KT Hull MA MT4

- Indicadores

- KEENBASE SOFTWARE SOLUTIONS

- Versión: 1.0

- Activaciones: 5

It's a modified, and improved version of the classic HMA developed initially by Alan Hull in 2005. It uses a combination of three weighted moving averages to reduce the lag.

- Long Entry: When HMA turns blue from red with an upward slope.

- Short Entry: When HMA turns red from blue with a downward slope.

Features

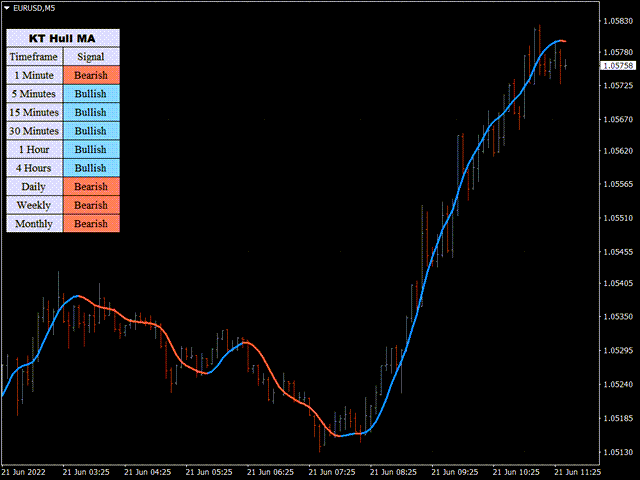

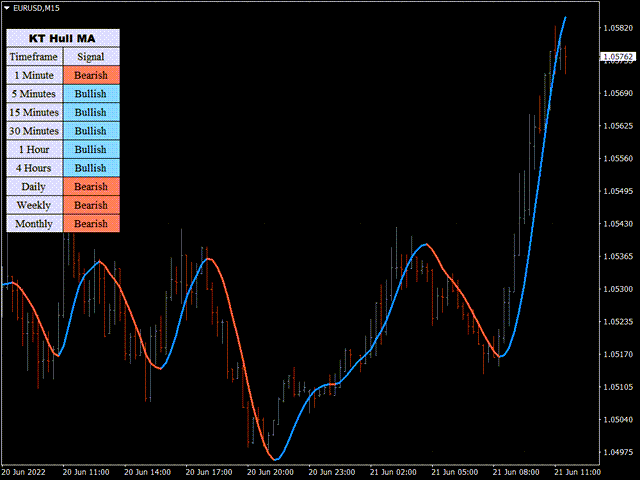

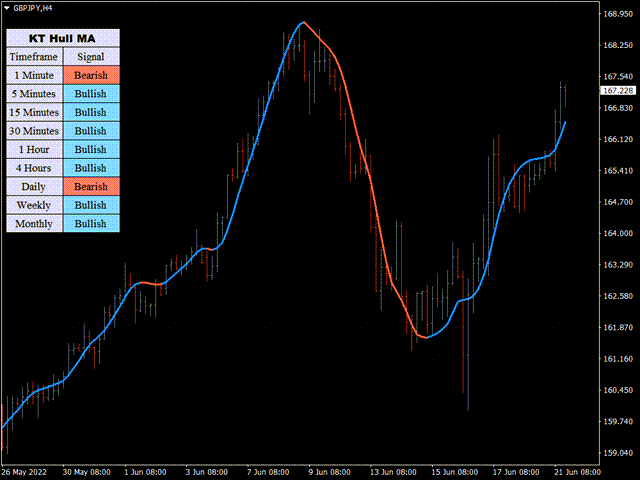

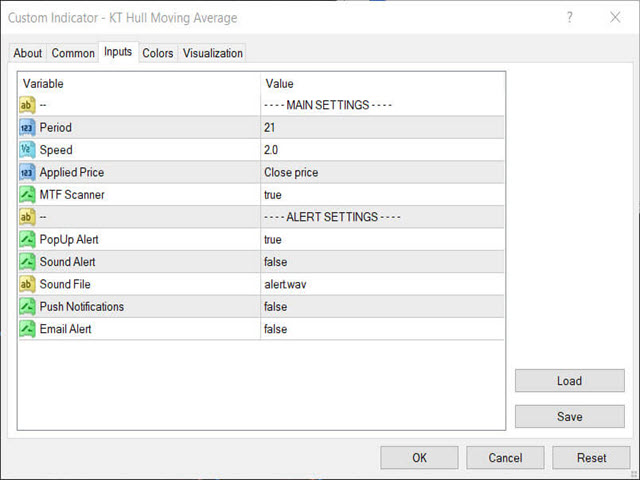

- It comes with a multi-timeframe scanner which scans for the new signals across all the timeframes.

- HMA reduces lags which usually come with the traditional moving averages.

- Effectively identifies the starting and ending of a new emerging trend.

- It comes with all MetaTrader alerts.

HMA Formula

The Hull moving average is calculated using three weighted MA combinations:

- WMA1 = P x WMA

- WMA2 = P/2 x WMA

- Raw HMA = (2 x WMA1) - WMA2

- Final HMA = WMA(sqrt(P)) of Raw HMA

P = Period

WMA = Weighted Moving Average

Pro-Tip

You can use the HMA standalone. However, we suggest using it with other indicators to improve the signal's accuracy. Also, it's practical to confirm the HMA's signals using the Multi-timeframe scanner.