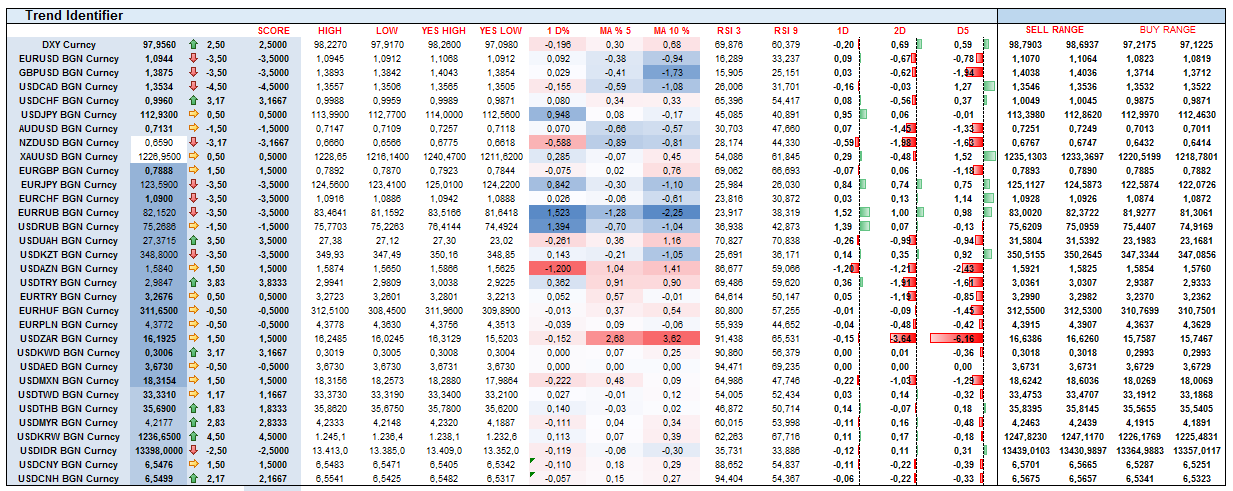

Last Friday saw a strong correction in the recent Emerging Markets rally that fueled some risk aversion afterwards. As far as I can see the main concern in KRW and TRY has been aggressive rate cuts being priced in as rates did not react in a credit negative way. ZAR did sell off badly due to political concerns which clearly was credit negative. EURUSD was pushed lower with some USD strength and ECB meeting closing up on the market, GBP was pushed lower by Brexit. NZD also got a rate cut push lower along with AUD. The strong trends remain in Oil, GBP, CAD and EUR.