WalkForwardOptimizer

- 라이브러리

- Stanislav Korotky

- 버전: 1.6

- 업데이트됨: 19 10월 2020

- 활성화: 5

WalkForwardOptimizer library allows you to perform rolling and cluster walk-forward optimization of expert advisers (EA) in MetaTrader 4.

To use the library include its header file WalkForwardOptimizer.mqh into your EA source code, add call provided functions as appropriate.

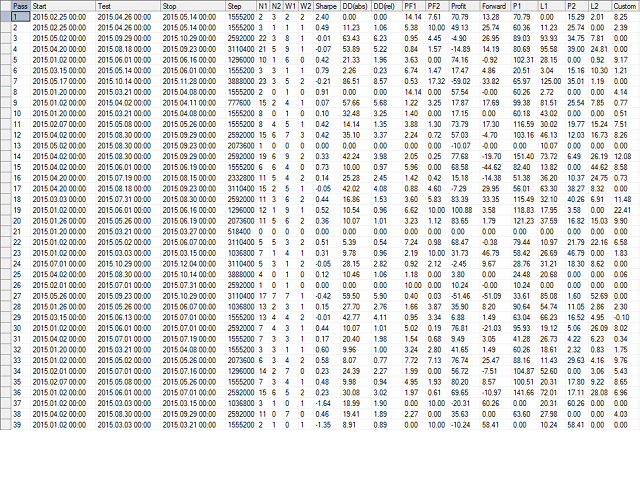

Once the library is embedded into EA, you may start optimization according to the procedure described in the User guide. When it's finished, intermediate results are saved into a csv-file and some special global variables. Then you can view and analyse the results by means of accompanying script WalkForwardReporter, which generates comprehensible reports as html-pages. The script is free.

