Join our fan page

- Views:

- 4167

- Rating:

- Published:

- 2018.06.18 16:21

-

You are missing trading opportunities:

You are missing trading opportunities:- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration Log inYou agree to website policy and terms of use

If you do not have an account, please register -

Need a robot or indicator based on this code? Order it on Freelance

Go to Freelance

Need a robot or indicator based on this code? Order it on Freelance

Go to Freelance

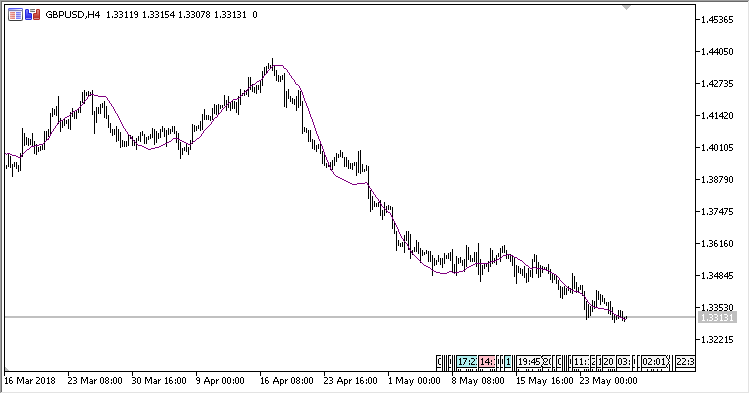

Indicator Kalman Filter. It allows efficiently smoothing the noise, extracting the main trend from it.

Kalman Filter is a variety of recursive filters. To assess the system status as of the current operation tact, it needs a status assessment (as the system status assessment and the error assessment of defining this status) at the preceding operation tact, and measuring at the current tact. This property distinguishes it from packet filters requiring to know at the current operation tact the history of measurements and/or assessments.

More about Kalman Filter.

The indicator has three input parameters:

- K - Kalman factor;

- Sharpness - factor for calculating the error minimization;

- Applied price - price used for calculations.

Calculations:

Kalman[i] = Error + Velocity[i]

where:

Error = Kalman[i-1] + Distance * ShK Velocity[i] = Velocity[i-1] + Distance * K / 100 Distance = Price[i] - Kalman[i-1] ShK = sqrt(Sharpness * K / 100)

Translated from Russian by MetaQuotes Ltd.

Original code: https://www.mql5.com/ru/code/20916

HL_StdDev

HL_StdDev

The oscillator shows standard deviation calculated on the difference between the High and the Low.

EMA_Trend

Two channels by the High and Low of MA.

Wiseman

Wiseman is an indicator basically aimed at showing the candlestick, on which the trend has changed its direction.

Rainbow_Volume

A colored tick-volume indicator.