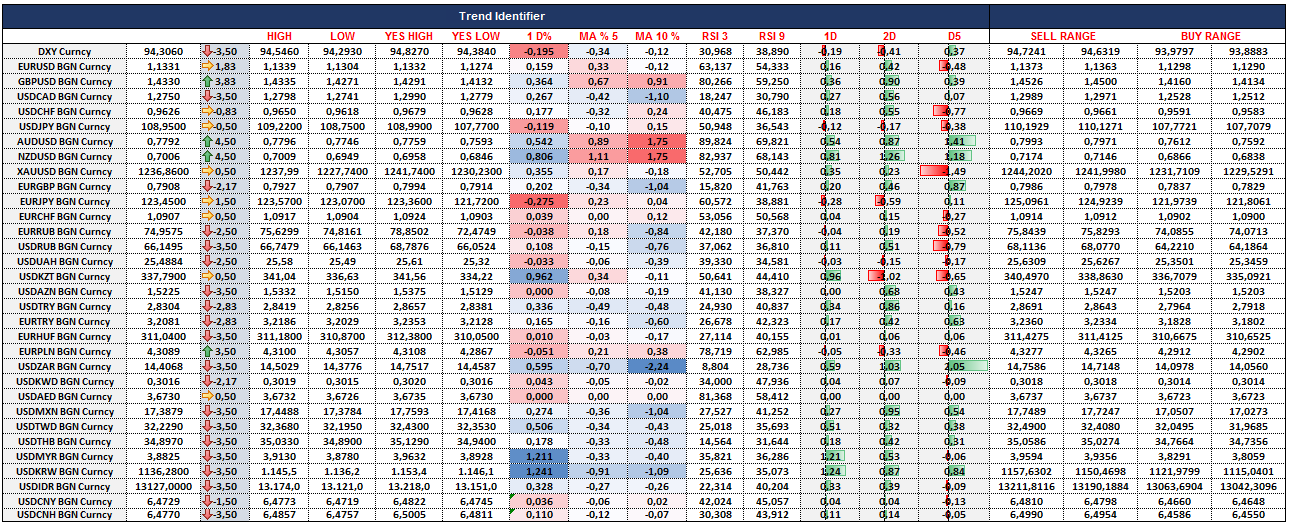

The recovery in oil prices since the Doha meeting may be indicative of a market that has support, though chasing upside in petro FX may prove futile once seasonal effects fade (May). DXY to trade sideways amid limited catalysts.All eyes will be on Governor Carney today who is due to appear before the House of Lords Economic Affairs Committee (1535 CET). While the implications of the forthcoming EU referendum is likely to dominate proceedings, also on the agenda is a discussion on China and its impact on the UK economy, as well as the million-dollar question – when will inflation return to the 2% target. Expect a broadly cautious tone from the BoE Governor as we suspect he may look to re emphasis some of the dovish assertions made in the April MPC minutes. With our economists looking for data later this week (employment growth and retail sales) to come in on a softer footing, we prefer to stay short GBP/USD. Price action wise, last two days have been about lower rates around the globe after the the oil rout. The initial reaction to the drop in oil price has been a widening in credit indexes but it seems the rally of the last few weeks has helped credit and risk in general get a better foothold. The cash that has been lying around for so long finally seems to be searching for yields and assets. The oil price move was largely discounted to be expected and USD weakness pushed commodities back higher. As DXY reenters weakening trend, AUD and NZD have pushed higher and remain in a trend to break higher. USDCAD is now pushing 1,2750 lows and trending lower. One exception is EUR, which has been trying to follow USD weakness but is having a hard time breaking through 1,1350s with inflation expectations still dropping. Almost all Asian Emerging Market pairs have been strong with CNH leading the charge. Even EMEA has done well, HUF and PLN have rallied strongly and TRY is trying to follow but is the underdog due to the central bank meeting and possible aggressive rate cut tomorrow. Ruble has rallied strongly with Oil and correlation has hit around 85%. It seems unless there is a major disappointment in the interest rates outlook, risk rally is here to stay.