Header file WalkForwardOptimizer.mqh

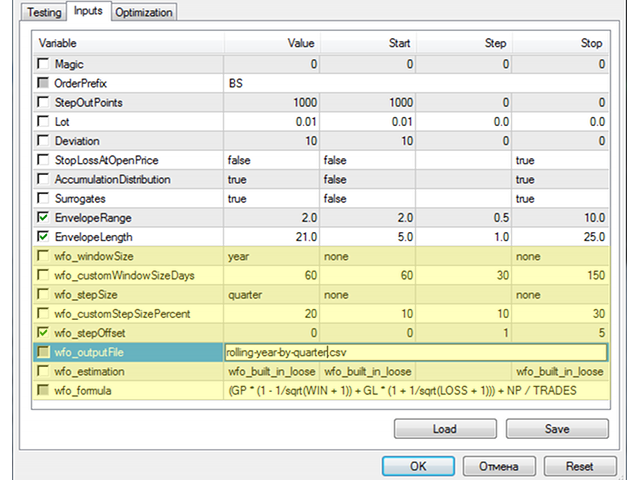

#define DAYS_PER_WEEK 7 #define DAYS_PER_MONTH 30 #define DAYS_PER_QUARTER (DAYS_PER_MONTH*3) #define DAYS_PER_HALF (DAYS_PER_MONTH*6) #define DAYS_PER_YEAR (DAYS_PER_MONTH*12) #define SEC_PER_DAY (60*60*24) #define SEC_PER_WEEK (SEC_PER_DAY*DAYS_PER_WEEK) #define SEC_PER_MONTH (SEC_PER_DAY*DAYS_PER_MONTH) #define SEC_PER_QUARTER (SEC_PER_MONTH*3) #define SEC_PER_HALF (SEC_PER_MONTH*6) #define SEC_PER_YEAR (SEC_PER_MONTH*12) #define CUSTOM_DAYS -1 enum WFO_TIME_PERIOD {none = 0, year = DAYS_PER_YEAR, halfyear = DAYS_PER_HALF, quarter = DAYS_PER_QUARTER, month = DAYS_PER_MONTH, week = DAYS_PER_WEEK, day = 1, custom = CUSTOM_DAYS}; enum WFO_ESTIMATION_METHOD {wfo_built_in_loose, wfo_built_in_strict, wfo_profit, wfo_sharpe, wfo_pf, wfo_drawdown, wfo_profit_by_drawdown, wfo_profit_trades_by_drawdown, wfo_average, wfo_expression}; extern WFO_TIME_PERIOD wfo_windowSize = year; extern int wfo_customWindowSizeDays = 0; extern WFO_TIME_PERIOD wfo_stepSize = quarter; extern int wfo_customStepSizePercent = 0; extern int wfo_stepOffset = 0; extern string wfo_outputFile = ""; extern WFO_ESTIMATION_METHOD wfo_estimation = wfo_built_in_loose; extern string wfo_formula = ""; #import "WalkForwardOptimizer.ex4" void wfo_setEstimationMethod(WFO_ESTIMATION_METHOD estimation, string formula); void wfo_setHeader(string s); void wfo_setPFmax(double max); void wfo_setGVAutomaticCleanup(bool b); void wfo_setCleanUpTimeout(int seconds); int wfo_OnInit(WFO_TIME_PERIOD optimizeOn, WFO_TIME_PERIOD optimizeStep, int optimizeStepOffset, int optimizeCustomW, int optimizeCustomS, string optimizeLog); int wfo_OnTick(); double wfo_OnTester(string payload = ""); void wfo_setCloseTradesOnSeparationLine(bool b); #import

Example of usage in your source code

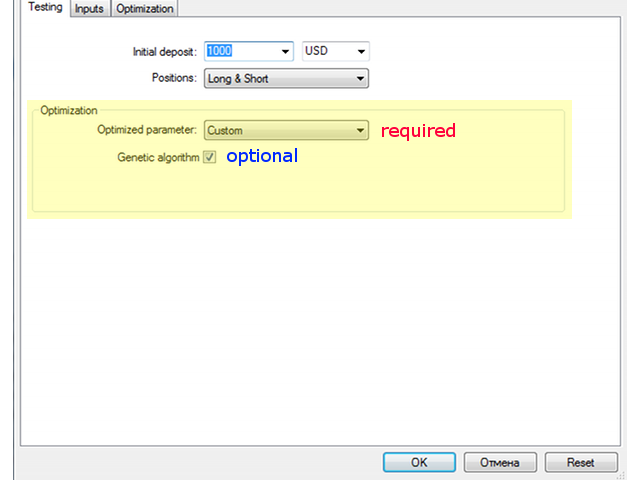

#include <WalkForwardOptimizer.mqh> ... int OnInit() { ... wfo_setEstimationMethod(wfo_estimation,wfo_formula); // wfo_built_in_loose by default wfo_setHeader("EnvelopeRange,EnvelopeLength"); // "Payload" by default wfo_setPFmax(100); // DBL_MAX by default // can be set to true, only if genetics not used // wfo_setGVAutomaticCleanup(true); // false by default // wfo_setCloseTradesOnSeparationLine(true); // false by default // this is the only required call in OnInit, all parameters come from the header int r = wfo_OnInit(wfo_windowSize, wfo_stepSize, wfo_stepOffset, wfo_customWindowSizeDays, wfo_customStepSizePercent, wfo_outputFile); return(r); } double OnTester() { // the passed string with optimizable work parameters of EA should match specified header in wfo_setHeader // the parameter is optional, you may have EA without parameters // the call to wfo_OnTester is required return wfo_OnTester(DoubleToStr(EnvelopeRange, 1) + "," + IntegerToString(EnvelopeLength)); } void OnTick() { int wfo = wfo_OnTick(); // required in OnTick if(wfo == -1) // this tick is before optimization window { return; } else if(wfo == +1) // this tick is after optimization window and forward test { return; } ... // your actual code goes here }

This library is a must have if you are trying to do a Walk Forward Analysis on MT4, and the author was very helpful when I had asked him questions. I would rent again!