Press review - page 338

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

Forex Weekly Outlook August 3-7 (based on forexcrunch article)

US ISM Manufacturing PMI, Trade Balance, ISM Non-Manufacturing PMI, Rate decision in Japan, Employment data from New Zealand, Canada and the US, including the all-important NFP report. Join us as we explore this week’s market movers.

Last week the FOMC issued its rate statement reaffirming that the US economy continues to strengthen, leaving the door open for a possible interest rate hike in September. Policymakers noted the economy has rebounded from the slowdown, despite a downturn in the energy sector. The Fed also stated that the employment market saw solid gains in recent months, suggesting continued jobs growth. The Fed maintained its rates unchanged and noted the labor market needs to advance “some” more and inflation has to rise towards the 2% medium-term target, before the Fed decides to raise rates. Will we see a rate hike in September?

NFPs, BoE and RBA Will Stir Volatility Even If Risk Trends Hold Steady (based on dailyfx article)

"The most high-profile indicator on the list is the NFPs, but labor data's wage component and Monday's PCE inflation report speak more directly to rate forecasting. High level event risk for the UK and Australia should also have traders keeping tabs on Pound and Aussie sets going forward. We look at the event risk and market potential ahead in the weekend Trading Video."

Fundamental Weekly Forecasts for US Dollar, AUDUSD, GBPUSD. USDJPY and GOLD (based on dailyfx article)

US Dollar - "This week, we will come across two particular indicators in a busy docketthat are important for shaping rate expectations. Monday’s PCE deflator is the Fed’s favored inflation measure. Friday’s July labor report will generate headlines with its NFP print, but the policy speculation will center on the wages component – the wellspring of inflation. If this data misses or beats, few will miss the implications."

GBPUSD - "GBP/USD may continue to face range-bound prices ahead of the BoE meeting, and the fresh developments coming out of the central bank may set the tone for August as market participants weigh the outlook for monetary policy. In turn, we are still waiting for a break & close above near-term resistance around 1.5630 (38.2% retracement) to 1.5650 (38.2% expansion) to favor a more bullish outlook for the sterling, but a cautious tone from the BoE may drag on the exchange rate and spur a test of support around 1.5330 (78.6% expansion) to 1.5350 (50% retracement)."

AUDUSD - "The onset of risk aversion triggered by the prospect of US tightening even as growth in the Eurozone and China remains sluggish, threatening the outlook for global performance at large, may bode doubly ill for the Australian unit."

USDJPY - "The US Dollar remains relatively strong as interest rate traders predict the Fed will raise rates as early as September, but the official focus on data leaves risks clearly to the downside for the Greenback. This dynamic leaves the Japanese Yen especially exposed as it has historically been one of the most interest rate-sensitive currencies. Watch for outsized USD/JPY reactions to Friday’s NFPs data to guide overall direction through the foreseeable future."

GOLD - "From a technical standpoint gold has continued to respect a critical support confluence noted last week at ~1070/73. The trade remains vulnerable for a rebound while above this region heading into August open initial resistance seen at the 2014 lows at 1130. The broader outlook for gold remains bearish while sub 1145/51 with a break of the lows targeting the 2010 low at 1044 backed by a key longer-term Fibonacci confluence lower down at 975/80. We’ll keep an eye on the August opening range for further guidance on our near-term directional bias with a breach of the recent consolidation range between below 1103 shifting the immediate focus higher."

Weekly Fundamentals by Morgan Stanley: USD, EUR, JPY, GBP, CAD (based on efxnews article)

USD: Bullish

"We expect USD strength to be focused against EM and commodity currencies."

EUR: Bearish

"Many investors have hedged equity positions in Europe with short EUR. This suggests that in an environment where commodity currencies and EM may sell off, risk generally could take a hit, adding some support to EUR in the near term. Over the medium to longer term, however, we retain our bearish view on EUR."

JPY: Neutral

"We believe the BoJ is likely to refrain from further easing barring an unforeseeable shock to inflation, which should offer support to JPY. The central bank is likely focused on its new core CPI measure which does not include energy, and has grown steadily over recent months."

GBP: Bullish

"GBP performance will unfold in three phases going forward. First, broad-based GBP strength heading into the August 6 MPC meeting, where we expect the first vote for a rate hike. Second, a more selective approach after the August meeting. Finally, given the longer-term headwinds to UK growth from fiscal tightening and political uncertainty, the currency may lose steam after the first hike."

CAD: Bearish

"We like buying USDCAD on this dip, believing that as oil price uncertainty continues to mount, USDCAD will continue to head higher, testing the levels reached at the end of last week. On top of this, the second round impact of the lower oil price on the economy is likely to continue to be seen, possibly in upcoming employment data."

