Barclays Plc was so bent on lifting its private trading venue to the upper ranks of Wall Street dark pools that it lied to customers and masked the role of high-frequency traders, according to New York’s attorney general.

Barclays falsified marketing materials to hide how much high-frequency traders were buying and selling, according to a complaint filed today by Eric Schneiderman. Barclays runs one of Wall Street’s largest dark pools, a private trading venue where investors can trade stocks mostly anonymously. Mark Lane, a spokesman for London-based Barclays, declined to comment.

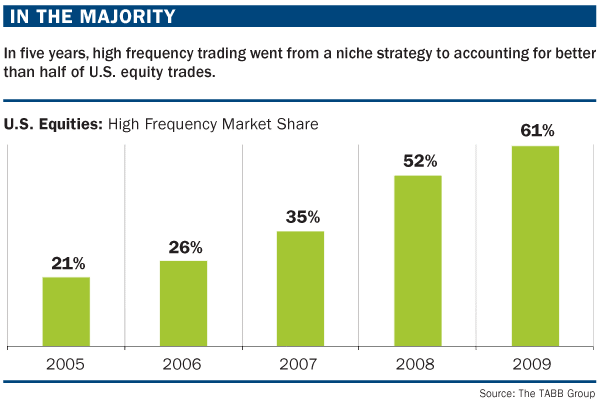

Schneiderman has taken a leading role in seeking to reform how equities trade in the $23 trillion U.S. stock market, examining whether exchanges and dark pools give unfair perks to high-frequency traders. Critics say firms using strategies built around buying and selling at rates measured in fractions of a second trade so quickly that others can’t compete.

Barclays Plc was so bent on lifting its private trading venue to the upper ranks of Wall Street dark pools that it lied to customers and masked the role of high-frequency traders, according to New York’s attorney general.

Barclays falsified marketing materials to hide how much high-frequency traders were buying and selling, according to a complaint filed today by Eric Schneiderman. Barclays runs one of Wall Street’s largest dark pools, a private trading venue where investors can trade stocks mostly anonymously. Mark Lane, a spokesman for London-based Barclays, declined to comment.

Schneiderman has taken a leading role in seeking to reform how equities trade in the $23 trillion U.S. stock market, examining whether exchanges and dark pools give unfair perks to high-frequency traders. Critics say firms using strategies built around buying and selling at rates measured in fractions of a second trade so quickly that others can’t compete.

“This is obviously a breach of confidence, a breach of trust,” said Joe Saluzzi, co-head of equity trading at Themis Trading LLC. “It’s pretty obvious at this point that the SEC needs to come in, it needs to know what’s going on actually inside these boxes. Barclays -- are they the only ones? We don’t know. I don’t know.”

Fortifying Suspicions

U.S. Securities and Exchange Commission Chairman Mary Jo White on June 5 voiced concern about the level of trading on venues where bids and offers are kept private, masking the true depth of demand for shares. Yesterday, the SEC said it would test a program to limit the amount of trading -- now roughly 40 percent of volume -- handled off public exchanges such as the New York Stock Exchange and Nasdaq Stock Market.

Schneiderman’s action will fortify a suspicion among critics of dark pools and high-frequency firms, which proliferated in the past decade with advances in computer power and efforts to spur competition among U.S. trading venues. Namely, that in the rush to attract traders to their markets and boost profits, the venues have catered to computerized market makers to the detriment of individuals.

“Everyone who cares about the integrity of our markets should be shocked by the conduct the complaint describes,” Schneiderman said today during a press conference.

In the complaint, filed in New York state Supreme Court in Manhattan, Schneiderman said Barclaystold customers that it was protecting them from “aggressive, predatory or toxic” high- frequency traders, while secretly courting them.

‘Fraud and Deceit’

Schneiderman painted a picture of “fraud and deceit” at Barclays perpetrated by unidentified executives who lied to customers about the role played by high-frequency traders in its market as part of an effort to increase its size. Some former “high-level” Barclays insiders helped frame the case, according to the complaint.

Seeking to reassure customers that their stock orders wouldn’t be picked off by predatory counterparts,Barclays touted a system designed to keep that from happening called liquidity profiling, according to the complaint. Marketing material including charts purported to show that very little of the trading within the dark pool was “aggressive” and that operating there was safe for institutions.

“The representations were false,” according to the complaint. The chart and accompanying statements misrepresented the trading taking place in Barclays’ dark pool. Senior Barclays personnel de-emphasized the presence of high-frequency traders in the pool and left out reference to one of the largest and most toxic participants, it said.

‘Taking Liberties’

“Internally, Barclays acknowledged that it was ‘taking liberties’ with the truth by suppressing the disclosure of this high frequency trading firm, but decided to falsify the analysis in order to ‘help ourselves,’” according to the complaint.

Expanding its dark pool to one of the biggest in the country “was a principal goal” of Barclays’electronic trading division in its quest to drive profits, according to the complaint. Attracting orders was important to building market share, reducing commissions paid to other venues and increasing fees collected from firms using the venue, it said.

Data from the Financial Industry Regulatory Authority shows that the Barclays LX venue is the second-largest U.S. dark pool, trailing only Credit Suisse Group AG’s Crossfinder.

Tradebot Systems

Barclays obscured the involvement on the dark pool of Tradebot Systems Inc., which had an “established history of trading activity that was known to Barclays as ‘toxic,’” according to the complaint. Tradebot is a high-frequency trading firm founded by its chairman, Dave Cummings, who declined to comment on the complaint.

Schneiderman accuses Barclays of violating New York’s Martin Act with counts of securities fraud and persistent fraud and illegality. The state seeks unspecified damages, disgorgement and restitution.

Dark pools were created as a haven for institutional investors seeking to trade large blocks of shares in secret, hoping to minimize their impact on prices so they can get a better deal on their trades. In practice, the average size of trades on private venues such as dark pools amounts to only 232 shares, according to SEC data released in October.

High-frequency traders have filled a void left by the exit of human market makers from the stock market and other securities. With trading profits so thin, few people can transact shares in the volume necessary to keep exchanges supplied with offers to buy and sell.

‘Juicy Prey’

On May 2, Bloomberg News reported that Schneiderman was planning to subpoena exchanges and has already requested information from dark pools in a probe related to high-frequency trading, a person familiar with the matter said at the time.

Michael Lewis’s “Flash Boys,” released in March, said bank-owned dark pools serve as a key intersection between high- frequency traders and brokers’ investor clients. The banks, Lewis wrote, charge high-frequency traders for the right to trade against orders placed by their brokerage customers.

“Why would anyone pay for access to the customers’ orders inside a Wall Street bank’s dark pool?” Lewis wrote. “The straight answer was that a customer’s stock market order, inside a dark pool, was fat and juicy prey.”

For dark pools generally, “even if the result isn’t that there is new regulation, the result is the others are going to be sufficiently freaked out” by the complaint, said Kevin McPartland, head of market structure and research at Greenwich Associates in Stamford, Connecticut.

After news broke that Schneiderman was going after Barclays, the bank postponed an offering of notes, according to a person familiar with the matter, who asked to not be identified because of a lack of authorization to speak publicly.