The market expects USD to remain largely range bound against G10 low yielders (EUR, CHF, JPY) for the most of the week, with some upside risks to USD on Fri due to the likely rebound in the April US retail sales (consensus is looking for a strong 0.8% MoM reading, from -0.3% previously). Given the very benign market pricing of the Fed funds path (only one rate hike fully priced in by 4Q17) and the shifting focus to the underlying US activity data as the missing ingredient for a potential policy tightening (given the signs of building US inflationary pressures and easing US domestic financial conditions), strong retail sales should support USD. New York Fed’s Dudley comments over the weekend that two rate hikes remain a “reasonable expectation” point to a limited room for further dovish re-pricing of the fed funds rate path from here.

The BoE May Inflation report (Thu) is the key GBP data point for the week. We may see a downward revision to the GDP outlook and the overall tone should not materially deviate from the current neutral-dovish bias. Over the coming weeks, the Brexit risk should be the key GBP driver and hence the Inflation Report forecasts are likely to be taken by the market with a pinch of salt (given that the BoE projections are based on the assumption of the UK remaining in the EU).

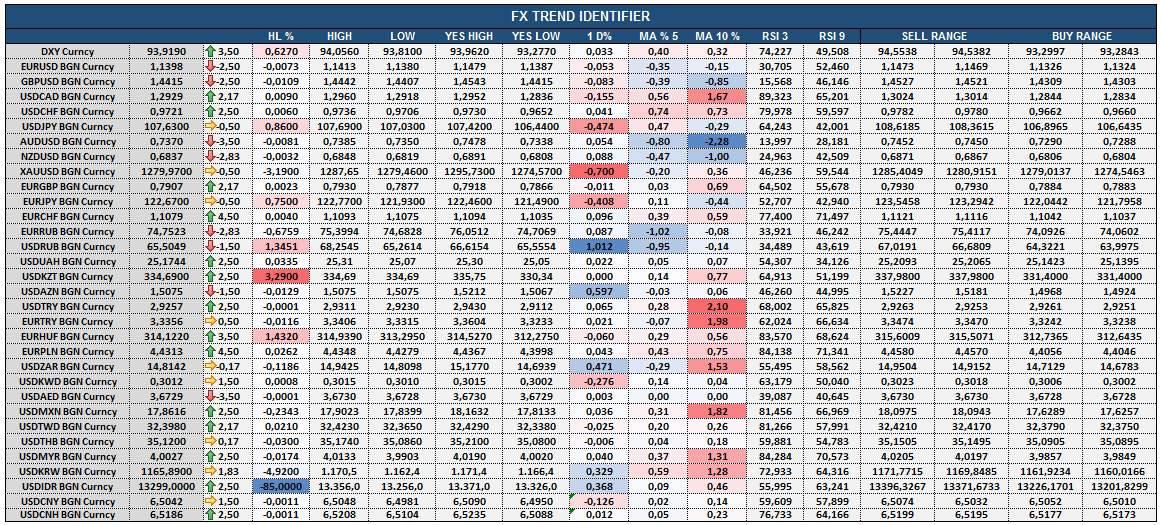

The price action remains mixed, USD is trying to make a come back after losing ground in the last two months. Low global interest rates has turned FX regimes into a competitive devaluation race if you look at the big picture. As of last two weeks higher yielding currencies have re entered rate cutting cycles. As a result AUD, NZD are lower on further rate cut expectations. Emerging markets currencies including TRY, ZAR, MXN and BRL are lower on politics, lower interest rates and fundamentals. Rub has remained relatively strong on oil but metals have been weak and Asia FX has been resisting a rally for the last week.