Skandinaviska Enskilda Banken: Outlooks For EUR/USD, USD/JPY, AUD/USD, SP500 (based on efxnews article)

EURUSD: rejection from the 55-day MA

'The up and down move on Friday became the third consecutive rejection from the 55d ma band (since the return below it a month ago). The behavior is showing that bearish forces are at play and increasingly so given the return to a negative slope. We are thus looking for additional selling.'

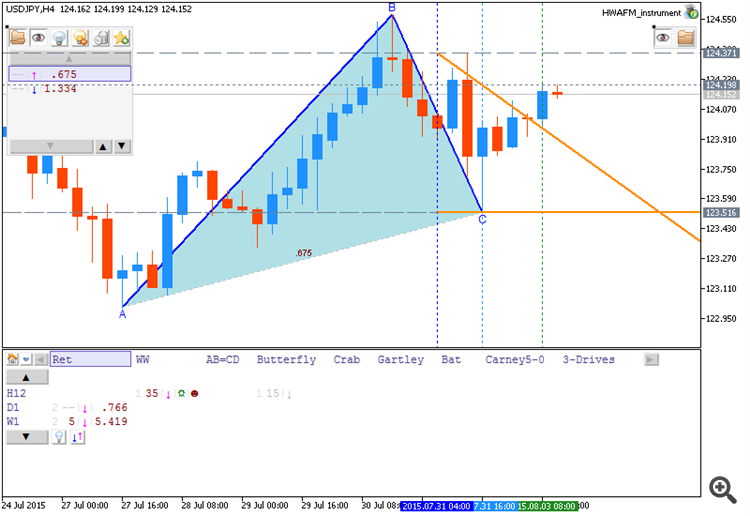

USDJPY: new attempt to be above the key level

'Given the violation of the B-wave high (and a three wave setback from Thursday’s peak) there’s a high probability of a soon more successful break higher (targeting a new trend high). For today we see 124.37 as the trigger point for the next step higher.'

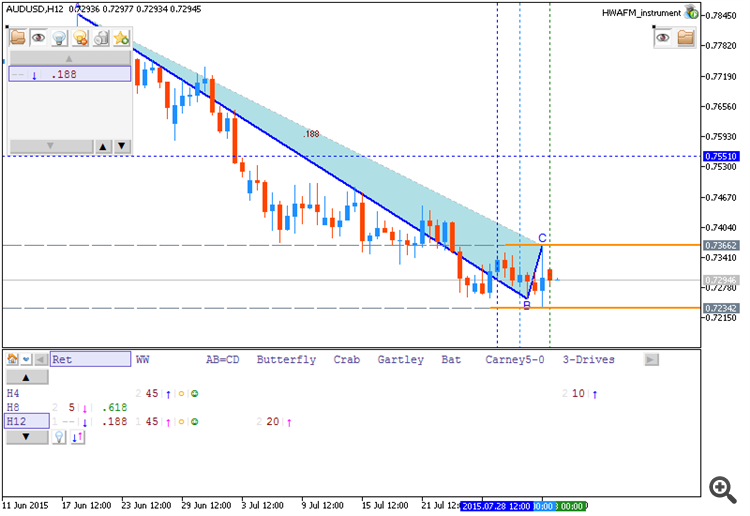

AUDUSD: Signs for sellers

'The spinning candle (small net move and big spikes to both sides) and the spring bottom are both signs of exhaustive sellers. There’s clearly a potential for the pair to bounce back to retest the 2001 trend line (or even back up to the 0.75- area) during the coming week.'

S&P 500: Higher again

'As long as the recent correction low remains unbroken a positive view should be kept in place (the July candle also developed into a mildly bullish piercing pattern). The entire structure since May can also be seen as an inverted head and shoulders formation, here seen as an upside continuation pattern.'

Societe Generale: EURUSD and Non-Farm Payrolls (based on efxnews article)

Societe Generale made some review for Non-Farm Employment Change report (Change in the number of employed people during the previous month, excluding the farming industry) which will be on Friday:

- "There’s a risk that we see edgy markets in the meantime...At

the risk of sounding like a broken record, the case for raising rates

to less unusually low levels does not rest on wage growth or inflation

returning in earnest first. Rates are too low, and capital is

misallocated as a result."

-

"More than the wage data however, we’d focus on the unemployment rate. We

look for a solid 240k increase in non-farm payrolls, a 2.2% increase in

hourly earnings and a drop to 5.2% from 5.3% in the unemployment rate."

