 4

Tobias Fedier

2014.11.16

Yea i wanted to add some more but unfortunately my MT4 crashes all the time :D

Manuel Jesus Barrera Velazquez

2014.11.19

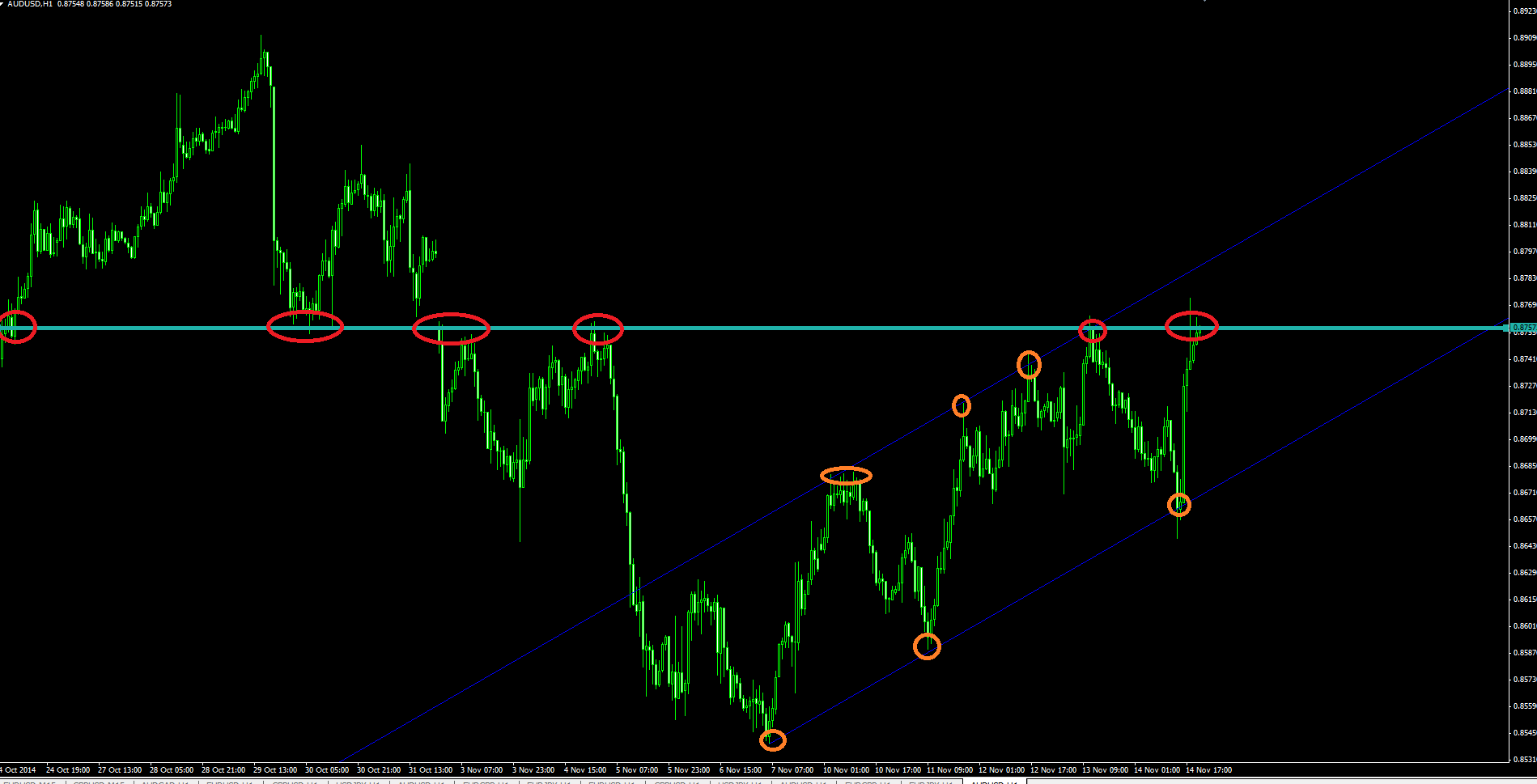

Whats can you see here??? Are you see anything here???????????? Its imposible to look something????