Press review - page 325

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

AUDIO - How To Make Money When Things Go Nowhere with Steve Moses

On a day when the markets rocketed to the upside, Merlin welcomes Steve Moses to help viewers understand the trading potential for Options. Steve’s preferred options strategy is spread trading, which allow him to profit when securities go sideways. The duo talk about this, and the other ways to use options to capitalize on market moves as well as how to generate income.

Morgan Stanley Chart Of The Week: EUR/USD Key Triggers (based on efxnews article)

On the long-term EUR/USD Chart

"Despite the corrective rebound developed since early March, EURUSD remains within a long term down trend, which accelerated from June of last year. Indeed, this move lower over the past year forms part of a C wave decline within a broad multi year corrective structure which has developed since the 1.6038 peak of 2008. The pace of decline over the past year is typical for a C wave. This suggests upside potential is limited for EURUSD," MS notes.

On the 2-Year EURUSD Chart

"The sub-structure of the decline from June of last year has been “impulsive”, with a 3 rd wave within the C wave now developing. The subsequent recovery since March has developed a clear 3-wave corrective structure, which now looks to have been completed at the 1.1467 mid-May peak (4th wave top within wave (3). This implies the next stage of the EURUSD decline (5th wave within wave (3)) is now likely to unfold," MS projects.

On the 90-Day EURUSD Chart

"This bearish interpretation will be confirmed by a move below 1.1005, suggesting the next impulse decline is set to take EURUSD below the 1.0854 level and back to the 1.0458 March low. This even implies a move to new lows with potential for a decline below parity over the medium term. Near-term risk to this scenario is a move above 1.1467, which would suggest another corrective leg higher before the downtrend resumes." MS argues.

Skandinaviska Enskilda Banken (SAB) - Intraday Outlooks for EURUSD, EURJPY and EURGBP (based on efxnews article)

EUR/USD: With yesterday’s downside correction out of the way there’s a big question mark over what the next step from here will be. However as long as the hourly pattern with lower highs remains in place (i.e. staying below 1.1278) we will hold a light downside bias.

EUR/JPY: With a relatively high probability we’re now in for a third attempt to break below the 138.44 support. The key question will of course be whether the break will be sustained or not. A sustained break lower will increase the probability that we prematurely have ended the C-wave (theoretical target = 143.96) and hence the entire correction from the April low.

EUR/GBP: With the latest development, the break and close below 0.7267, we can with a lot higher confidence call for wave C to now have been put in place. More losses are expected near term with focus at the ideal point for wave D, 0.7127.

EURUSD trades in mid range in a Friday wander (based on forexlive article)

The EURUSD followed mainly below the 100 hour moving average and Asia-Pacific trading. In the European session, the pair tried to hold support at the 200 hour MA - like yesterday - but gave way and extended the narrow trading range (at the time). The pair is not back above and below the 200 hour MA at 1.1222 .The topside trend line and 100 hour MA loom ahead as a level to target at 1.1255 and 1.1267 respectively. The pair is stuck near mid range. Near the 200 hour MA. Below the 100 above. The 38.2% is below at 1.1168. We are kinda in a place of neutrality.

Forex Weekly Outlook June 15-19 (based on forexcrunch article)

The US dollar did not lick honey against most currencies despite some OK data. The focus now moves to the all-important Fed decision. In addition we have housing and inflation numbers in the US, rate decisions in Japan and Switzerland and the ongoing Greek crisis. These are among the main events on forex calendar for this week. Here is an outlook on the market movers coming our way.

The released positive economic data with better than expected retail sales figures. American consumers increased their purchases in May, especially for autos, clothes and building materials, suggesting the improvement in the labor market boosted sales. Alsoconsumer sentiment for June beat expectations, but most market analysts doubt this is enough for an early rate. In the euro-zone, Greek headlines had a growing impact on the common currency as the clock is ticking. The Aussie enjoyed a good employment report while the kiwi fell sharply on a rate cut. Where will currencies move next?

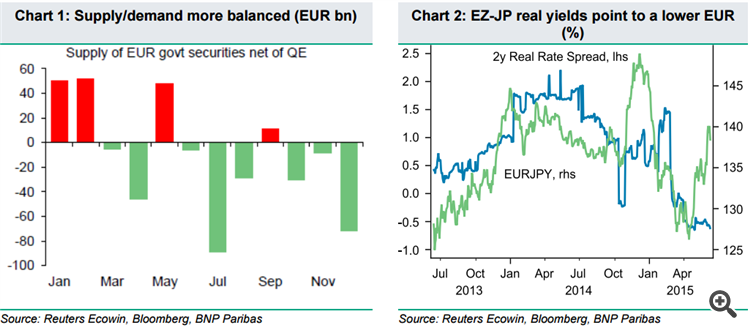

BNP Paribas - Here Is Why The EUR Will Re-Emerge As A Funding Currency Soon (based on efxnews article)

"The rise in eurozone bond yields has caused the EUR’s status as a funding currency to fade in recent weeks and the JPY to overtake as the favoured currency for the market to sell, especially as a funder for long USD positions. This switch in focus has caused EURJPY to rise 10% over the past two months, reaching its highest level since January earlier this week.

The EUR should re-emerge as the main funding currency.

i. The rise in the EUR in recent weeks has corresponded to the rise in eurozone bond yields. Our interest rate strategy team highlight that the rise in eurozone yields is likely to be nearing an end.

