AIS Kolmogorov Zhurbenko Filter

- Indicators

- Aleksej Poljakov

- Version: 1.0

- Activations: 5

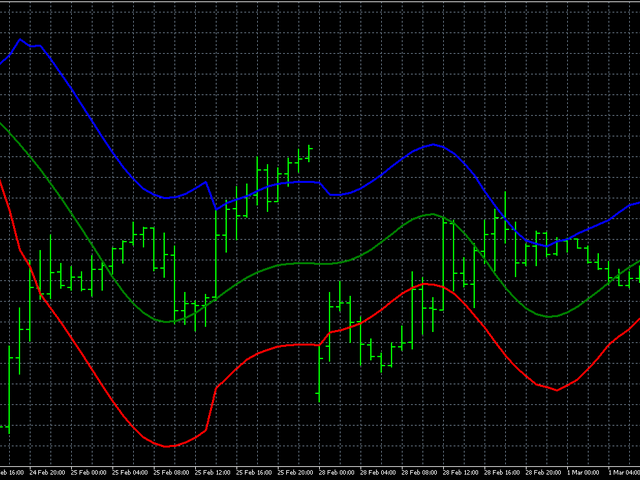

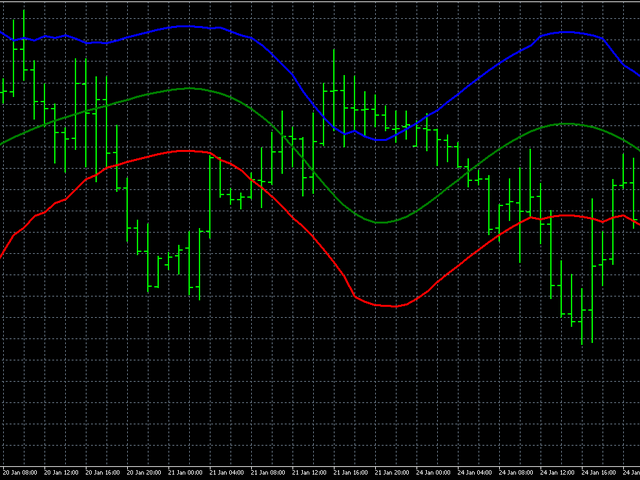

The Kolmogorov-Zhurbenko filter can be considered as a special window function designed to eliminate spectral leakage. This filter is optimal for smoothing stochastic (including financial) time series.

The indicator based on this filter contains the following parameters:

- iLength - the period of the original rectangular window used to build the filter. Valid value is 2 - 255.

- iDegree - filter order. If iDegree=0, then a simple moving average will be obtained. If iDegree=1, then you get a triangular moving average. Higher orders allow for better smoothing and noise suppression. Allowed value is 2 - 255. Also, this parameter affects the final period of the indicator = iLength + iDegree * (iLength - 1).

- iMultiplier - a multiplier showing the number of standard deviations counted from the filter value.

The appearance of the indicator is shown in the pictures.