EA Gone Rogue... Help!!

I wrote a Super Trend Hull indicator advisor: Super Trend Hull EA

The EA checks the value in the color buffer on the current bar and on the previous one.

Super Trend Hull EA

- www.mql5.com

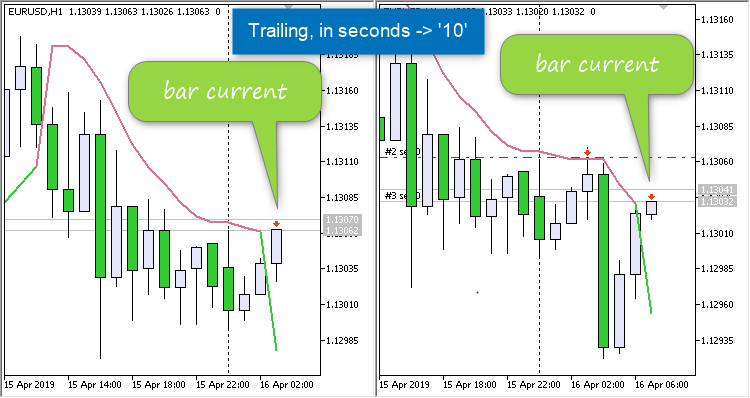

на баре может быть только одна сделка 'вход в рынок' (это внутренний параметр, он не вынесен во входные параметры и это не имеет отношения к параметру ' Only one positions') при работе в режиме 'внутри бара' ('Search signals, in seconds' больше или равно '10') текущий бар - бар #0, при работе в режиме 'только в момент рождения нового бара'...

Vladimir Karputov:

I wrote a Super Trend Hull indicator advisor: Super Trend Hull EA

The EA checks the value in the color buffer on the current bar and on the previous one.

That is great. Taking a look.

Thanks.

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

Hello,

Thanks in advance for even taking a look.

Super Trend Hull by Mladen

EA by VR---BUCH(barabashkakvn's edition).mq5 Copyrighted to Voldemar227.

I have been trying to do this with my limited trading and coding knowledge.

Buy when the super trend hull indicator is limegreen and sell when voiletred

I am pretty much stuck. The only time the EA takes trades is when I do

bool buy = (green[0]) which certainly is not my intention.

edit: I sort of exceed the maximum characters allowed so I have attached the full code.