Tester MT4 presenting big results that don't come back in reality

It may be the way around, how do you make your robot make more sense on live market.

For example,

Tester has got a fixed spread where as in real trading your spread will vary, which can have dramatic effects, unless you build in the a 'order only when spread is < lower then' feature.

Also, if your small stop loss get's hit a lot, you might consider setting it wider :) or even better, make it variable in a way it will adjust itself to market movements.

Best robots perform good on all currency pairs, adjust themselves or are adjustable to different timeframes, without the need of curve fitting, and that depends on the strategy used.

The "every tick" option doesn't mean that the MT bakctester uses ticks, collected from the market. It is a play on words.

In reality the MT tester "fabricates" ticks in a special algorithm in the bar range. The algorithm is described in the documentation.

It is possible an expert advisor to trade in such a way that exploits the backtesting algorithm logic in order to show highly overestimated and unreal results. I call that "method-fitting" in an analogy to the curve-fitting, which is also possible.

There are several other reasons for a false backtest - indicators that redraw past loosing signals, indicators that look in the future...

I'm fighting with this issues from 10 years and developed several other backtesting algos in the process.

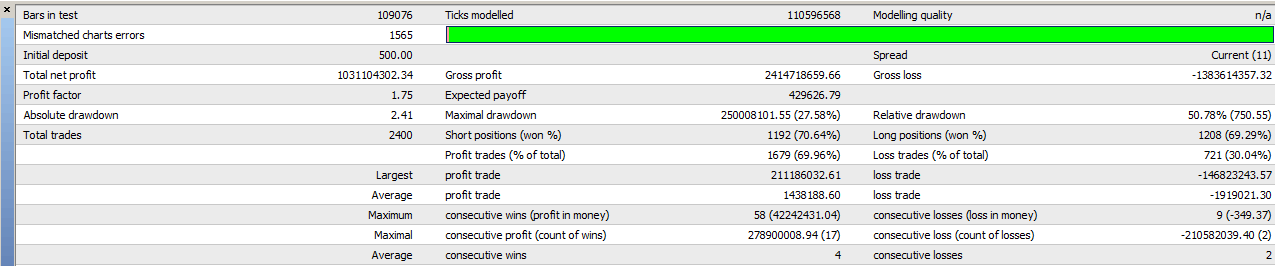

for example like this:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

Well, I read about 'tester' at this site and forum, but did not find an answer to my question: how can Strategy Tester MT4 present good results, that I don't see back in real trading? I use 'every tick'-mode in tester, but it seems that in real trading it makes less profits and more losses. So what good is then this tester??? Is there somebody who knows how to tackle this difference, so that testing in tester makes any sense? Is there a way or are there some kinda things to prevent (for example small stop loss that's hit more often in real trading than in tester?). Or any other solution to make a reliable test on my EA? Thank you so much in advance!