-

"Anything that gets the front end of the curve higher in the US should

be negative for EUR/USD. A meander back above 1.10 is possible in the

early part of the week, but we’d like to sell against 1.11 and look for a

break lower in August."

Just to remind that previous NFP data was 223K, and forecasting for this Friday is aroud 224K for example (from 222K to 225K), so if Societe Generale is looking for 240K as anactual data for this Friday - it merans to be more bearish for EURUSD. Because in case of NPF: actual > forecast = good for currency (for US Dollar in our case). So, it means: more bearish for EURUSD with some key support levels to be broken. And Unemployment Rate is forecadting to be 5.2% from 5.3% by SG.Thus, I think - it may be good bearish breakdown during this high impacted news event.

Deutsche Bank - Get Ready For An August-October 'Jump' In USD/JPY (based on efxnews article)

Deutsche Bank made a forecast for USDJPY for August-October 2015 and for 2016:

"We believe the USD/JPY could jump to a ¥125-128 level over the next few months in reflection of robust US economic indicators."

"We expect the USD/JPY to strengthen in August-October and edge upward to only around ¥130 throughout 2016."

Let's evaluate this situation using Pivot Points and s/r levels.

If we look at USDJPY W1 timeframe so we see the price broke symmetric pattern from below to above with 125.85 as the nearest resistance level, and it is located for now between 120.40 support and 125.85 resistance.

The price is located to be above yearly Central Pivot at 114.36 and below R1 Pivot at 127.96. It means the bullish market condition with secondary ranging.

If we summarize above mentioned data so we can understand the following: the price is on primary bullish condition with the nearest target as 125.85. The next target is R1 Pivot at 127.96, and we may expect for this next target to be broken by the end of this year for example.

As to 2016 so it may be much easier - R2 Pivot level is located at 135.22, and it will be the next target in 2016 if the price will break 127.96 by the end of this year.

Thus, the forecast of Deutsche Bank was confirmed: ¥125-128 during August-October 2015, and around ¥130 in 2016.

Bank of Tokyo-Mitsubishi - 'we target EUR/USD at parity by year-end and at 0.96 by Q1'16-end' (based on efxnews article)

Bank of Tokyo-Mitsubishi (BTMU) made their fundamental forecasts for EURUSD based on some fundamental factors:

Bank of Tokyo-Mitsubishi (BTMU) forecasts for EURUSD to be at parity by year-end and at 0.96 by Q1'16-end.

By the way, the price is located to be below yearly Central Pivot at 1.2729 for the primary ranguing between S1 Pivot at 1.1466 and S2 Pivot at 1.0834, and the next target in the case the bearish trend will be continuing is S3 Pivot at 0.9571. So, the Bank of Tokyo-Mitsubishi (BTMU) is right with their forecast.

if hawkish > expected = good for currency (for AUD in our case)

More hawkish than expected = Good for currency

[AUD - Cash Rate and RBA Rate Statement] = Interest rate charged on overnight loans between financial intermediaries. Short term interest rates are the paramount factor in currency valuation - traders look at most other indicators merely to predict how rates will change in the future. RBA Rate Statement is among the primary tools the RBA Reserve Bank Board uses to communicate with investors about monetary policy. It contains the outcome of their decision on interest rates and commentary about the economic conditions that influenced their decision. Most importantly, it discusses the economic outlook and offers clues on the outcome of future decisions.

==========

"The Federal Reserve is expected to start increasing its policy rate later this year, but some other major central banks are continuing to ease policy. Hence, global financial conditions remain very accommodative. Despite fluctuations in markets associated with the respective developments in China and Greece, long-term borrowing rates for most sovereigns and creditworthy private borrowers remain remarkably low."

"The Board today judged that leaving the cash rate unchanged was appropriate at this meeting. Further information on economic and financial conditions to be received over the period ahead will inform the Board's ongoing assessment of the outlook and hence whether the current stance of policy will most effectively foster sustainable growth and inflation consistent with the target."

==========

AUDUSD M5: 94 pips price movement by AUD - Cash Rate news event :

EURUSD Breakout Fails (based on dailyfx article)

After traversing its daily 30 pip range, the EURUSD has opened the US trading session with a false breakout. Prices attempted a move above today’s R4 Camarilla pivot at 1.0979, but this bullish breakout quickly reversed. Prices are currently tradingback inside of today’s pivot range. As seen below, the EURUSD’s trading range begins at resistance found at the R3 pivot, at a price of 1.0964. If price continues to decline through values of support, traders will begin to look for price to target the S3 pivot found at a price of 1.0934.