Firstly, German bond yields are now much closer to model gauges of ‘fair value’ following the bond sell-off.

Second, the net supply picture is better for European bonds as we move into the summer months and expect better performance ahead (Chart 1). We expect a decline in yields over the months ahead to encourage EUR-funded carry trades to be re-established.

ii. Our Positioning Analysis indicates that short EUR positioning is at light levels with a score of -10 (out of -50), having reached -4 last week (its lightest level since the start of the year). As such, there appears to be substantial scope for short EUR positions to be restoredMorgan Stanley - Outlooks for the Coming Week for USD, EUR, JPY, GBP and AUD (based on efxnews article)

USD: EM and G10 Divergence. Neutral.

We remain medium-term USD bulls, though in the near term we see scope for retracement. The failure of the USD to rally following last week’s strong payrolls print suggests that momentum is against the currency. What’s more, recent comments from policymakers in Japan suggest that USD strength may becoming detrimental for economies, and could drive a near-term retracement, particularly given signs of long USD positioning.

EUR: Draghi Gives EUR Legs. Bearish.

EUR could see further strength in the near term as European yields continue to rise. Thus far, European equities have held up well despite the sell off in European rates – if this starts to turn around, it could counterintuitively offer further support to EUR as investors are forced to buy back their short EUR hedges. The reluctance of Draghi to push back on market volatility suggests that European bond yields could rise further. Greece remains a major risk factor for the EUR.

JPY: A Shift towards strength. Bullish.

Prime Minister Kuroda’s comments on the strength of the JPY are likely to make JPY the outperformer over coming weeks. Indeed, JPY is trading near historical lows on a REER basis, and we see scope for some retracement from recent weakness. In addition, signs of reflation in Japan reduce the probability of further BoJ easing. Higher market volatility should weigh on risk appetite, also adding to JPY support.

GBP: Data filled week. Neutral.

The rise in GBPUSD has been mainly driven by USD weakness. Should this continue then we would expect GBP to remain supported. However we continue to highlight that the performance of GBPUSD is mainly driven by rate expectations. This week’s set of data: inflation, employment and retail sales will therefore be important. We put particular emphasis on average weekly earnings in the services sector. A strong reading here should support GBP and inflation expectations

AUD: Carry and Commodities Undermined. Bearish.

We remain bearish on AUD and high carry currencies generally. As volatility rises and core yields head higher, volatility adjusted rate differentials become less attractive, removing support for AUD. The latest comments from the RBA suggest the central bank wants to support the economy but is concerned about financial stability risks associated with rate cuts, making the currency a good tool. We will watch the upcoming RBA minutes for further color.Key Technical Levels Remain for USD-pairs as Week Ends (based on dailyfx article)

"It's a much quieter day on the economic calendar, with only one event due over the next few hours that qualifies as a 'medium' or 'high' ranked event to close out the week. Instead, attention will be focused on two developing themes as the week draws to a close: the rebound in US economic data; and the negotiations surrounding Greece."

Morgan Stanley: EUR/USD Elliot Wave technical analysis (based on forexlive article)

Ian Stannard from Morgan Stanley: "despite the corrective rebound developed since early March, EURUSD remains within a long term down trend... suggests upside potential is limited for EURUSD" and the "sub-structure of the decline from June of last year has been "impulsive... the next stage of the EURUSD decline ... is now likely to unfold."

"This bearish interpretation will be confirmed by a move below 1.1005, suggesting the next impulse decline is set to take EURUSD below the 1.0854 level and back to the 1.0458 March low. This even implies a move to new lows with potential for a decline below parity over the medium term. Near-term risk to this scenario is a move above 1.1467, which would suggest another corrective leg higher before the downtrend resumes."

Barclay: The Case For Staying Short EUR/USD Into FOMC (based on efxnews article)

"Markets will pay close attention to the tone of the FOMC statement on Wednesday and watch for hints on the timing of the first rate hike. Given the recent pickup in US consumption and labor market data, we think the Fed is likely to maintain its view that the winter slowdown was transitory and that the economy is likely to expand at a moderate pace. Indeed, the pace of job growth has picked up, with payrolls rising 280K in May, and the Fed’s LMCI has increased since the April meeting. Additionally, we expect the Fed to reiterate that inflation will gradually rise toward the 2% target in the medium term as the labor market continues to improve and inflation expectations remain stable," Barclays clarifires.

"Indeed, CPI data on Thursday, along with the latest import price data, should support our view that downward pressures on domestic core inflation from the lagged effects of USD appreciation will begin to wane going into the third quarter. As such, we continue to think the Fed is on track to hike twice this year (at the September and December meetings)," Barclays projects.

"Overall, we believe that the FOMC statements, along with CPI and other macro data, should support the USD," Barclays argues.

"Greek political uncertainty remains high, as the gap in negotiations between Greece and the Institutions remains substantial. The IMF is reported to have walked away from talks with Greek officials on Thursday because of the inability to find agreement on such issues as pension and tax reforms. Meanwhile, the economic and financial situation is continuing to deteriorate in Greece, with the state revenue shortfall having grown €1bn in May to reach a total of €2bn, and with the ECB having last week raised the limit on the Emergency Liquidity Assistance (ELA) to Greek banks by a further €2.3bn, to €83bn. The Eurogroup and ECOFIN meetings will be held on 18 and 19 June, respectively," Barclays notes.